Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Addis Ababa University: College of Business and Economics Departement of Accounting and FinanceDokument57 SeitenAddis Ababa University: College of Business and Economics Departement of Accounting and FinanceALem Alem100% (1)

- Project On NJ India Invest PVT LTDDokument77 SeitenProject On NJ India Invest PVT LTDrajveerpatidar69% (26)

- (120406) MPAM Market LetterDokument2 Seiten(120406) MPAM Market LettergsprivNoch keine Bewertungen

- (120504) MPAM Market LetterDokument2 Seiten(120504) MPAM Market LettergsprivNoch keine Bewertungen

- (110606-10) MPAM Market LetterDokument1 Seite(110606-10) MPAM Market LettergsprivNoch keine Bewertungen

- (110401) MPAM Market LetterDokument2 Seiten(110401) MPAM Market LettergsprivNoch keine Bewertungen

- (101217) Global Macro Calls 2011Dokument1 Seite(101217) Global Macro Calls 2011gsprivNoch keine Bewertungen

- (110204) MPAM Market LetterDokument1 Seite(110204) MPAM Market LettergsprivNoch keine Bewertungen

- Security Analysis and Portfolio ManagementDokument3 SeitenSecurity Analysis and Portfolio ManagementRam MintoNoch keine Bewertungen

- Andrea Unger OTS2018 Presentation SlidesDokument58 SeitenAndrea Unger OTS2018 Presentation Slidesshree bNoch keine Bewertungen

- Internship Report On Finance MBADokument95 SeitenInternship Report On Finance MBABhaskar GuptaNoch keine Bewertungen

- Investment Manager Financial Analyst in Seattle WA Resume Greg EisenDokument2 SeitenInvestment Manager Financial Analyst in Seattle WA Resume Greg EisenGregEisenNoch keine Bewertungen

- Iqbal Khan, MMS 75, Capstone ProjectDokument71 SeitenIqbal Khan, MMS 75, Capstone ProjectSatish JadhavNoch keine Bewertungen

- Customer Perception Towards Mutual Fund FinalDokument74 SeitenCustomer Perception Towards Mutual Fund FinalujranchamanNoch keine Bewertungen

- SKKPDokument14 SeitenSKKPgloomy monsterNoch keine Bewertungen

- Security Analysis and Portfolio ManagementDokument11 SeitenSecurity Analysis and Portfolio Managementsarah IsharatNoch keine Bewertungen

- 3rd Annual Private Wealth Management Summit 2019Dokument11 Seiten3rd Annual Private Wealth Management Summit 2019Sreejit NairNoch keine Bewertungen

- CFA III. MockexamDokument53 SeitenCFA III. MockexamHoang Thi Phuong ThuyNoch keine Bewertungen

- Hedge Fund Risk Modeling: Miguel Alvarez Mike LevinsonDokument27 SeitenHedge Fund Risk Modeling: Miguel Alvarez Mike LevinsonkiransookNoch keine Bewertungen

- Chentia Aisya Oktarina - 242221055 - Magister ManajemenDokument34 SeitenChentia Aisya Oktarina - 242221055 - Magister ManajemenChentia Aisya OktarinaNoch keine Bewertungen

- GIC Report 2015Dokument66 SeitenGIC Report 2015sdgaNoch keine Bewertungen

- Project ReportDokument53 SeitenProject ReportAbhishek MishraNoch keine Bewertungen

- Al Safi PlatformDokument15 SeitenAl Safi PlatformbadrishNoch keine Bewertungen

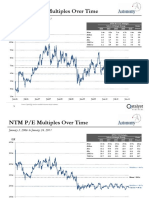

- NTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011Dokument3 SeitenNTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011mittleNoch keine Bewertungen

- Dulverton TrustDokument39 SeitenDulverton TrustCazzac111Noch keine Bewertungen

- Syllabus 15Dokument10 SeitenSyllabus 15carmenng1990Noch keine Bewertungen

- Casey Quirk (2008) - The New GatekeepersDokument30 SeitenCasey Quirk (2008) - The New Gatekeeperssawilson1Noch keine Bewertungen

- Syllabus Course 1: Global Financial Markets and AssetsDokument12 SeitenSyllabus Course 1: Global Financial Markets and AssetsFerNoch keine Bewertungen

- Boom and Bust A Collection of EssaysDokument221 SeitenBoom and Bust A Collection of Essaysdhritiman30Noch keine Bewertungen

- Marcellus Little-Champs PresentationDokument17 SeitenMarcellus Little-Champs PresentationqwertyNoch keine Bewertungen

- Summary - Reading 20Dokument5 SeitenSummary - Reading 20derek_2010Noch keine Bewertungen

- AMFI ReportsDokument1.030 SeitenAMFI ReportsDustyHouseNoch keine Bewertungen

- 4 - 1-A Macro Risk-Based Approach - J-TeiletcheDokument19 Seiten4 - 1-A Macro Risk-Based Approach - J-TeiletcheLoulou DePanamNoch keine Bewertungen

- MN2177 Block5Dokument12 SeitenMN2177 Block5Mandy SunNoch keine Bewertungen

- PrimeInvestor Guide To Profitable PortfolioDokument66 SeitenPrimeInvestor Guide To Profitable Portfoliodabster7000Noch keine Bewertungen

- LUSETDokument1 SeiteLUSETVan LLiNoch keine Bewertungen