Das könnte Ihnen auch gefallen

- 8th Annual New York: Value Investing CongressDokument46 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- Third Point Q3 2012 Investor Letter TPOIDokument11 SeitenThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCNoch keine Bewertungen

- Ubben ValueInvestingCongress 100212Dokument27 SeitenUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- SHLDDokument18 SeitenSHLDduwe7809100% (1)

- Value Investing Congress Presentation-Tilson-10!1!12Dokument93 SeitenValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCNoch keine Bewertungen

- 8th Annual New York: Value Investing CongressDokument51 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- 8th Annual New York: Value Investing CongressDokument53 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- 2012 Third Point Q2 Investor Letter TPOIDokument7 Seiten2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Ghazi ValueInvestingCongress 100112Dokument70 SeitenGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDokument7 Seiten2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- T2 Accredited Fund Letter To Investors June 12Dokument10 SeitenT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCNoch keine Bewertungen

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDokument8 SeitenGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteNoch keine Bewertungen

- Rockstone Research URS1 EnglishDokument32 SeitenRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- Greenlight Q2 Letter To InvestorsDokument5 SeitenGreenlight Q2 Letter To InvestorsVALUEWALK LLCNoch keine Bewertungen

- VALUExVail 2012 James ChanosDokument30 SeitenVALUExVail 2012 James ChanosVALUEWALK LLCNoch keine Bewertungen

- Fairholme: Ignore The CrowdDokument13 SeitenFairholme: Ignore The CrowdVALUEWALK LLCNoch keine Bewertungen

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Dokument15 SeitenMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugNoch keine Bewertungen

- HP PresentationDokument69 SeitenHP Presentationssc320Noch keine Bewertungen

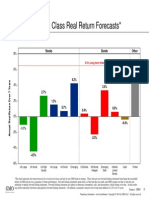

- GMO 7 Year Asset Forecast - Jan 2014Dokument1 SeiteGMO 7 Year Asset Forecast - Jan 2014CanadianValueNoch keine Bewertungen

- Fairholme: Ignore The CrowdDokument13 SeitenFairholme: Ignore The CrowdVALUEWALK LLCNoch keine Bewertungen

- Nokia Results2011Q4eDokument60 SeitenNokia Results2011Q4ejunaid112Noch keine Bewertungen

- Why We'Re Long J.C. Penney-T2 PartnersDokument18 SeitenWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCNoch keine Bewertungen

- Bruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Dokument2 SeitenBruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Luochang YuNoch keine Bewertungen

- Annual Report: March 31, 2011Dokument23 SeitenAnnual Report: March 31, 2011VALUEWALK LLCNoch keine Bewertungen

- Pershing Square Q1 12 Investor LetterDokument14 SeitenPershing Square Q1 12 Investor LetterVALUEWALK LLCNoch keine Bewertungen

- ASFL - Quarterly Accounts - September 30, 2011Dokument17 SeitenASFL - Quarterly Accounts - September 30, 2011VALUEWALK LLCNoch keine Bewertungen

- To Longleaf Shareholders: Cumulative Returns at December 31, 2011Dokument6 SeitenTo Longleaf Shareholders: Cumulative Returns at December 31, 2011VALUEWALK LLCNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Chipotle AnalysisDokument14 SeitenChipotle Analysisscotthnguyen0% (1)

- Chapter 6 Foreign Currency TransactionsDokument10 SeitenChapter 6 Foreign Currency Transactionsfitsum tesfayeNoch keine Bewertungen

- Presentation 4 - Basics of Capital Budgeting (Draft)Dokument27 SeitenPresentation 4 - Basics of Capital Budgeting (Draft)sanjuladasanNoch keine Bewertungen

- Valuation and Financial Forecasting A Handbook For Academics and Practitioners (294 Pages) (Ben Sopranzetti Braun Kiess) (Z-Library)Dokument295 SeitenValuation and Financial Forecasting A Handbook For Academics and Practitioners (294 Pages) (Ben Sopranzetti Braun Kiess) (Z-Library)normando vikingo100% (2)

- Chapter 9 & 10Dokument2 SeitenChapter 9 & 10atikah darayaniNoch keine Bewertungen

- CH10 ... Capital Markets & The Pricing of RiskDokument50 SeitenCH10 ... Capital Markets & The Pricing of RiskMariam AlraeesiNoch keine Bewertungen

- Presentation ON Cash Management OF Ans Steel Tubes Ltd. (JBM Group)Dokument23 SeitenPresentation ON Cash Management OF Ans Steel Tubes Ltd. (JBM Group)soniaNoch keine Bewertungen

- NAL Online Training Program Online Rapid Learning Series-VDokument7 SeitenNAL Online Training Program Online Rapid Learning Series-VKripal SinghNoch keine Bewertungen

- Gold ETFDokument13 SeitenGold ETFஅருள் முருகன்Noch keine Bewertungen

- Roof Tile Project ProfileDokument18 SeitenRoof Tile Project ProfileHendra Samantha100% (1)

- 317 BowicijiwinuqDokument3 Seiten317 BowicijiwinuqHsjsjNoch keine Bewertungen

- Revenue Recognition PoliciesDokument2 SeitenRevenue Recognition PoliciesMohan BishtNoch keine Bewertungen

- Cash Management of NMB Bank PDFDokument74 SeitenCash Management of NMB Bank PDFSantosh ChhetriNoch keine Bewertungen

- Commitment of Traders (COT) Using The COT Report in Forex TradingDokument8 SeitenCommitment of Traders (COT) Using The COT Report in Forex TradingVeljko KerčevićNoch keine Bewertungen

- Ican Journal March 2014Dokument64 SeitenIcan Journal March 2014casarokarNoch keine Bewertungen

- 914010012706577Dokument17 Seiten914010012706577manu santhuNoch keine Bewertungen

- This Study Resource Was: FINANCIAL ASSET AT AMORTIZED COST (Investor or Bondholder)Dokument9 SeitenThis Study Resource Was: FINANCIAL ASSET AT AMORTIZED COST (Investor or Bondholder)Erica CadagoNoch keine Bewertungen

- Department of Business Administration: MVSR Engineering CollegeDokument19 SeitenDepartment of Business Administration: MVSR Engineering CollegeSanjay GoudNoch keine Bewertungen

- Case Study - Marsoft Valuation MethodologyDokument8 SeitenCase Study - Marsoft Valuation MethodologymekulaNoch keine Bewertungen

- 4.2 Marketing PlanningDokument32 Seiten4.2 Marketing Planningavik senguptaNoch keine Bewertungen

- Investment in Associate SBEDokument1 SeiteInvestment in Associate SBEemman neriNoch keine Bewertungen

- Unit 1 Role of Financial Institutions and MarketsDokument11 SeitenUnit 1 Role of Financial Institutions and MarketsGalijang ShampangNoch keine Bewertungen

- Cost of CapitalDokument19 SeitenCost of CapitalADITYA KUMARNoch keine Bewertungen

- A Dissertation On InvestmentDokument108 SeitenA Dissertation On InvestmentPrakash SinghNoch keine Bewertungen

- MIDTERM-MAS Responsibility Accounting Transfer PricingDokument9 SeitenMIDTERM-MAS Responsibility Accounting Transfer PricingbangtansonyeondaNoch keine Bewertungen

- Vision 2020 For India The Financial Sector: Planning CommissionDokument22 SeitenVision 2020 For India The Financial Sector: Planning Commissionarpitasharma_301Noch keine Bewertungen

- Stock Cheat SheetDokument6 SeitenStock Cheat SheetalishaNoch keine Bewertungen

- MFSA Newsletter July 2011Dokument8 SeitenMFSA Newsletter July 2011Andrea DG Markt TraineeNoch keine Bewertungen

- SAR-MAR-210422-1227PM - RR - 034-COPY 1.editedDokument12 SeitenSAR-MAR-210422-1227PM - RR - 034-COPY 1.editedJishnu ChaudhuriNoch keine Bewertungen

- Q1 From The Following Particulars of XYZ Ltd. Prepare The Cash Flow StatementDokument2 SeitenQ1 From The Following Particulars of XYZ Ltd. Prepare The Cash Flow StatementSuvam PatelNoch keine Bewertungen