Das könnte Ihnen auch gefallen

- Primus Automotion Devision Case 2002Dokument9 SeitenPrimus Automotion Devision Case 2002Devin Fortranansi FirdausNoch keine Bewertungen

- Financial Management Case 9 Primus Automation DivisionDokument15 SeitenFinancial Management Case 9 Primus Automation DivisiondidiNoch keine Bewertungen

- PrimusDokument11 SeitenPrimusClarissa Hapsari100% (1)

- AC 3 - Aurora Textile CompanyDokument6 SeitenAC 3 - Aurora Textile CompanySarmad100% (2)

- Jacobs Division PDFDokument5 SeitenJacobs Division PDFAbdul wahabNoch keine Bewertungen

- This Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Dokument19 SeitenThis Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)ntl2180% (1)

- The Body Shop Plc 2001: Historical Financial AnalysisDokument13 SeitenThe Body Shop Plc 2001: Historical Financial AnalysisNaman Nepal100% (1)

- P&G Acquisition of Gillette - CalculationDokument8 SeitenP&G Acquisition of Gillette - CalculationAryan AnandNoch keine Bewertungen

- Aurora Textile CompanyDokument47 SeitenAurora Textile CompanyMoHadrielCharki63% (8)

- Ben & Jerry'sDokument2 SeitenBen & Jerry'sThea Delicia100% (2)

- BCE: INC Case AnalysisDokument6 SeitenBCE: INC Case AnalysisShuja Ur RahmanNoch keine Bewertungen

- PCL Case - ImplicationsDokument3 SeitenPCL Case - ImplicationsYen YeeNoch keine Bewertungen

- M&M PizzaDokument1 SeiteM&M Pizzasusana3gamito0% (4)

- Q1. What Inference Do You Draw From The Trends in The Free Cash Flow of The Company?Dokument6 SeitenQ1. What Inference Do You Draw From The Trends in The Free Cash Flow of The Company?sridhar607Noch keine Bewertungen

- Fonderia di Torino Case PresentationDokument1 SeiteFonderia di Torino Case Presentationpoo_granger5229Noch keine Bewertungen

- Bayonne Packaging, Inc - Case Solution QualityDokument19 SeitenBayonne Packaging, Inc - Case Solution QualityCheenu JainNoch keine Bewertungen

- Financial ratio analysis and evaluationDokument3 SeitenFinancial ratio analysis and evaluationDwinanda SeptiadhiNoch keine Bewertungen

- Quiz 1Dokument3 SeitenQuiz 1Yong RenNoch keine Bewertungen

- Goff Computer's Cost of Capital AnalysisDokument13 SeitenGoff Computer's Cost of Capital AnalysisChris Galvez100% (1)

- Pharma SimDokument31 SeitenPharma SimOsman Abdul Quader100% (2)

- Dupont AnalysisDokument4 SeitenDupont AnalysisCha-am JamalNoch keine Bewertungen

- Case Background: Case - TSE International CompanyDokument9 SeitenCase Background: Case - TSE International CompanyAvinash AgrawalNoch keine Bewertungen

- Arcadian Business CaseDokument20 SeitenArcadian Business CaseHeniNoch keine Bewertungen

- Deal Genzyme en tcm28-30538Dokument5 SeitenDeal Genzyme en tcm28-30538Jorge M TorresNoch keine Bewertungen

- Typical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetDokument7 SeitenTypical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetSylvan EversNoch keine Bewertungen

- Kota SolutionDokument59 SeitenKota SolutionAlvaro M. JimenezNoch keine Bewertungen

- IB SummaryDokument7 SeitenIB SummaryrronakrjainNoch keine Bewertungen

- JetBlue SASB Sustainability LeadershipDokument1 SeiteJetBlue SASB Sustainability LeadershipShivani KarkeraNoch keine Bewertungen

- YVCDokument2 SeitenYVCnetterinder0% (1)

- Acquisition of YVC by TSEDokument2 SeitenAcquisition of YVC by TSEZia AhmadNoch keine Bewertungen

- Investment Detective CaseDokument1 SeiteInvestment Detective CaseJonathan ZhaoNoch keine Bewertungen

- Managing Multinational Financial Systems for Tax ArbitrageDokument14 SeitenManaging Multinational Financial Systems for Tax ArbitrageKARISHMAATA2Noch keine Bewertungen

- Case 13Dokument12 SeitenCase 13Superb AdnanNoch keine Bewertungen

- Accounting For Frequent FliersDokument3 SeitenAccounting For Frequent FliersJorge Abreu AbudNoch keine Bewertungen

- Case Study Analysis: Chestnut FoodsDokument7 SeitenCase Study Analysis: Chestnut FoodsNaman KohliNoch keine Bewertungen

- 1800flowers Com Company AnalysisDokument21 Seiten1800flowers Com Company AnalysissyedsubzposhNoch keine Bewertungen

- Fonderia Di Torina SpADokument10 SeitenFonderia Di Torina SpARoberta AyalingoNoch keine Bewertungen

- Case Analysis - Compania de Telefonos de ChileDokument4 SeitenCase Analysis - Compania de Telefonos de ChileSubrata BasakNoch keine Bewertungen

- The Financial DetectiveDokument5 SeitenThe Financial DetectiveCole DanielsNoch keine Bewertungen

- AutoZone financial analysis and stock repurchase impactDokument1 SeiteAutoZone financial analysis and stock repurchase impactmalimojNoch keine Bewertungen

- Case StudyDokument4 SeitenCase StudyArifNoch keine Bewertungen

- Ch. 15 Capital StructureDokument69 SeitenCh. 15 Capital StructureScorpian MouniehNoch keine Bewertungen

- Chapter 13: Leverage and Capital Structure (Continued) : Tutorial 6Dokument2 SeitenChapter 13: Leverage and Capital Structure (Continued) : Tutorial 6musicslave96Noch keine Bewertungen

- AnageneDokument1 SeiteAnagenevijai100% (1)

- Aleph Farms Case Analysis Highlights Company's Focus on SustainabilityDokument7 SeitenAleph Farms Case Analysis Highlights Company's Focus on SustainabilityOlivia HorvathNoch keine Bewertungen

- Financial ManagementDokument12 SeitenFinancial ManagementVaibhav AroraNoch keine Bewertungen

- Cashlet 4Dokument3 SeitenCashlet 4Vinay SharmaNoch keine Bewertungen

- Hausser Foods SCDokument6 SeitenHausser Foods SCHumphrey OsaigbeNoch keine Bewertungen

- OM Scott Case AnalysisDokument20 SeitenOM Scott Case AnalysissushilkhannaNoch keine Bewertungen

- Example of Investment Analysis Paper PDFDokument24 SeitenExample of Investment Analysis Paper PDFYoga Nurrahman AchfahaniNoch keine Bewertungen

- Nike Inc - Case Solution (Syndicate Group 4) - FadhilaDokument13 SeitenNike Inc - Case Solution (Syndicate Group 4) - FadhilaFadhila HanifNoch keine Bewertungen

- Syndicate 2 - Decision Tree (Day 1)Dokument20 SeitenSyndicate 2 - Decision Tree (Day 1)Dina Rizkia RachmahNoch keine Bewertungen

- Delta AssignmentDokument4 SeitenDelta Assignmentbinzidd007Noch keine Bewertungen

- Accounting for Frequent FliersDokument28 SeitenAccounting for Frequent FliersSyed Mazhar Ali Kazmi0% (1)

- ASsignmentDokument10 SeitenASsignmenthu mirzaNoch keine Bewertungen

- Aurora Textile Investment AnalysisDokument9 SeitenAurora Textile Investment AnalysisRoger Toni50% (2)

- Payback Period-1Dokument12 SeitenPayback Period-1OlamiNoch keine Bewertungen

- Fin 425 Final NIKEDokument11 SeitenFin 425 Final NIKEcuterahaNoch keine Bewertungen

- Investment Appraisal Report (Individual Report)Dokument10 SeitenInvestment Appraisal Report (Individual Report)Eric AwinoNoch keine Bewertungen

- Financial Management 2 2Dokument5 SeitenFinancial Management 2 2karma SherpaNoch keine Bewertungen

- Kota Fibres Case Study: Improving Cash Flow Through Operational ChangesDokument4 SeitenKota Fibres Case Study: Improving Cash Flow Through Operational ChangesZhijian HuangNoch keine Bewertungen

- Report On Teletech Corporation Case StudyDokument1 SeiteReport On Teletech Corporation Case StudyZhijian HuangNoch keine Bewertungen

- Saxonville Case StudyDokument4 SeitenSaxonville Case StudyZhijian Huang100% (1)

- Saxonville Case StudyDokument4 SeitenSaxonville Case StudyZhijian Huang100% (1)

- Mountain Man Case StudyDokument4 SeitenMountain Man Case StudyZhijian Huang100% (2)

- Unit 1 Concept of Human Resources ManagementDokument2 SeitenUnit 1 Concept of Human Resources ManagementPrajita ShresthaNoch keine Bewertungen

- ResumeChaturyaKommala PDFDokument2 SeitenResumeChaturyaKommala PDFbharathi yenneNoch keine Bewertungen

- SAP Agricultural Contract ManagementDokument14 SeitenSAP Agricultural Contract ManagementPaulo FranciscoNoch keine Bewertungen

- WEEK 10-Compensating Human Resources and Employee Benfeits and ServicesDokument8 SeitenWEEK 10-Compensating Human Resources and Employee Benfeits and ServicesAlfred John TolentinoNoch keine Bewertungen

- Professional Practice NotesDokument5 SeitenProfessional Practice NotesSHELLA MARIE DELOS REYESNoch keine Bewertungen

- The Impact of Effective Public Relations On Organizational Performance in Micmakin Nigeria LimitedDokument8 SeitenThe Impact of Effective Public Relations On Organizational Performance in Micmakin Nigeria LimitedBajegbo OluwadamilareNoch keine Bewertungen

- I HG F Autumn 2018 ApplicationformDokument8 SeitenI HG F Autumn 2018 ApplicationformSnzy DelNoch keine Bewertungen

- 9 External Environment Factors That Affect BusinessDokument5 Seiten9 External Environment Factors That Affect BusinessHasan NaseemNoch keine Bewertungen

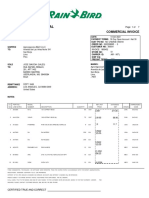

- Rain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Dokument7 SeitenRain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Alejandra JamboNoch keine Bewertungen

- Technical DetailsDokument3 SeitenTechnical DetailsKimberly NorrisNoch keine Bewertungen

- Housing Site AnalysisDokument1 SeiteHousing Site AnalysisFrances Irish Marasigan100% (1)

- SAP Plant Maintenance Training PDFDokument5 SeitenSAP Plant Maintenance Training PDFRAMRAJA RAMRAJANoch keine Bewertungen

- Engineering Marketing and EntrepreneurshipDokument41 SeitenEngineering Marketing and Entrepreneurshipimma coverNoch keine Bewertungen

- Qip QSB v4.2 - Trad P Anotaçôes Rev02Dokument17 SeitenQip QSB v4.2 - Trad P Anotaçôes Rev02Yasmin BatistaNoch keine Bewertungen

- Vishal JainDokument2 SeitenVishal JainVishal JainNoch keine Bewertungen

- How To Build A Double Calendar SpreadDokument26 SeitenHow To Build A Double Calendar SpreadscriberoneNoch keine Bewertungen

- Fuel Supply Agreement - LNG - UI 2021 (407769612.1)Dokument54 SeitenFuel Supply Agreement - LNG - UI 2021 (407769612.1)Edmund KhoveyNoch keine Bewertungen

- Lean Fundamentals Training: Gain A World Recognised AccreditationDokument4 SeitenLean Fundamentals Training: Gain A World Recognised AccreditationAhmed ElhajNoch keine Bewertungen

- Breakfast is the Most Important Meal: Starting a Pancake House BusinessDokument28 SeitenBreakfast is the Most Important Meal: Starting a Pancake House BusinessChristian Lim100% (1)

- Project Report On Birla Sun LifeDokument62 SeitenProject Report On Birla Sun Lifeeshaneeraj94% (34)

- Tradenet Funded Account Review - ($14,000 Buying Power)Dokument3 SeitenTradenet Funded Account Review - ($14,000 Buying Power)Enrique BlancoNoch keine Bewertungen

- Introduction of BRAC Bank's centralized operations during COVIDDokument4 SeitenIntroduction of BRAC Bank's centralized operations during COVIDTarannum TahsinNoch keine Bewertungen

- HR Management Key to Success of Virtual Firm iGATEDokument20 SeitenHR Management Key to Success of Virtual Firm iGATERajanMakwanaNoch keine Bewertungen

- (N-Ab) (1-A) : To Tariffs)Dokument16 Seiten(N-Ab) (1-A) : To Tariffs)Amelia JNoch keine Bewertungen

- FPC ManualDokument8 SeitenFPC ManualAdnan KaraahmetovicNoch keine Bewertungen

- Practices by KFCDokument17 SeitenPractices by KFCfariaNoch keine Bewertungen

- HGS Launches New Customer Experience Solution in U.S. (Company Update)Dokument2 SeitenHGS Launches New Customer Experience Solution in U.S. (Company Update)Shyam SunderNoch keine Bewertungen

- Done OJTjvvvvvDokument30 SeitenDone OJTjvvvvvMike Lawrence CadizNoch keine Bewertungen

- Forensic Accounting Notes - Lesson 1 2Dokument11 SeitenForensic Accounting Notes - Lesson 1 2wambualucas74Noch keine Bewertungen

- Cash PoolingDokument10 SeitenCash PoolingsavepageNoch keine Bewertungen