Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Order Confirmation - IKEADokument1 SeiteOrder Confirmation - IKEAsandeepNoch keine Bewertungen

- Term Paper On Rolex: North South University Dhaka, BangladeshDokument39 SeitenTerm Paper On Rolex: North South University Dhaka, BangladeshSao Nguyễn ToànNoch keine Bewertungen

- Coming Jobs in PPSC: (Default - Aspx)Dokument2 SeitenComing Jobs in PPSC: (Default - Aspx)Tariq SultanNoch keine Bewertungen

- CesDokument3 SeitenCesTariq Sultan100% (1)

- Commonly Used Math FormulasDokument14 SeitenCommonly Used Math FormulasTariq SultanNoch keine Bewertungen

- Reliability Basics Overview of The Gumbel, Logistic, Loglogistic and Gamma DistributionsDokument7 SeitenReliability Basics Overview of The Gumbel, Logistic, Loglogistic and Gamma DistributionsTariq SultanNoch keine Bewertungen

- CesDokument3 SeitenCesTariq Sultan100% (1)

- Using The Trans-Log Expenditure Function To Endogenize New Market Access in Partial Equilibrium ModelsDokument15 SeitenUsing The Trans-Log Expenditure Function To Endogenize New Market Access in Partial Equilibrium ModelsTariq SultanNoch keine Bewertungen

- Apec 8001 Applied Microeconomic Analysis: Demand Theory Lecture 2: Consumer Choice (MWG, Ch. 2, Pp.17-28)Dokument21 SeitenApec 8001 Applied Microeconomic Analysis: Demand Theory Lecture 2: Consumer Choice (MWG, Ch. 2, Pp.17-28)Tariq SultanNoch keine Bewertungen

- CesDokument3 SeitenCesTariq Sultan100% (1)

- In VersesDokument3 SeitenIn VersesTariq SultanNoch keine Bewertungen

- Al-Mawardi - The Ordinances of Government - Al-Ahkam As-SultaniyyahDokument381 SeitenAl-Mawardi - The Ordinances of Government - Al-Ahkam As-SultaniyyahTariq Sultan100% (2)

- Economics 201b Spring 2010 Problem Set 4 SolutionsDokument15 SeitenEconomics 201b Spring 2010 Problem Set 4 SolutionsTariq SultanNoch keine Bewertungen

- 04Dokument20 Seiten04Tariq SultanNoch keine Bewertungen

- 1 The Deterministic Case: Stockholm Doctoral Program in Economics Handelsh Ogskolan I Stockholm Stockholms UniversitetDokument16 Seiten1 The Deterministic Case: Stockholm Doctoral Program in Economics Handelsh Ogskolan I Stockholm Stockholms UniversitetTariq SultanNoch keine Bewertungen

- Berg-E-Sehra by Mohsin NaqviDokument132 SeitenBerg-E-Sehra by Mohsin NaqviFarhan AnwarNoch keine Bewertungen

- Gifts: Philosophy and Economics InvolvedDokument2 SeitenGifts: Philosophy and Economics InvolvedTariq SultanNoch keine Bewertungen

- Macroeconomics TheoryDokument38 SeitenMacroeconomics TheoryTariq SultanNoch keine Bewertungen

- Quiz ME 1Dokument4 SeitenQuiz ME 1Radytia BimantaraNoch keine Bewertungen

- NMS COMPLEX EpgDokument12 SeitenNMS COMPLEX EpgVishnu KhandareNoch keine Bewertungen

- InvoiceDokument1 SeiteInvoicejadav karmakarNoch keine Bewertungen

- The Theory of Consumer Choice The Theory of Consumer Choice: MicroeconomicsDokument28 SeitenThe Theory of Consumer Choice The Theory of Consumer Choice: MicroeconomicsTannu RadhaNoch keine Bewertungen

- BUSINESS PLAN For ICDDokument26 SeitenBUSINESS PLAN For ICDtsegaye denberieNoch keine Bewertungen

- The Strategic and Operational Planning Process: Powerpoint Presentation by Charlie CookDokument38 SeitenThe Strategic and Operational Planning Process: Powerpoint Presentation by Charlie CookALTERINDONESIANoch keine Bewertungen

- Beco 2301 Macro l6 SV Ad-As Model p1Dokument24 SeitenBeco 2301 Macro l6 SV Ad-As Model p1Ahmed MousaNoch keine Bewertungen

- Strategic Analysis and Strategic Cost Management: Mcgraw-Hill/IrwinDokument33 SeitenStrategic Analysis and Strategic Cost Management: Mcgraw-Hill/IrwinTubagus Donny SyafardanNoch keine Bewertungen

- Full Download Understanding Canadian Business Canadian 8th Edition Nickels Test BankDokument35 SeitenFull Download Understanding Canadian Business Canadian 8th Edition Nickels Test Bankkiffershidx100% (31)

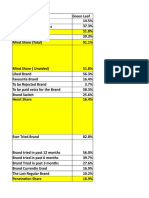

- Brand Health Analysis TemplateDokument4 SeitenBrand Health Analysis Templateanon_493704527Noch keine Bewertungen

- Merger and AcquisitionDokument4 SeitenMerger and Acquisitionshady emadNoch keine Bewertungen

- Markets PDFDokument4 SeitenMarkets PDFnostxlgiaNoch keine Bewertungen

- Strategic Plan of "Made in China 2025" and Its ImplementationDokument26 SeitenStrategic Plan of "Made in China 2025" and Its ImplementationHalli GalliNoch keine Bewertungen

- Role of CRM in MarketingDokument19 SeitenRole of CRM in MarketingVivek Kumar Gupta86% (14)

- Robusta Coffee Shop A Feasibility StudyDokument26 SeitenRobusta Coffee Shop A Feasibility StudysabberNoch keine Bewertungen

- SWOT Analysis Slides Powerpoint TemplateDokument20 SeitenSWOT Analysis Slides Powerpoint TemplateiedaNoch keine Bewertungen

- Unit 10 Brand Equity: Product PositioningDokument11 SeitenUnit 10 Brand Equity: Product Positioningsabyasachi samalNoch keine Bewertungen

- E Commerce Application Based On Farming ProductsDokument4 SeitenE Commerce Application Based On Farming ProductsEditor IJTSRDNoch keine Bewertungen

- Swot AnalysisDokument4 SeitenSwot AnalysisAhmad ShahNoch keine Bewertungen

- The Goal(s) of Monetary PolicyDokument8 SeitenThe Goal(s) of Monetary PolicyHafiz Saddique MalikNoch keine Bewertungen

- Outsourced Chief Investment Officer (OCIO) - Details, Activities and BenefitsDokument4 SeitenOutsourced Chief Investment Officer (OCIO) - Details, Activities and BenefitsTanyamagistralNoch keine Bewertungen

- International RetailingDokument13 SeitenInternational RetailingAbhi SinghNoch keine Bewertungen

- Burger King 5CDokument10 SeitenBurger King 5CYogesh Kumar0% (1)

- BUS100 Sample Final Chaps 11-16Dokument16 SeitenBUS100 Sample Final Chaps 11-16Muhammad SaeedNoch keine Bewertungen

- Basel 3Dokument32 SeitenBasel 3Venkat SaiNoch keine Bewertungen

- Army Source Selection Guide February 2007Dokument146 SeitenArmy Source Selection Guide February 2007Lovac1988Noch keine Bewertungen

- Consumer BehaviourDokument6 SeitenConsumer BehaviourShashank SharmaNoch keine Bewertungen

- Granolite Vitrified Tiles Pvt. LTD Project Report-Prince DudhatraDokument59 SeitenGranolite Vitrified Tiles Pvt. LTD Project Report-Prince DudhatrapRiNcE DuDhAtRaNoch keine Bewertungen