Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- CH 8 Sales MixDokument12 SeitenCH 8 Sales MixNikki Coleen SantinNoch keine Bewertungen

- iFASTCorp AnnualReport 2020Dokument216 SeiteniFASTCorp AnnualReport 2020Zheng Yuan TanNoch keine Bewertungen

- Module 9 - Earnings and Market Approach ValuationDokument46 SeitenModule 9 - Earnings and Market Approach Valuationnatalie clyde matesNoch keine Bewertungen

- Investor Day Presentation 2015 PDFDokument152 SeitenInvestor Day Presentation 2015 PDFexpairtiseNoch keine Bewertungen

- Indian Stock Market Training PresentationDokument40 SeitenIndian Stock Market Training PresentationShakti Shukla100% (1)

- Dse 05Dokument3 SeitenDse 05SharifMahmudNoch keine Bewertungen

- Logistics & Distribution Management: Name Roll No. Organization Position HeldDokument18 SeitenLogistics & Distribution Management: Name Roll No. Organization Position HeldVikas SinglaNoch keine Bewertungen

- Chapter 19 Test BankDokument100 SeitenChapter 19 Test BankBrandon LeeNoch keine Bewertungen

- Iridium Case Study InstructionsDokument3 SeitenIridium Case Study InstructionsAnkush AgrawalNoch keine Bewertungen

- 2020 Level II IFT Study PlannerDokument11 Seiten2020 Level II IFT Study PlannerzainNoch keine Bewertungen

- Brand Prefernce of Scooters in Kathmandu Valley by FemaleDokument12 SeitenBrand Prefernce of Scooters in Kathmandu Valley by Femalegobindapandit1213Noch keine Bewertungen

- Solutions To The Problems in Introduction To Dynamic Macroeconomic TheoryDokument9 SeitenSolutions To The Problems in Introduction To Dynamic Macroeconomic TheoryYutUyiNoch keine Bewertungen

- DMC College Foundation: School of Business and Accountancy Bachelor of Science in Accountancy Sta. Filomena, Dipolog CityDokument12 SeitenDMC College Foundation: School of Business and Accountancy Bachelor of Science in Accountancy Sta. Filomena, Dipolog CityEarl Russell S PaulicanNoch keine Bewertungen

- QUOTESDokument147 SeitenQUOTESYAMRAJ SINGHNoch keine Bewertungen

- Transaction History Reportwellnxtcorporwellnxt Corporation14062019210657Dokument2 SeitenTransaction History Reportwellnxtcorporwellnxt Corporation14062019210657roda mansuetoNoch keine Bewertungen

- Independent University, Bangladesh: Assignment 1: Youview PointDokument4 SeitenIndependent University, Bangladesh: Assignment 1: Youview PointRobiul Alam Rana100% (1)

- Neil Coe, Philip Kelly, Henry W. C. Yeung - Economic Geography - A Contemporary IntroductionDokument453 SeitenNeil Coe, Philip Kelly, Henry W. C. Yeung - Economic Geography - A Contemporary Introductionanut100% (1)

- Strategi Komunikasi Pemasaran Terpadu Mangsi Coffee Dalam Memperkenalkan KopiDokument6 SeitenStrategi Komunikasi Pemasaran Terpadu Mangsi Coffee Dalam Memperkenalkan KopiMade Aristiawan100% (1)

- Puma Financial Statements 2011 PDFDokument105 SeitenPuma Financial Statements 2011 PDFApple JuiceNoch keine Bewertungen

- Economic GeographyDokument20 SeitenEconomic GeographyИто ХиробумиNoch keine Bewertungen

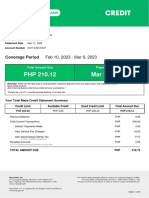

- MayaCredit SoA 2023MARDokument2 SeitenMayaCredit SoA 2023MARJan SaysonNoch keine Bewertungen

- Ethics of Business SystemsDokument49 SeitenEthics of Business SystemsSweta HansariaNoch keine Bewertungen

- Magnum PDFDokument11 SeitenMagnum PDFHarman Bhullar100% (1)

- Shimla Dairy Case Study ReportDokument4 SeitenShimla Dairy Case Study ReportAnu AmruthNoch keine Bewertungen

- Product Life Cycle of Lux SoapDokument23 SeitenProduct Life Cycle of Lux SoapSugandha KumariNoch keine Bewertungen

- HSBC Case AsbmDokument23 SeitenHSBC Case Asbmnitinchilli100% (3)

- PROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheDokument4 SeitenPROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheMargaveth P. Balbin75% (4)

- SCORE Annual Marketing Budget TemplateDokument1 SeiteSCORE Annual Marketing Budget TemplatePrincess AarthiNoch keine Bewertungen

- Karakteristik Perjanjian Jual Beli Medium Term Notes: Universitas AirlanggaDokument20 SeitenKarakteristik Perjanjian Jual Beli Medium Term Notes: Universitas AirlanggaMuhammad Rexel Abdi ZulfikarNoch keine Bewertungen

- Bengal Cement LTD.: Rate AdjustmentDokument3 SeitenBengal Cement LTD.: Rate AdjustmentLutfor RahmanNoch keine Bewertungen