Das könnte Ihnen auch gefallen

- Al Baraka BankDokument3 SeitenAl Baraka BankEisha AmjadNoch keine Bewertungen

- Introduction of BanksDokument4 SeitenIntroduction of BanksNoman AnsariNoch keine Bewertungen

- final projectDokument24 Seitenfinal projectSaboor BalochNoch keine Bewertungen

- Project Bank IslamiDokument26 SeitenProject Bank IslamiUzairNoch keine Bewertungen

- Ismail Arshad 1947172 Islamic Banking ProjectDokument10 SeitenIsmail Arshad 1947172 Islamic Banking Projectismail malikNoch keine Bewertungen

- Business and Organisation Structure of Standard Chartered BankDokument17 SeitenBusiness and Organisation Structure of Standard Chartered BankHumaira Shafiq0% (1)

- Group Information: Faysal BankDokument26 SeitenGroup Information: Faysal Bankbajwa122Noch keine Bewertungen

- Report HMBDokument14 SeitenReport HMBDaniyal SoomroNoch keine Bewertungen

- Internship ReportDokument32 SeitenInternship ReportZIA UL REHMANNoch keine Bewertungen

- Summit Bank Internship ReportDokument72 SeitenSummit Bank Internship ReportStranger BoyNoch keine Bewertungen

- 6 Faysal BankDokument58 Seiten6 Faysal BankUsman SaleemNoch keine Bewertungen

- Internship Report On Meezan Bank CompleteDokument86 SeitenInternship Report On Meezan Bank CompleteArslan96% (27)

- Management Information System of Standard Charterd Bank PVT LTDDokument18 SeitenManagement Information System of Standard Charterd Bank PVT LTDPakassignmentNoch keine Bewertungen

- Internship Report: Bank Alfalah LimitedDokument54 SeitenInternship Report: Bank Alfalah LimitedBadshah SalamutNoch keine Bewertungen

- MCB IslamicDokument21 SeitenMCB IslamicSadia ArslanNoch keine Bewertungen

- Annual Report of FAYSAL Bank Limited 2009Dokument129 SeitenAnnual Report of FAYSAL Bank Limited 2009zabeehNoch keine Bewertungen

- Meezan BankDokument83 SeitenMeezan BankAsifaNoreenNoch keine Bewertungen

- Internship Report: Bank Alfalah LimitedDokument12 SeitenInternship Report: Bank Alfalah LimitedRimsha TauqeerNoch keine Bewertungen

- Kasb BankDokument17 SeitenKasb BankUsman Chughtai0% (1)

- Internship Report On Meezan Bank CompleteDokument85 SeitenInternship Report On Meezan Bank CompleteJamil AhmedNoch keine Bewertungen

- ERP at HBL: Modules and BenefitsDokument22 SeitenERP at HBL: Modules and BenefitsJannat Aslam100% (1)

- Management Information System of Standard Charterd Bank PVT LTDDokument17 SeitenManagement Information System of Standard Charterd Bank PVT LTDUnscrewing_buks92% (13)

- Burj Bank's Islamic Banking Vision and OperationsDokument17 SeitenBurj Bank's Islamic Banking Vision and Operationshusnainrazzaqbaloch1Noch keine Bewertungen

- Bahria University Management ReportDokument13 SeitenBahria University Management ReportRahyla HassanNoch keine Bewertungen

- Leading Islamic Banking ProviderDokument6 SeitenLeading Islamic Banking ProviderZahid KhanNoch keine Bewertungen

- With The Name of Allah Most Compassionate Most MercifulDokument42 SeitenWith The Name of Allah Most Compassionate Most MercifulMimi ZamanNoch keine Bewertungen

- Training & DevelopmentDokument27 SeitenTraining & Developmentbushra saeedNoch keine Bewertungen

- Financial Institution: (Assignment)Dokument11 SeitenFinancial Institution: (Assignment)Muhammad Ahsan AkramNoch keine Bewertungen

- Faysal Bank Internship ReportDokument84 SeitenFaysal Bank Internship Reportimran_greenplus100% (3)

- Meezan BankDokument56 SeitenMeezan BankKhurram ShahzadNoch keine Bewertungen

- Habib Bank LimitedDokument64 SeitenHabib Bank Limitedviper959550% (2)

- Meezan BankDokument41 SeitenMeezan BankMohsin AliNoch keine Bewertungen

- Al Baraka Bank Pakistan OverviewDokument97 SeitenAl Baraka Bank Pakistan OverviewPrincess IqraNoch keine Bewertungen

- Summit Bank Internship ReportDokument72 SeitenSummit Bank Internship ReportAbdul Qadir50% (2)

- Organizational Analysis of Faysal Bank LtdDokument17 SeitenOrganizational Analysis of Faysal Bank LtdAsad UllahNoch keine Bewertungen

- Report of Meezan BankDokument15 SeitenReport of Meezan BankAbbasLiaqatQureshiNoch keine Bewertungen

- Faysal Bank Internship ReportDokument84 SeitenFaysal Bank Internship ReportSuleman H KhanNoch keine Bewertungen

- Internship ReportDokument65 SeitenInternship ReportPakassignmentNoch keine Bewertungen

- University of SindhDokument16 SeitenUniversity of Sindhameen panhwarNoch keine Bewertungen

- Standard Chartered Bank PakistanDokument19 SeitenStandard Chartered Bank PakistanMuhammad Mubasher Rafique100% (1)

- Meezan BankDokument16 SeitenMeezan BankSaifullahMakenNoch keine Bewertungen

- Internship Report On Askari Bank Limited MBA Finance, Hazara University Mansehra, Internship Ship Final Report Part 2 Jahangir KhanDokument60 SeitenInternship Report On Askari Bank Limited MBA Finance, Hazara University Mansehra, Internship Ship Final Report Part 2 Jahangir KhanJahangir KhanNoch keine Bewertungen

- Bank Alfala HCBFDokument59 SeitenBank Alfala HCBFNaaz SikandarNoch keine Bewertungen

- Bank AlFalahDokument89 SeitenBank AlFalahIrfan safdarNoch keine Bewertungen

- Malaysia Banking Industry AnalysisDokument21 SeitenMalaysia Banking Industry AnalysisAhmad Amiruddin60% (5)

- KARVY'S GUIDE TO INTEGRATED FINANCIAL SERVICESDokument54 SeitenKARVY'S GUIDE TO INTEGRATED FINANCIAL SERVICESj_sachin09Noch keine Bewertungen

- Money and Capital Markets PresentationDokument29 SeitenMoney and Capital Markets PresentationRashid MustahsanNoch keine Bewertungen

- Bank AlfahaDokument94 SeitenBank AlfahamcbNoch keine Bewertungen

- Bank AlflahDokument122 SeitenBank AlflahM Waqar JavedNoch keine Bewertungen

- Mission VisionmmDokument11 SeitenMission VisionmmHumayra SalsabilNoch keine Bewertungen

- Shari'ah Non-compliance Risk Management and Legal Documentations in Islamic FinanceVon EverandShari'ah Non-compliance Risk Management and Legal Documentations in Islamic FinanceNoch keine Bewertungen

- The Handbook of Financing Growth: Strategies, Capital Structure, and M&A TransactionsVon EverandThe Handbook of Financing Growth: Strategies, Capital Structure, and M&A TransactionsNoch keine Bewertungen

- Practice Made (More) Perfect: Transforming a Financial Advisory Practice Into a BusinessVon EverandPractice Made (More) Perfect: Transforming a Financial Advisory Practice Into a BusinessNoch keine Bewertungen

- Governance, Compliance and Supervision in the Capital MarketsVon EverandGovernance, Compliance and Supervision in the Capital MarketsNoch keine Bewertungen

- Algerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyVon EverandAlgerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyNoch keine Bewertungen

- Profiting from Hedge Funds: Winning Strategies for the Little GuyVon EverandProfiting from Hedge Funds: Winning Strategies for the Little GuyNoch keine Bewertungen

- Billing and Shipping Address for Gordon DillaDokument1 SeiteBilling and Shipping Address for Gordon DillaGh UnlockersNoch keine Bewertungen

- Guide For Health Insurance: Key For Associateship ExaminationDokument19 SeitenGuide For Health Insurance: Key For Associateship ExaminationDebasish25% (4)

- Myths of U.S. HealthcareDokument3 SeitenMyths of U.S. HealthcarecherylsealatlargeNoch keine Bewertungen

- US Bank Account Types and Features in 40 CharactersDokument7 SeitenUS Bank Account Types and Features in 40 CharactersAbhilash RjNoch keine Bewertungen

- JS2 Computer Studies Examination (Third Term)Dokument2 SeitenJS2 Computer Studies Examination (Third Term)Ejiro Ndifereke100% (4)

- QBO Cert Exam Module 3 - 4Dokument121 SeitenQBO Cert Exam Module 3 - 4Nikka ella LaraNoch keine Bewertungen

- An Internship Report ON Global Ime Bank Limited Chauraha, Dhangadhi Branch, Kailali Submitted by Kabita NegiDokument42 SeitenAn Internship Report ON Global Ime Bank Limited Chauraha, Dhangadhi Branch, Kailali Submitted by Kabita NegiSubin PariyarNoch keine Bewertungen

- Sales Order ProcessingDokument5 SeitenSales Order ProcessingSadaab HassanNoch keine Bewertungen

- 13A074Dokument15 Seiten13A074Naveen MeenaNoch keine Bewertungen

- Confident Guidance CG 09-2013Dokument4 SeitenConfident Guidance CG 09-2013api-249217077Noch keine Bewertungen

- MBM Criteria For Accreditation v2Dokument5 SeitenMBM Criteria For Accreditation v2Leo PorrasNoch keine Bewertungen

- Juniper Cloud Fundamentals (JCF)Dokument2 SeitenJuniper Cloud Fundamentals (JCF)MateiNoch keine Bewertungen

- Jio TariffDokument4 SeitenJio Tariffraja30gNoch keine Bewertungen

- b2c E-Commerce ReviewDokument10 Seitenb2c E-Commerce ReviewadiltsaNoch keine Bewertungen

- Wireshark 802.11 Display Filter Field Reference GuideDokument2 SeitenWireshark 802.11 Display Filter Field Reference Guideregister NameNoch keine Bewertungen

- Adjusting Entry Part 2Dokument4 SeitenAdjusting Entry Part 2Ken DiNoch keine Bewertungen

- KONUS-Flyer+2017 EnglischDokument2 SeitenKONUS-Flyer+2017 EnglischSoumi Bandyopadhyay SBNoch keine Bewertungen

- The Escape Plan - ngh625Dokument12 SeitenThe Escape Plan - ngh6252lmqibmsNoch keine Bewertungen

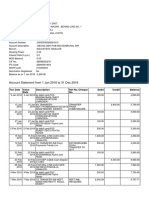

- Account Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 1 Jan 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceManishDikshitNoch keine Bewertungen

- AcademyCloudArchitecting Module 01Dokument36 SeitenAcademyCloudArchitecting Module 01Kaichun YauNoch keine Bewertungen

- MR - Meraki Wireless Access PointsDokument12 SeitenMR - Meraki Wireless Access PointsTerrel YehNoch keine Bewertungen

- Big BazaarDokument19 SeitenBig BazaarAlok RanjanNoch keine Bewertungen

- Telugu and I HaveDokument7 SeitenTelugu and I HaveSunidhi KNoch keine Bewertungen

- Unit 7 Channels of DistributionDokument14 SeitenUnit 7 Channels of DistributionKritika RajNoch keine Bewertungen

- Service-Charges 01.01.2022 WEBDokument58 SeitenService-Charges 01.01.2022 WEBRenesh RNoch keine Bewertungen

- 2023 2024 Academic Fees Schedule Nursing Med Lab Human NutitionDokument7 Seiten2023 2024 Academic Fees Schedule Nursing Med Lab Human Nutitionchukwuemekac359Noch keine Bewertungen

- AP - Cash in VaultDokument14 SeitenAP - Cash in VaultNorie Jane CaninoNoch keine Bewertungen

- Maritime HandbookDokument233 SeitenMaritime Handbookmohdsibhath ppNoch keine Bewertungen

- Social Security, Medicare and Medicaid Work For Washington 2012Dokument23 SeitenSocial Security, Medicare and Medicaid Work For Washington 2012SocialSecurityWorksNoch keine Bewertungen

- Unit - 3: Pricing Strategy Objectives & Pricing MethodsDokument13 SeitenUnit - 3: Pricing Strategy Objectives & Pricing MethodssreedeviNoch keine Bewertungen