Das könnte Ihnen auch gefallen

- Corporate Finance Syllabus and Outline: Aswath DamodaranDokument13 SeitenCorporate Finance Syllabus and Outline: Aswath Damodarandreamer4077Noch keine Bewertungen

- FIN 5305 01 Syllabus Aguenaou F 2021Dokument5 SeitenFIN 5305 01 Syllabus Aguenaou F 2021amina ZeroualNoch keine Bewertungen

- UT Dallas Syllabus For Fin6301.502.11s Taught by Arzu Ozoguz (Axo101000)Dokument10 SeitenUT Dallas Syllabus For Fin6301.502.11s Taught by Arzu Ozoguz (Axo101000)UT Dallas Provost's Technology GroupNoch keine Bewertungen

- Fin 320-00 Fall 2022 Online Package R PageNDokument473 SeitenFin 320-00 Fall 2022 Online Package R PageNElijah CarigonNoch keine Bewertungen

- A. Financial Management 13Dokument5 SeitenA. Financial Management 13Honey EditsNoch keine Bewertungen

- Work Program Portfolio 2013Dokument17 SeitenWork Program Portfolio 20132009028818Noch keine Bewertungen

- Case Method of Teaching and Learning by Ahindra ChakrabartiDokument27 SeitenCase Method of Teaching and Learning by Ahindra ChakrabartiParth SanghviNoch keine Bewertungen

- BF R. Kit As at 25 April 2006Dokument255 SeitenBF R. Kit As at 25 April 2006Winny Shiru Machira100% (2)

- Intermediate Finance: Session 1Dokument24 SeitenIntermediate Finance: Session 1rizaunNoch keine Bewertungen

- Corporate Finance SyllabusDokument15 SeitenCorporate Finance SyllabusgosangNoch keine Bewertungen

- Syllabus Gfii 090921 v1 PubDokument6 SeitenSyllabus Gfii 090921 v1 PubJoana MouraNoch keine Bewertungen

- FIN 501 Corporate Finance Course SyllabusDokument4 SeitenFIN 501 Corporate Finance Course SyllabusAmandeep AroraNoch keine Bewertungen

- Fin 301-900 Syllabus W20Dokument12 SeitenFin 301-900 Syllabus W20Sagar PatelNoch keine Bewertungen

- #0 - Syllabus FIN823 Derivatives KEWEI HOUDokument5 Seiten#0 - Syllabus FIN823 Derivatives KEWEI HOUJinsoo YangNoch keine Bewertungen

- The Financial Planning ProcessDokument50 SeitenThe Financial Planning ProcessSHEILA LUMAYGAYNoch keine Bewertungen

- Unit of Study Outline: Corporate Finance IIDokument8 SeitenUnit of Study Outline: Corporate Finance IIsuitup100Noch keine Bewertungen

- 260 sp09 PDFDokument10 Seiten260 sp09 PDFpatternprojectNoch keine Bewertungen

- Finance Homework QuestionsDokument5 SeitenFinance Homework Questionstfrzpxmpd100% (1)

- Synergy Selection GuideDokument3 SeitenSynergy Selection GuideGouravNoch keine Bewertungen

- Cfsyllspr 23Dokument24 SeitenCfsyllspr 23shubhamjob4Noch keine Bewertungen

- Buss & Fin - Day 1Dokument48 SeitenBuss & Fin - Day 1Phill SamonteNoch keine Bewertungen

- Money and Financial Intermediation: Economics/Finance 325Dokument3 SeitenMoney and Financial Intermediation: Economics/Finance 325JohnNoch keine Bewertungen

- Class 1Dokument22 SeitenClass 1Julio PanduroNoch keine Bewertungen

- Financial Accounting SyllabusDokument8 SeitenFinancial Accounting SyllabusCh Bharath KumarNoch keine Bewertungen

- Kuratko 8 e CH 09Dokument24 SeitenKuratko 8 e CH 09waqasNoch keine Bewertungen

- MGT523 SPR (A) DL AY21-22 RequirementDokument7 SeitenMGT523 SPR (A) DL AY21-22 RequirementAbdullahNoch keine Bewertungen

- Corporate Finance What Is It?: Aswath DamodaranDokument14 SeitenCorporate Finance What Is It?: Aswath DamodaranAnshik BansalNoch keine Bewertungen

- CCI Yale ConsultingIndustryDokument20 SeitenCCI Yale ConsultingIndustrynparlanceNoch keine Bewertungen

- Improvement of Entrepreneur:-Meaning of EntrepreneurDokument5 SeitenImprovement of Entrepreneur:-Meaning of EntrepreneurAurang Zeb KhanNoch keine Bewertungen

- Introduction of Organization and Nature of Work: SolutionDokument12 SeitenIntroduction of Organization and Nature of Work: SolutionMohd AlzairuddinNoch keine Bewertungen

- Module in EntrepreneurshipDokument49 SeitenModule in EntrepreneurshipLiezyl AldaveNoch keine Bewertungen

- 415-1x - L00 - Video 3 - Introduction To Modern Finance-EnDokument2 Seiten415-1x - L00 - Video 3 - Introduction To Modern Finance-EnDaveYepestNoch keine Bewertungen

- FIN 600 SyllabusDokument5 SeitenFIN 600 SyllabusJames MeinersNoch keine Bewertungen

- Syllabus Corporate FinanceDokument6 SeitenSyllabus Corporate FinanceTara PNoch keine Bewertungen

- The University of North Carolina at Greensboro Joseph M. Bryan School of Business and Economics Department of Accounting and Finance Fall 2010Dokument10 SeitenThe University of North Carolina at Greensboro Joseph M. Bryan School of Business and Economics Department of Accounting and Finance Fall 2010Louie RamNoch keine Bewertungen

- FIN 301 SyllabusDokument9 SeitenFIN 301 SyllabusAnh NguyenNoch keine Bewertungen

- FNCE101 wk1Dokument51 SeitenFNCE101 wk1Ian ChengNoch keine Bewertungen

- Module 7 Mutual FundsDokument11 SeitenModule 7 Mutual FundsVelante IrafrankNoch keine Bewertungen

- Assessment CentresDokument11 SeitenAssessment Centresauberginesue100% (1)

- VCIC PlaybookDokument19 SeitenVCIC PlaybookKumar Gaurab JhaNoch keine Bewertungen

- Tds ThesisDokument4 SeitenTds Thesismelissamooreportland100% (1)

- Kuratko 8e CH 09Dokument24 SeitenKuratko 8e CH 09BoyNoch keine Bewertungen

- Investment Banking Spring WeeksDokument7 SeitenInvestment Banking Spring WeeksEduardoNoch keine Bewertungen

- Creative Problem Solving: BY: Muhammad UmarDokument31 SeitenCreative Problem Solving: BY: Muhammad UmarMuhammad UmarNoch keine Bewertungen

- Civics and Economics Homework HelpDokument5 SeitenCivics and Economics Homework Helpdbrysbjlf100% (1)

- BMA5008 RV 1213 Sem2Dokument4 SeitenBMA5008 RV 1213 Sem2Adnan ShoaibNoch keine Bewertungen

- MBA Pricing & Markets Course - INSEAD 2016Dokument16 SeitenMBA Pricing & Markets Course - INSEAD 2016apuszNoch keine Bewertungen

- BA 190 Course Outline 0120Dokument9 SeitenBA 190 Course Outline 0120Sophia TayagNoch keine Bewertungen

- Corporate Finance Syllabus and Outline SPRING 2020: Aswath DamodaranDokument23 SeitenCorporate Finance Syllabus and Outline SPRING 2020: Aswath DamodarandghxgfhNoch keine Bewertungen

- Final Paper 1 - SolutionDokument14 SeitenFinal Paper 1 - Solutionishujain007Noch keine Bewertungen

- Finance Homework ProblemsDokument6 SeitenFinance Homework Problemsafmtoolap100% (1)

- Master Thesis Topics in Banking and FinanceDokument6 SeitenMaster Thesis Topics in Banking and Financeelizabethjenkinsatlanta100% (2)

- NUS Business School Investment Course OutlineDokument5 SeitenNUS Business School Investment Course OutlinechocodwinNoch keine Bewertungen

- Syllabus JDM CourseDokument4 SeitenSyllabus JDM CourseAlberto ForteNoch keine Bewertungen

- Ross Casebook 2010Dokument108 SeitenRoss Casebook 2010Archibald_Moore100% (3)

- SyllabusDokument2 SeitenSyllabusprodigymakerNoch keine Bewertungen

- Eng 111 Syllabus PDFDokument3 SeitenEng 111 Syllabus PDFnadimNoch keine Bewertungen

- Employment Tips: A Guide To Navigating Career Success In The Ever-Changing Job MarketVon EverandEmployment Tips: A Guide To Navigating Career Success In The Ever-Changing Job MarketNoch keine Bewertungen

- HBR Guide to Finance Basics for Managers (HBR Guide Series)Von EverandHBR Guide to Finance Basics for Managers (HBR Guide Series)Bewertung: 4.5 von 5 Sternen4.5/5 (18)

- 155 Best Business English Vocabulary TermsVon Everand155 Best Business English Vocabulary TermsBewertung: 3 von 5 Sternen3/5 (2)

- CAPE U1 Partnership Revaluation QuestionsDokument6 SeitenCAPE U1 Partnership Revaluation QuestionsNadine DavidsonNoch keine Bewertungen

- Toa PreboardDokument9 SeitenToa PreboardLeisleiRagoNoch keine Bewertungen

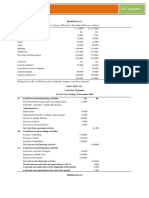

- Cash Flow Statement Problems PDFDokument32 SeitenCash Flow Statement Problems PDFnsrivastav179% (29)

- ReceivablesDokument11 SeitenReceivablesmobylay25% (4)

- Risk Management in Banks, The AHP Way - Diksha AroraDokument29 SeitenRisk Management in Banks, The AHP Way - Diksha AroraDiksha Arora KathuriaNoch keine Bewertungen

- Applied Auditing Chapter08 - AnswerDokument27 SeitenApplied Auditing Chapter08 - AnswerGraceNoch keine Bewertungen

- Stock ResearchDokument50 SeitenStock Researchvikas yadavNoch keine Bewertungen

- Particulars Year Ended 31 March, 2020: Income Statement For Birla Corporation LTDDokument24 SeitenParticulars Year Ended 31 March, 2020: Income Statement For Birla Corporation LTDSomil GuptaNoch keine Bewertungen

- Create A Company in Tally ERP9 and Do The Following Task As Directed:-Create The Following Ledger A/cDokument4 SeitenCreate A Company in Tally ERP9 and Do The Following Task As Directed:-Create The Following Ledger A/cDhrubajyoti SinghaNoch keine Bewertungen

- WEINGARTEN REALTY INVESTORS /TX/ 8-K (Events or Changes Between Quarterly Reports) 2009-02-24Dokument83 SeitenWEINGARTEN REALTY INVESTORS /TX/ 8-K (Events or Changes Between Quarterly Reports) 2009-02-24http://secwatch.comNoch keine Bewertungen

- Mekane Yesus Bulcha Area Local Church Business PlanDokument11 SeitenMekane Yesus Bulcha Area Local Church Business Planpenna belewNoch keine Bewertungen

- QUICKDokument8 SeitenQUICKnissaNoch keine Bewertungen

- Full Disclosure in Financial ReportingDokument22 SeitenFull Disclosure in Financial ReportingIrwan JanuarNoch keine Bewertungen

- Group 6 - Management Control System of Measurement and Control of Managed AssetsDokument25 SeitenGroup 6 - Management Control System of Measurement and Control of Managed AssetsHernawatiNoch keine Bewertungen

- Water StationDokument14 SeitenWater StationPrincess TolentinoNoch keine Bewertungen

- FINAL FABM2 Handouts #3.pdf  Version 1Dokument12 SeitenFINAL FABM2 Handouts #3.pdf  Version 1Kristy Veyna BautistaNoch keine Bewertungen

- Accounting 1101 Midterm Examination 100 PointsDokument7 SeitenAccounting 1101 Midterm Examination 100 PointsRhaizel HernandezNoch keine Bewertungen

- Funding The Business TACN 2 HVTCDokument10 SeitenFunding The Business TACN 2 HVTCNguyễn Lương Minh ChâuNoch keine Bewertungen

- 0452 s03 Ms 2Dokument6 Seiten0452 s03 Ms 2lie chingNoch keine Bewertungen

- SEO-Optimized Multiple Choice Exam QuestionsDokument3 SeitenSEO-Optimized Multiple Choice Exam QuestionsChristian Joy ReyesNoch keine Bewertungen

- Business Solution Enterprise Statement of Financial Position As of December 31, 2018 AssetsDokument4 SeitenBusiness Solution Enterprise Statement of Financial Position As of December 31, 2018 AssetsCheche Casaljay AmpoanNoch keine Bewertungen

- Anisa Muzaqi 4c Lat 22 Castleman Holdings, IncDokument6 SeitenAnisa Muzaqi 4c Lat 22 Castleman Holdings, Incanisa MuzaqiNoch keine Bewertungen

- Sphinx Embedded & It SolutionsDokument8 SeitenSphinx Embedded & It SolutionsJANANI COMPUTERSNoch keine Bewertungen

- Fixed Asset 31122022Dokument1.406 SeitenFixed Asset 31122022kelsykalokiNoch keine Bewertungen

- Devi ProjectDokument56 SeitenDevi Projectdurga deviNoch keine Bewertungen

- F-401 Course Outline BBA 23rd 2020 - EditedDokument1 SeiteF-401 Course Outline BBA 23rd 2020 - EditedtamannaakterNoch keine Bewertungen

- Modul 7 - Financial Distress-1Dokument39 SeitenModul 7 - Financial Distress-1Cornelita Tesalonika R. K.Noch keine Bewertungen

- Financial management toolkit for MFIsDokument45 SeitenFinancial management toolkit for MFIsAndreea Cismaru100% (3)

- Full Download Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions ManualDokument36 SeitenFull Download Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manualcolagiovannibeckah100% (29)

- Chap 007Dokument87 SeitenChap 007dsementsovaNoch keine Bewertungen