Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- AGR NECEC FERC 206 Complaint Against NEE (10-13-2020) PDFDokument110 SeitenAGR NECEC FERC 206 Complaint Against NEE (10-13-2020) PDFPress Clean Energy MattersNoch keine Bewertungen

- 15562711-ad97-4f6d-9325-e852a0c8add9Dokument7 Seiten15562711-ad97-4f6d-9325-e852a0c8add9Julia FairNoch keine Bewertungen

- Laws Effective July 1, 2012Dokument12 SeitenLaws Effective July 1, 2012Georgette Takushi DeemerNoch keine Bewertungen

- Rep. Derek Kawakami Selected For NCSL Emerging Leaders Symposium NRDokument1 SeiteRep. Derek Kawakami Selected For NCSL Emerging Leaders Symposium NRGeorgette Takushi DeemerNoch keine Bewertungen

- Tax Review Final ReportDokument154 SeitenTax Review Final ReportGeorgette Takushi DeemerNoch keine Bewertungen

- House Members Oppose Tax Review Commission Recommendations NR 2012Dokument1 SeiteHouse Members Oppose Tax Review Commission Recommendations NR 2012Georgette Takushi DeemerNoch keine Bewertungen

- Marilyn Lee School Bus Cuts NRDokument1 SeiteMarilyn Lee School Bus Cuts NRGeorgette Takushi DeemerNoch keine Bewertungen

- Rep Isaac Choy TestimonyDokument4 SeitenRep Isaac Choy TestimonyGeorgette Takushi DeemerNoch keine Bewertungen

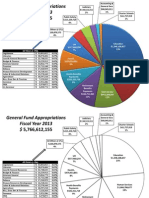

- Pie Chart 2013 GF AppropriationsDokument2 SeitenPie Chart 2013 GF AppropriationsGeorgette Takushi DeemerNoch keine Bewertungen

- Rep Denny Coffman Legislative Energy Horizon Institute CertificateDokument1 SeiteRep Denny Coffman Legislative Energy Horizon Institute CertificateGeorgette Takushi DeemerNoch keine Bewertungen

- Rep Denny Coffman Legislative Energy Horizon Institute CertificateDokument1 SeiteRep Denny Coffman Legislative Energy Horizon Institute CertificateGeorgette Takushi DeemerNoch keine Bewertungen

- Rep. Jerry Chang To Retire From Elected Office NRDokument1 SeiteRep. Jerry Chang To Retire From Elected Office NRGeorgette Takushi DeemerNoch keine Bewertungen

- Prevailing Winds Vol 4 Issue 4 May-June 2012Dokument2 SeitenPrevailing Winds Vol 4 Issue 4 May-June 2012Georgette Takushi DeemerNoch keine Bewertungen

- Pulse Summer 2011Dokument4 SeitenPulse Summer 2011Georgette Takushi DeemerNoch keine Bewertungen

- Rep Denny Coffman Legislative Energy Horizon Institute CertificateDokument1 SeiteRep Denny Coffman Legislative Energy Horizon Institute CertificateGeorgette Takushi DeemerNoch keine Bewertungen

- Ommunity Ewsletter: O R J JDokument4 SeitenOmmunity Ewsletter: O R J JGeorgette Takushi DeemerNoch keine Bewertungen

- 2011 Flyer Kauai WorkshopsDokument1 Seite2011 Flyer Kauai WorkshopsGeorgette Takushi DeemerNoch keine Bewertungen

- HB608 Organ Transplant FacilityDokument1 SeiteHB608 Organ Transplant FacilityGeorgette Takushi DeemerNoch keine Bewertungen

- Samuel Lee NRDokument1 SeiteSamuel Lee NRGeorgette Takushi DeemerNoch keine Bewertungen

- Project Interchange State Elected Officials ReleaseDokument3 SeitenProject Interchange State Elected Officials ReleaseGeorgette Takushi DeemerNoch keine Bewertungen

- Puuhulu Stream CleanupDokument2 SeitenPuuhulu Stream CleanupGeorgette Takushi DeemerNoch keine Bewertungen

- 2012 Session CalendarDokument2 Seiten2012 Session CalendarGeorgette Takushi DeemerNoch keine Bewertungen

- 2012 Classified AdDokument1 Seite2012 Classified AdGeorgette Takushi DeemerNoch keine Bewertungen

- Infrastructure Improvement Projects For Our Community Total Over $15 MillionDokument4 SeitenInfrastructure Improvement Projects For Our Community Total Over $15 MillionGeorgette Takushi DeemerNoch keine Bewertungen

- 2011 Flyer Big Island WorkshopsDokument1 Seite2011 Flyer Big Island WorkshopsGeorgette Takushi DeemerNoch keine Bewertungen

- 2012 Conference Room ScheduleDokument1 Seite2012 Conference Room ScheduleGeorgette Takushi DeemerNoch keine Bewertungen

- WLN Board Officer Press Release 2011-2012Dokument3 SeitenWLN Board Officer Press Release 2011-2012Georgette Takushi DeemerNoch keine Bewertungen

- NR NCSL Exec RepChongDokument2 SeitenNR NCSL Exec RepChongGeorgette Takushi DeemerNoch keine Bewertungen

- Reps Aquino and Cullen Hold Disaster Preparedness MeetingDokument1 SeiteReps Aquino and Cullen Hold Disaster Preparedness MeetingGeorgette Takushi DeemerNoch keine Bewertungen

- Mililani Community Report August 2011Dokument2 SeitenMililani Community Report August 2011Georgette Takushi DeemerNoch keine Bewertungen

- Purchase Order: Your Company Name Phone: XXX-XXX-XXXX Fax: XXX-XXX-XXXX Address, City, State, Zip CodeDokument12 SeitenPurchase Order: Your Company Name Phone: XXX-XXX-XXXX Fax: XXX-XXX-XXXX Address, City, State, Zip CodeBALAJINoch keine Bewertungen

- Ias Our Dram Gs NotesDokument129 SeitenIas Our Dram Gs Notesbalu56kvNoch keine Bewertungen

- NFLPA 2010 LM-2 Schedules 19 - 20Dokument13 SeitenNFLPA 2010 LM-2 Schedules 19 - 20Robert LeeNoch keine Bewertungen

- Asia Traders Insurance Corporation vs. Court of Appeals: Supreme Court Reports AnnotatedDokument7 SeitenAsia Traders Insurance Corporation vs. Court of Appeals: Supreme Court Reports AnnotatedKimmy DomingoNoch keine Bewertungen

- ISO 554-1976 ScanDokument4 SeitenISO 554-1976 ScanrezaeibehrouzNoch keine Bewertungen

- Knights Inn LawsuitDokument9 SeitenKnights Inn LawsuitTom JohanningmeierNoch keine Bewertungen

- COURSE SYLLABUS Book II Article 114 133Dokument5 SeitenCOURSE SYLLABUS Book II Article 114 133Honey Anjelyn M. MontecalboNoch keine Bewertungen

- Panes Vs Visayas State College of AgricultureDokument10 SeitenPanes Vs Visayas State College of Agriculturejimart10100% (1)

- Tamil Nadu Industrial Establishments (Conferment of Permanent Status To Workman Act, 1981Dokument12 SeitenTamil Nadu Industrial Establishments (Conferment of Permanent Status To Workman Act, 1981Latest Laws TeamNoch keine Bewertungen

- Section 9Dokument12 SeitenSection 9Ashish RajNoch keine Bewertungen

- JurisprudenceDokument2 SeitenJurisprudencextinemaniegoNoch keine Bewertungen

- SSRN Id2758033Dokument13 SeitenSSRN Id2758033Kumar Kaustubh Batch 2027Noch keine Bewertungen

- Chapter 7 Vocabulary DefinitionsDokument2 SeitenChapter 7 Vocabulary Definitionsapi-245168163Noch keine Bewertungen

- Morales v. Harbour Centre Port Terminal, G.R. No. 174208, Jan. 25, 2012Dokument9 SeitenMorales v. Harbour Centre Port Terminal, G.R. No. 174208, Jan. 25, 2012Martin SNoch keine Bewertungen

- Executive ReviewerDokument15 SeitenExecutive ReviewerJanica AngelesNoch keine Bewertungen

- TK 4001설명서2015Dokument11 SeitenTK 4001설명서2015geetha raniNoch keine Bewertungen

- 70 Policies That Shaped India PDFDokument212 Seiten70 Policies That Shaped India PDFKCNoch keine Bewertungen

- Contentio Writers NDA Kavita AdhikariDokument2 SeitenContentio Writers NDA Kavita Adhikarikavita adhikariNoch keine Bewertungen

- Constitution SummaryDokument4 SeitenConstitution SummaryBoy ToyNoch keine Bewertungen

- European Purchase Terms - EnglishDokument21 SeitenEuropean Purchase Terms - EnglishgheNoch keine Bewertungen

- Credit Card Application Form: Applicant'S InformationDokument4 SeitenCredit Card Application Form: Applicant'S InformationStacy BeckNoch keine Bewertungen

- Writs in Article 199 of The Constitution of PakistanDokument3 SeitenWrits in Article 199 of The Constitution of PakistanAwais KhanNoch keine Bewertungen

- Chihuly Inc Et Al v. LaCount Et Al - Document No. 7Dokument6 SeitenChihuly Inc Et Al v. LaCount Et Al - Document No. 7Justia.comNoch keine Bewertungen

- Norma AtexDokument4 SeitenNorma AtexV_VicNoch keine Bewertungen

- Lodha Park-2Dokument50 SeitenLodha Park-2Rohan BagadiyaNoch keine Bewertungen

- G.R. No. 78239 February 9, 1989 SALVACION A. MONSANTO, Petitioner, Vs - FULGENCIO S. FACTORAN, JR., RespondentDokument4 SeitenG.R. No. 78239 February 9, 1989 SALVACION A. MONSANTO, Petitioner, Vs - FULGENCIO S. FACTORAN, JR., RespondentI.F.S. VillanuevaNoch keine Bewertungen

- Attn: Rachel Olmogues Senior Sales RepresentativeDokument2 SeitenAttn: Rachel Olmogues Senior Sales RepresentativeShine BillonesNoch keine Bewertungen

- CPD FormDokument2 SeitenCPD FormAlex Olivar, Jr.Noch keine Bewertungen