Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Holder V OwnerDokument1 SeiteHolder V OwnerA. CampbellNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- 2016-03-21 - MTD Unconsionable ContractDokument9 Seiten2016-03-21 - MTD Unconsionable ContractA. CampbellNoch keine Bewertungen

- Unconscionable ContractDokument2 SeitenUnconscionable ContractA. Campbell100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Go FigureDokument1 SeiteGo FigureA. CampbellNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Part 2Dokument3 SeitenPart 2A. CampbellNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Bananas, Bikinis, GirlsDokument3 SeitenBananas, Bikinis, GirlsA. CampbellNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- 179124259410Dokument2 Seiten179124259410A. CampbellNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Opinion For Paatalo MTD DeniedDokument18 SeitenOpinion For Paatalo MTD DeniedA. Campbell100% (1)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Squirrelly Two StepDokument13 SeitenSquirrelly Two StepA. Campbell100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- 179124259801Dokument22 Seiten179124259801A. CampbellNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- 179124259822Dokument25 Seiten179124259822A. CampbellNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Zero SumDokument2 SeitenZero SumA. CampbellNoch keine Bewertungen

- Supreme Court Rules Mortgage Registration Business Has No Constitutionally Protected Interest in PropertyDokument34 SeitenSupreme Court Rules Mortgage Registration Business Has No Constitutionally Protected Interest in PropertyA. CampbellNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- 179124259513Dokument17 Seiten179124259513A. CampbellNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Cream NoteDokument1 SeiteCream NoteA. CampbellNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Star of BethlehemDokument8 SeitenStar of BethlehemA. CampbellNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- FTC Amicus BriefDokument25 SeitenFTC Amicus BriefA. Campbell100% (1)

- You Foot The Bill, SuckerDokument7 SeitenYou Foot The Bill, SuckerA. Campbell100% (2)

- Joey Rodriguez Petition For Writ of Certiorari (June 11 2015)Dokument74 SeitenJoey Rodriguez Petition For Writ of Certiorari (June 11 2015)A. CampbellNoch keine Bewertungen

- Writ Quo WarrantoDokument15 SeitenWrit Quo WarrantoA. CampbellNoch keine Bewertungen

- Rights of TitleDokument1 SeiteRights of TitleA. CampbellNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Ripley, Believe It or Not. It Happened.Dokument8 SeitenRipley, Believe It or Not. It Happened.A. CampbellNoch keine Bewertungen

- Common StatutoryDokument3 SeitenCommon StatutoryA. Campbell100% (1)

- Mammon or GodDokument1 SeiteMammon or GodA. CampbellNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- 26 Usc 6323Dokument2 Seiten26 Usc 6323A. CampbellNoch keine Bewertungen

- Security Promise 524Dokument7 SeitenSecurity Promise 524A. CampbellNoch keine Bewertungen

- Promise and PledgeDokument2 SeitenPromise and PledgeA. CampbellNoch keine Bewertungen

- Nolo Contenderé Hearsay SacrificedDokument1 SeiteNolo Contenderé Hearsay SacrificedA. CampbellNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Playing The Field: Geomagnetic Storms and The Stock MarketDokument53 SeitenPlaying The Field: Geomagnetic Storms and The Stock MarketPaolo100% (1)

- PermissiveDokument2 SeitenPermissiveA. CampbellNoch keine Bewertungen

- Important Schemes - Department of Financial Services - Ministry of Finance - Government of IndiaDokument4 SeitenImportant Schemes - Department of Financial Services - Ministry of Finance - Government of IndiaritulNoch keine Bewertungen

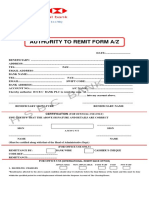

- HSBC Fund Transfer FORMDokument1 SeiteHSBC Fund Transfer FORMPinzariuSimona100% (1)

- BBNI - Annual Report 2019 - Lamp - 01Dokument308 SeitenBBNI - Annual Report 2019 - Lamp - 01Anton SocoNoch keine Bewertungen

- Economic FileDokument135 SeitenEconomic Filemonikarohilla33Noch keine Bewertungen

- AsdfghjklDokument2 SeitenAsdfghjklAdventurous FreakNoch keine Bewertungen

- Audit of Statement of Cash FlowsDokument2 SeitenAudit of Statement of Cash FlowsAndrew ManaloNoch keine Bewertungen

- BDO Unibank, Inc. (Bangco de Oro)Dokument2 SeitenBDO Unibank, Inc. (Bangco de Oro)Bevegel Sasan LlidoNoch keine Bewertungen

- Nike CorruptionDokument41 SeitenNike CorruptionLas Vegas Review-JournalNoch keine Bewertungen

- Pastor StatementDokument11 SeitenPastor StatementPaulNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Zakat DeclarationDokument1 SeiteZakat DeclarationSyed Mohsin SheraziNoch keine Bewertungen

- Midterm Examination in Business LogicDokument3 SeitenMidterm Examination in Business LogicMaguan, Vincent Paul A.Noch keine Bewertungen

- Cash ManagementDokument20 SeitenCash ManagementRahul DewakarNoch keine Bewertungen

- Dfi 211 Lecturer I-3Dokument40 SeitenDfi 211 Lecturer I-3CatherineNoch keine Bewertungen

- DBBL ChargesDokument9 SeitenDBBL ChargesAhmadullah Sohag100% (1)

- Bank ReconciliationDokument26 SeitenBank ReconciliationM Hammad KothariNoch keine Bewertungen

- The Mechanism of Letter of CreditDokument4 SeitenThe Mechanism of Letter of CreditKatrina MillerNoch keine Bewertungen

- Risk Management in Indian Banks: Some Emerging Issues: Dr. Krishn A.Goyal, Int. Eco. J. Res., 2010 1 (1) 102-109Dokument8 SeitenRisk Management in Indian Banks: Some Emerging Issues: Dr. Krishn A.Goyal, Int. Eco. J. Res., 2010 1 (1) 102-109Shukla JineshNoch keine Bewertungen

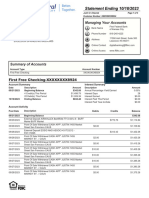

- E Passbook 2023 09 26 20 04 17 PMDokument140 SeitenE Passbook 2023 09 26 20 04 17 PMrajakarnal1987Noch keine Bewertungen

- The Prelist Along With The Checks Will Be Sent To TheDokument2 SeitenThe Prelist Along With The Checks Will Be Sent To TheRaca DesuNoch keine Bewertungen

- أساسيات صيغ التمويل الاسلامي المطبقة في الاقتصاد الاسلاميDokument19 Seitenأساسيات صيغ التمويل الاسلامي المطبقة في الاقتصاد الاسلاميJafarkolathurNoch keine Bewertungen

- Presentation On Internship at Global IME BankDokument10 SeitenPresentation On Internship at Global IME BankAnkit NeupaneNoch keine Bewertungen

- Final ProjectDokument22 SeitenFinal ProjectDishan Aich OfficialNoch keine Bewertungen

- Law On Negotiable InstrumentsDokument6 SeitenLaw On Negotiable InstrumentsLyRiCjEsS100% (1)

- ACI Dealing Certificate: SyllabusDokument12 SeitenACI Dealing Certificate: SyllabusKhaldon AbusairNoch keine Bewertungen

- DxwebDokument4 SeitenDxwebjustinagtrfde100Noch keine Bewertungen

- FABM 2 2nd Quarter (Week 1) Students Copy 2Dokument45 SeitenFABM 2 2nd Quarter (Week 1) Students Copy 2tjhunter077Noch keine Bewertungen

- Lecture 1 Financial Markets Inst. and InstrumentsDokument40 SeitenLecture 1 Financial Markets Inst. and InstrumentsPerbielyn BasinilloNoch keine Bewertungen

- Customer Application Form: Personal DetailsDokument19 SeitenCustomer Application Form: Personal DetailsAKNoch keine Bewertungen

- Document 3119946238763383936Dokument2 SeitenDocument 3119946238763383936abel zhangNoch keine Bewertungen

- Interbank Giro Credit CardDokument1 SeiteInterbank Giro Credit CardJulius Putra Tanu SetiajiNoch keine Bewertungen

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorVon EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorBewertung: 4.5 von 5 Sternen4.5/5 (63)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingVon EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingBewertung: 4.5 von 5 Sternen4.5/5 (97)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementVon EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementBewertung: 4.5 von 5 Sternen4.5/5 (20)

- Introduction to Negotiable Instruments: As per Indian LawsVon EverandIntroduction to Negotiable Instruments: As per Indian LawsBewertung: 5 von 5 Sternen5/5 (1)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorVon EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorBewertung: 4.5 von 5 Sternen4.5/5 (132)