Das könnte Ihnen auch gefallen

- Pershing SQR 1Q 2Q 2014 Investor Letter 1Dokument20 SeitenPershing SQR 1Q 2Q 2014 Investor Letter 1ValueWalk50% (2)

- Investment Manager's Report: Letter To ShareholdersDokument19 SeitenInvestment Manager's Report: Letter To Shareholdersbrunomarz12345Noch keine Bewertungen

- Pershing Q1 2010 Investor LetterDokument13 SeitenPershing Q1 2010 Investor LetterguruekNoch keine Bewertungen

- Bob Robotti - Navigating Deep WatersDokument35 SeitenBob Robotti - Navigating Deep WatersCanadianValue100% (1)

- Greenhaven Road Capital Q1 2017Dokument12 SeitenGreenhaven Road Capital Q1 2017superinvestorbulletiNoch keine Bewertungen

- Pershing Square's Q1 Letter To InvestorsDokument10 SeitenPershing Square's Q1 Letter To InvestorsDealBook100% (22)

- FRP FinalDokument88 SeitenFRP Finalgeeta44Noch keine Bewertungen

- Investment Commentary: Market and Performance SummaryDokument12 SeitenInvestment Commentary: Market and Performance SummaryCanadianValueNoch keine Bewertungen

- Pershing Square Second-Quarter Investor LetterDokument23 SeitenPershing Square Second-Quarter Investor LetterNew York PostNoch keine Bewertungen

- Brookfield Asset Management q2 2013 Letter To ShareholdersDokument6 SeitenBrookfield Asset Management q2 2013 Letter To ShareholdersCanadianValueNoch keine Bewertungen

- Steven Romick September 30, 2010Dokument13 SeitenSteven Romick September 30, 2010eric695Noch keine Bewertungen

- H. Kevin Byun's Q4 2013 Denali Investors LetterDokument4 SeitenH. Kevin Byun's Q4 2013 Denali Investors LetterValueInvestingGuy100% (1)

- Report LimitadaDokument7 SeitenReport LimitadaandreatopNoch keine Bewertungen

- 2017 q3 Cef Investor LetterDokument6 Seiten2017 q3 Cef Investor LetterKini TinerNoch keine Bewertungen

- Q2 2015 KAM Conference Call 07-07-15 FINALDokument18 SeitenQ2 2015 KAM Conference Call 07-07-15 FINALCanadianValueNoch keine Bewertungen

- Third Point Q109 LetterDokument4 SeitenThird Point Q109 LetterZerohedgeNoch keine Bewertungen

- Portfolio Management - Part 2: Portfolio Management, #2Von EverandPortfolio Management - Part 2: Portfolio Management, #2Bewertung: 5 von 5 Sternen5/5 (9)

- Brenner West - 2010 Fourth Quarter LetterDokument4 SeitenBrenner West - 2010 Fourth Quarter LettergatzbpNoch keine Bewertungen

- PE - Norway Pension Fund - Evaluatin Investments in PE (Ver P. 32)Dokument154 SeitenPE - Norway Pension Fund - Evaluatin Investments in PE (Ver P. 32)Danilo Just SoaresNoch keine Bewertungen

- Greenlight Capital Letter (1-Oct-08)Dokument0 SeitenGreenlight Capital Letter (1-Oct-08)brunomarz12345Noch keine Bewertungen

- PM Perspective High YieldDokument8 SeitenPM Perspective High YieldMikeNoch keine Bewertungen

- Executive SummaryDokument6 SeitenExecutive SummaryhowellstechNoch keine Bewertungen

- DB Transcript 6-2-15Dokument10 SeitenDB Transcript 6-2-15rpconsultingNoch keine Bewertungen

- Artko Capital 2018 Q2 LetterDokument9 SeitenArtko Capital 2018 Q2 LetterSmitty WNoch keine Bewertungen

- Initial Public Offering - Ipo': Debt EquityDokument7 SeitenInitial Public Offering - Ipo': Debt Equitykomaloza25Noch keine Bewertungen

- Pershing Square Management's Letter To InvestorsDokument7 SeitenPershing Square Management's Letter To InvestorsDealBook100% (1)

- Reflections After 2 Years: Business Review To The Investment CommitteeDokument4 SeitenReflections After 2 Years: Business Review To The Investment Committeemaxmueller15Noch keine Bewertungen

- Third Point Q1'09 Investor LetterDokument4 SeitenThird Point Q1'09 Investor LetterDealBook100% (2)

- 1main Capital Q1 2022Dokument8 Seiten1main Capital Q1 2022dsfsadf asNoch keine Bewertungen

- Fpo Finally Final27-05Dokument73 SeitenFpo Finally Final27-05alwynsp50% (2)

- Paul Sonkin Investment StrategyDokument20 SeitenPaul Sonkin Investment StrategyCanadianValueNoch keine Bewertungen

- Week 1-4 - The Private Equity IndustryDokument5 SeitenWeek 1-4 - The Private Equity IndustryVirgilio Jay CervantesNoch keine Bewertungen

- Arlington Value 2011 Annual LetterDokument8 SeitenArlington Value 2011 Annual LetterChrisNoch keine Bewertungen

- Brookfield Letter To General Growth Re Reorganization PlanDokument7 SeitenBrookfield Letter To General Growth Re Reorganization PlanDealBookNoch keine Bewertungen

- SocietyOne Shareholder Update December 11 2013Dokument8 SeitenSocietyOne Shareholder Update December 11 2013Philip GardinerNoch keine Bewertungen

- 1Q 2019 PresentationDokument8 Seiten1Q 2019 Presentationaugtour4977Noch keine Bewertungen

- ZO1 - SW - Zooplus AG - Special Call - 08.13.21Dokument5 SeitenZO1 - SW - Zooplus AG - Special Call - 08.13.21LazardNoch keine Bewertungen

- IpoDokument5 SeitenIpoImroz MahmudNoch keine Bewertungen

- Investment Commentary: Market and Performance SummaryDokument20 SeitenInvestment Commentary: Market and Performance SummaryCanadianValueNoch keine Bewertungen

- WST PrattCapitalDokument7 SeitenWST PrattCapital4thfloorvalueNoch keine Bewertungen

- Third Point Q3 Investor LetterDokument8 SeitenThird Point Q3 Investor Lettersuperinvestorbulleti100% (1)

- Financing A New Venture Trough and Initial Public Offering (IPO)Dokument32 SeitenFinancing A New Venture Trough and Initial Public Offering (IPO)Manthan LalanNoch keine Bewertungen

- IPO Versus RTODokument5 SeitenIPO Versus RTOpaksengNoch keine Bewertungen

- PIPES Private Equity Investments in Distressed FirmsDokument8 SeitenPIPES Private Equity Investments in Distressed Firmselentini11111Noch keine Bewertungen

- Wow Si Ép ÊiDokument17 SeitenWow Si Ép ÊiGia MinhNoch keine Bewertungen

- Fund SummaryDokument6 SeitenFund SummaryhowellstechNoch keine Bewertungen

- Summary of The Intelligent Investor: by Benjamin Graham and Jason Zweig | Includes AnalysisVon EverandSummary of The Intelligent Investor: by Benjamin Graham and Jason Zweig | Includes AnalysisBewertung: 5 von 5 Sternen5/5 (1)

- Mastering the Art of Investing Using Other People's MoneyVon EverandMastering the Art of Investing Using Other People's MoneyNoch keine Bewertungen

- Guide to Benjamin Graham’s & et al The Intelligent InvestorVon EverandGuide to Benjamin Graham’s & et al The Intelligent InvestorNoch keine Bewertungen

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Von EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Noch keine Bewertungen

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingVon EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNoch keine Bewertungen

- Lessons from Private Equity Any Company Can UseVon EverandLessons from Private Equity Any Company Can UseBewertung: 4.5 von 5 Sternen4.5/5 (12)

- The Dividend Investor: A practical guide to building a share portfolio designed to maximise incomeVon EverandThe Dividend Investor: A practical guide to building a share portfolio designed to maximise incomeNoch keine Bewertungen

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingVon EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingNoch keine Bewertungen

- A Beginner's Guide to Investing: Investing For Tomorrow - Discover Proven Strategies To Trade and Invest In Any Type of MarketVon EverandA Beginner's Guide to Investing: Investing For Tomorrow - Discover Proven Strategies To Trade and Invest In Any Type of MarketNoch keine Bewertungen

- Third Point Q3 2012 Investor Letter TPOIDokument11 SeitenThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCNoch keine Bewertungen

- 8th Annual New York: Value Investing CongressDokument51 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- 8th Annual New York: Value Investing CongressDokument46 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- Ubben ValueInvestingCongress 100212Dokument27 SeitenUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- 8th Annual New York: Value Investing CongressDokument53 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- SHLDDokument18 SeitenSHLDduwe7809100% (1)

- Value Investing Congress Presentation-Tilson-10!1!12Dokument93 SeitenValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCNoch keine Bewertungen

- HP PresentationDokument69 SeitenHP Presentationssc320Noch keine Bewertungen

- Ghazi ValueInvestingCongress 100112Dokument70 SeitenGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- Rockstone Research URS1 EnglishDokument32 SeitenRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDokument8 SeitenGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteNoch keine Bewertungen

- 2012 Third Point Q2 Investor Letter TPOIDokument7 Seiten2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDokument7 Seiten2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Greenlight Q2 Letter To InvestorsDokument5 SeitenGreenlight Q2 Letter To InvestorsVALUEWALK LLCNoch keine Bewertungen

- T2 Accredited Fund Letter To Investors June 12Dokument10 SeitenT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCNoch keine Bewertungen

- Fairholme: Ignore The CrowdDokument13 SeitenFairholme: Ignore The CrowdVALUEWALK LLCNoch keine Bewertungen

- Fairholme: Ignore The CrowdDokument13 SeitenFairholme: Ignore The CrowdVALUEWALK LLCNoch keine Bewertungen

- VALUExVail 2012 James ChanosDokument30 SeitenVALUExVail 2012 James ChanosVALUEWALK LLCNoch keine Bewertungen

- Annual Report: March 31, 2011Dokument23 SeitenAnnual Report: March 31, 2011VALUEWALK LLCNoch keine Bewertungen

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Dokument15 SeitenMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugNoch keine Bewertungen

- Bruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Dokument2 SeitenBruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Luochang YuNoch keine Bewertungen

- ASFL - Quarterly Accounts - September 30, 2011Dokument17 SeitenASFL - Quarterly Accounts - September 30, 2011VALUEWALK LLCNoch keine Bewertungen

- Why We'Re Long J.C. Penney-T2 PartnersDokument18 SeitenWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCNoch keine Bewertungen

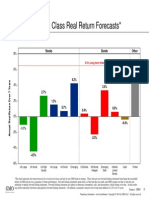

- GMO 7 Year Asset Forecast - Jan 2014Dokument1 SeiteGMO 7 Year Asset Forecast - Jan 2014CanadianValueNoch keine Bewertungen

- To Longleaf Shareholders: Cumulative Returns at December 31, 2011Dokument6 SeitenTo Longleaf Shareholders: Cumulative Returns at December 31, 2011VALUEWALK LLCNoch keine Bewertungen

- Nokia Results2011Q4eDokument60 SeitenNokia Results2011Q4ejunaid112Noch keine Bewertungen

- 4 Simple Volume Trading StrategiesDokument49 Seiten4 Simple Volume Trading StrategiesCharles Barony25% (4)

- New Summer Training Project ReportDokument62 SeitenNew Summer Training Project ReportSagar Bhardwaj100% (1)

- Liquidity Ratio of VodafoneDokument12 SeitenLiquidity Ratio of VodafoneBenjamin Harris100% (1)

- DOW - MOY EffectDokument47 SeitenDOW - MOY EffectRajat AggarwalNoch keine Bewertungen

- Expanding The Indian Equities Market Through ETFsDokument62 SeitenExpanding The Indian Equities Market Through ETFsdanielpolk100% (2)

- 03 Icai Case Study QuestionDokument7 Seiten03 Icai Case Study QuestionFAMLITNoch keine Bewertungen

- Putnam Alternating Market LeadershipDokument2 SeitenPutnam Alternating Market LeadershipPutnam InvestmentsNoch keine Bewertungen

- Contemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test BankDokument19 SeitenContemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test Bankfrederick100% (25)

- Chap 005Dokument11 SeitenChap 005Mohammed FahadNoch keine Bewertungen

- Jarislowsky Fraser International Equity Segregated Fund - 2023 - SepDokument1 SeiteJarislowsky Fraser International Equity Segregated Fund - 2023 - Sepsmartinvest2011Noch keine Bewertungen

- 2778-Article Text-8143-1-10-20191009 PDFDokument22 Seiten2778-Article Text-8143-1-10-20191009 PDFDũng Nguyễn AnhNoch keine Bewertungen

- April2018 1 UnlockedDokument77 SeitenApril2018 1 UnlockedAlok KapoorNoch keine Bewertungen

- Stock and CommDokument11 SeitenStock and CommTed MaragNoch keine Bewertungen

- Storebrand Asa: SelskapsanalyseDokument8 SeitenStorebrand Asa: SelskapsanalyseKristian AndersenNoch keine Bewertungen

- Foreign Ownership Restrictions and Minimum Foreign Headroom RequirementDokument8 SeitenForeign Ownership Restrictions and Minimum Foreign Headroom RequirementJoão Gabriel de Oliveira FreitasNoch keine Bewertungen

- A Practical Handbook On Stock Market TradingDokument105 SeitenA Practical Handbook On Stock Market TradingSudhanshu SinghNoch keine Bewertungen

- Fact-Sheet 20191230 06 Idxg30Dokument1 SeiteFact-Sheet 20191230 06 Idxg30Taqiya NadiyaNoch keine Bewertungen

- Classification of Mutual FundsDokument11 SeitenClassification of Mutual FundsAbhay KumarNoch keine Bewertungen

- Mock 1 - Afternoon - AnswersDokument27 SeitenMock 1 - Afternoon - Answerspagis31861Noch keine Bewertungen

- Intermediate: Futures & ForwardsDokument120 SeitenIntermediate: Futures & ForwardsBurhanudin BurhanudinNoch keine Bewertungen

- Anil Rana ProjectDokument34 SeitenAnil Rana Projectanil ranaNoch keine Bewertungen

- Comparative Study of Mutual FundDokument65 SeitenComparative Study of Mutual Fundsimantt100% (2)

- Mutual FundsDokument35 SeitenMutual FundsDovilė Purickaitė - Koncienė100% (1)

- Ch18 Globalization and International InvestingDokument43 SeitenCh18 Globalization and International InvestingA_StudentsNoch keine Bewertungen

- CourseMarial - Ca11cinvestment Analysis and Portfolio ManagementDokument4 SeitenCourseMarial - Ca11cinvestment Analysis and Portfolio Managementfash selectNoch keine Bewertungen

- Assignment Three: S&P Launches ESG Index For EgyptDokument1 SeiteAssignment Three: S&P Launches ESG Index For EgyptYasser YassinNoch keine Bewertungen

- Equit Alpha Bofa 1julDokument12 SeitenEquit Alpha Bofa 1julgerrich rusNoch keine Bewertungen

- Customer's Perception Towards Equity TradingDokument47 SeitenCustomer's Perception Towards Equity TradingPadam Gupta33% (3)