Das könnte Ihnen auch gefallen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- Methods of LendingDokument2 SeitenMethods of LendingilovesomeoneNoch keine Bewertungen

- Retail LoansDokument3 SeitenRetail LoansMonisha Bhatia0% (1)

- CHAP - 03 - Managing and Pricing Deposit ServicesDokument60 SeitenCHAP - 03 - Managing and Pricing Deposit ServicesTran Thanh NganNoch keine Bewertungen

- Credit Monitoring Module 1 NIBMDokument135 SeitenCredit Monitoring Module 1 NIBMMike100% (1)

- Unit 7 Merchant BankingDokument14 SeitenUnit 7 Merchant BankingSravani RajuNoch keine Bewertungen

- Credit PolicyDokument26 SeitenCredit PolicyNaren Karimikonda100% (1)

- Top 100 Finance Interview Questions With AnswersDokument37 SeitenTop 100 Finance Interview Questions With AnswersIbtissame EL HMIDINoch keine Bewertungen

- Credit Rating ProcessDokument36 SeitenCredit Rating ProcessBhuvi SharmaNoch keine Bewertungen

- Factors, Impact, Symptoms of NPADokument7 SeitenFactors, Impact, Symptoms of NPAMahesh ChandankarNoch keine Bewertungen

- Pre-Sanction Credit ProcessDokument14 SeitenPre-Sanction Credit ProcessSumit Kumar Sharma100% (2)

- Credit Appraisal ProcessDokument19 SeitenCredit Appraisal ProcessVaishnavi khot100% (1)

- An Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankDokument86 SeitenAn Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankAbhinandan SahooNoch keine Bewertungen

- MCQ's - NBFCDokument2 SeitenMCQ's - NBFCZara KhanNoch keine Bewertungen

- Credit Appraisal TechniquesDokument9 SeitenCredit Appraisal TechniquesMragank Dixit0% (2)

- A Loan Sanction Dilemma CaseDokument2 SeitenA Loan Sanction Dilemma CaseSandeep Mishra0% (1)

- Banking ProductsDokument45 SeitenBanking ProductsRAJAN SINGHNoch keine Bewertungen

- Axis Bank: Presented byDokument19 SeitenAxis Bank: Presented byPratyush RathaNoch keine Bewertungen

- Assignment of Management of Working Capital: TopicDokument13 SeitenAssignment of Management of Working Capital: TopicDavinder Singh Banss0% (1)

- ForfeitingDokument18 SeitenForfeitingAchal KhandelwalNoch keine Bewertungen

- Chapter-01 Accounting For Banking CompanyDokument26 SeitenChapter-01 Accounting For Banking CompanyRabbi Ul Apon100% (1)

- CreditDokument20 SeitenCreditnibedita dashNoch keine Bewertungen

- Liability Products of HDFC BankDokument1 SeiteLiability Products of HDFC BankNikhil SinghalNoch keine Bewertungen

- Microfinancial Analysis of J&K Grameen Bank2Dokument99 SeitenMicrofinancial Analysis of J&K Grameen Bank2Ayan NazirNoch keine Bewertungen

- Merchant Banking SyllabusDokument4 SeitenMerchant Banking SyllabusjeganrajrajNoch keine Bewertungen

- Working Capital Finance-Recommendations of Various Committees.Dokument33 SeitenWorking Capital Finance-Recommendations of Various Committees.Ranaque JahanNoch keine Bewertungen

- Assessment of Working Capital Finance 95MIKGBVDokument31 SeitenAssessment of Working Capital Finance 95MIKGBVpankaj_xaviers100% (1)

- Banking Sector of India PresentationDokument30 SeitenBanking Sector of India Presentationvinni vone89% (53)

- Making A Lending DecisionDokument3 SeitenMaking A Lending DecisionSandeep MishraNoch keine Bewertungen

- Questionnaire For BankDokument5 SeitenQuestionnaire For BankRajendra Patidar100% (1)

- Credit Management - IIBFDokument11 SeitenCredit Management - IIBFteju16sy0% (1)

- Treasury Management AssignmentDokument4 SeitenTreasury Management AssignmentJed Bentillo100% (1)

- A Case Study On Credit Appraisal For Working Capital Finance To Small and Medium Enterprises in Bank of IndiaDokument34 SeitenA Case Study On Credit Appraisal For Working Capital Finance To Small and Medium Enterprises in Bank of Indiaarcherselevators0% (1)

- QUESTIONNAIREDokument2 SeitenQUESTIONNAIREshabnampkNoch keine Bewertungen

- Retail Products and Services of State Bank of IndiaDokument81 SeitenRetail Products and Services of State Bank of IndiaNishant Singh50% (2)

- Icici Bank Project Summer Internship Program 2020Dokument45 SeitenIcici Bank Project Summer Internship Program 2020Bhavna PatnaikNoch keine Bewertungen

- Credit AppraisalDokument6 SeitenCredit AppraisalAnjali Angel ThakurNoch keine Bewertungen

- Credit Appraisal PNBDokument48 SeitenCredit Appraisal PNBURMI0% (1)

- Organization StructureDokument1 SeiteOrganization StructureShruti SharmaNoch keine Bewertungen

- RSKMGT Module II Credit Risk CH 1 - Introduction To Credit RiskDokument12 SeitenRSKMGT Module II Credit Risk CH 1 - Introduction To Credit Riskimran khanNoch keine Bewertungen

- Credit Risk Management On HDFC BankDokument17 SeitenCredit Risk Management On HDFC BankAhemad 12Noch keine Bewertungen

- Credit AppraisalDokument89 SeitenCredit AppraisalSkillpro KhammamNoch keine Bewertungen

- HDFC Bank LoansDokument75 SeitenHDFC Bank LoansSahil Sethi100% (2)

- Merchant BankingDokument17 SeitenMerchant BankingRaghavendra.K.A100% (1)

- GB HRMDokument31 SeitenGB HRMmevrick_guy67% (3)

- 12 Chapter 9 - Risk Management in Banks NBFCsDokument4 Seiten12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceNoch keine Bewertungen

- Hand Book On Retail Loan Products PDFDokument78 SeitenHand Book On Retail Loan Products PDFparadise_27Noch keine Bewertungen

- Working Capital of Borrower-Bank of BarodaDokument82 SeitenWorking Capital of Borrower-Bank of BarodaRaj KopadeNoch keine Bewertungen

- Credit Risk ManagementDokument3 SeitenCredit Risk Managementamrut_bNoch keine Bewertungen

- Credit Management in Indian Overseas BankDokument60 SeitenCredit Management in Indian Overseas BankAkash DixitNoch keine Bewertungen

- Questionnaire: Services of Private Sector Banks and Public Sector Bank" I AmDokument4 SeitenQuestionnaire: Services of Private Sector Banks and Public Sector Bank" I Amaxay12_kimcos10Noch keine Bewertungen

- Credit Appraisal and Risk Rating at PNBDokument48 SeitenCredit Appraisal and Risk Rating at PNBAbhay Thakur100% (2)

- THEJASWINI ProjectDokument112 SeitenTHEJASWINI Projectswamy yashuNoch keine Bewertungen

- Importance of CASA DepositsDokument2 SeitenImportance of CASA Depositsvinodkulkarni100% (1)

- QuestionnaireDokument3 SeitenQuestionnaireKarn PandyaNoch keine Bewertungen

- BankingDokument110 SeitenBankingNarcity UzumakiNoch keine Bewertungen

- Chapter 14Dokument20 SeitenChapter 14runawayyyNoch keine Bewertungen

- Chapter 10 1Dokument40 SeitenChapter 10 1William Masterson Shah0% (1)

- Chapter 12Dokument28 SeitenChapter 12Aditi SenNoch keine Bewertungen

- SARBOXDokument16 SeitenSARBOXMahmudur RahmanNoch keine Bewertungen

- Corporate Government PrinciplesDokument16 SeitenCorporate Government PrinciplesMahmudur RahmanNoch keine Bewertungen

- Control and Ownership StructureDokument15 SeitenControl and Ownership StructureMahmudur RahmanNoch keine Bewertungen

- Types of Companies and Corporate PositionsDokument30 SeitenTypes of Companies and Corporate PositionsMahmudur Rahman100% (1)

- 2-Ppt Corporate Governance-Cg DefinitionDokument14 Seiten2-Ppt Corporate Governance-Cg DefinitionMahmudur RahmanNoch keine Bewertungen

- Corporate Governance Models Around The WorldDokument14 SeitenCorporate Governance Models Around The WorldMahmudur Rahman50% (2)

- Code of Corporate Governance in BangladeshDokument11 SeitenCode of Corporate Governance in BangladeshMahmudur RahmanNoch keine Bewertungen

- Myanmar Country ProfileDokument26 SeitenMyanmar Country ProfileMahmudur RahmanNoch keine Bewertungen

- Analysis of Telecommunications IndustryDokument9 SeitenAnalysis of Telecommunications IndustryMahmudur RahmanNoch keine Bewertungen

- Operational Areas of Haque Bistuits LimitedDokument15 SeitenOperational Areas of Haque Bistuits LimitedMahmudur RahmanNoch keine Bewertungen

- 3steps For Effective Communication.Dokument48 Seiten3steps For Effective Communication.Mahmudur Rahman100% (1)

- Developing Effective Communication Skills.Dokument37 SeitenDeveloping Effective Communication Skills.Mahmudur RahmanNoch keine Bewertungen

- Buscomm (1) .PpthiDokument17 SeitenBuscomm (1) .PpthiPrince KumarNoch keine Bewertungen

- Effective Business Communication SkillsDokument22 SeitenEffective Business Communication SkillsMahmudur RahmanNoch keine Bewertungen

- The Financial Statements of Banks and Their Principal CompetitorsDokument30 SeitenThe Financial Statements of Banks and Their Principal CompetitorsMahmudur Rahman100% (4)

- Chapter Four: Establishing New Banks, Branches, Atms, Telephone Services, and Web SitesDokument17 SeitenChapter Four: Establishing New Banks, Branches, Atms, Telephone Services, and Web SitesMahmudur RahmanNoch keine Bewertungen

- The Internal Environment Resources, Capabilities, and Core CompetenciesDokument41 SeitenThe Internal Environment Resources, Capabilities, and Core CompetenciesMahmudur Rahman50% (4)

- Developing Effective Communication SkillDokument21 SeitenDeveloping Effective Communication SkillMahmudur RahmanNoch keine Bewertungen

- Pathways To Supply Chain ExcellenceDokument217 SeitenPathways To Supply Chain ExcellenceMahmudur Rahman100% (3)

- The External EnvironmentOpportunities, Threats, Industry Competition, and Competitor AnalysisDokument51 SeitenThe External EnvironmentOpportunities, Threats, Industry Competition, and Competitor AnalysisMahmudur RahmanNoch keine Bewertungen

- Strategic EntrepreneurshipDokument36 SeitenStrategic EntrepreneurshipMahmudur Rahman100% (1)

- Acquisition and Restructuring StrategiesDokument72 SeitenAcquisition and Restructuring StrategiesMahmudur Rahman100% (2)

- Strategic Management and Strategic CompetitivenessDokument21 SeitenStrategic Management and Strategic CompetitivenessMahmudur RahmanNoch keine Bewertungen

- International StrategyDokument39 SeitenInternational StrategyMahmudur RahmanNoch keine Bewertungen

- An Overview of Banks and Financial Sector Service.Dokument22 SeitenAn Overview of Banks and Financial Sector Service.Mahmudur RahmanNoch keine Bewertungen

- Risk Management For Changing Interest Rates Asset-Liability ManagementDokument28 SeitenRisk Management For Changing Interest Rates Asset-Liability ManagementMahmudur Rahman100% (1)

- Chapter06-1 Measuring PerformanceDokument11 SeitenChapter06-1 Measuring PerformanceMahmudur RahmanNoch keine Bewertungen

- Lead Time in Garment IndustyDokument13 SeitenLead Time in Garment IndustyPraveen Kumar IpsNoch keine Bewertungen

- Value ChainDokument6 SeitenValue ChainMuhammad Akif SarwarNoch keine Bewertungen

- IB B397F 2023 Spring Term T2Dokument19 SeitenIB B397F 2023 Spring Term T2Mohammed Ameer EjazNoch keine Bewertungen

- IFMP Membership FormDokument2 SeitenIFMP Membership FormShahzad AliNoch keine Bewertungen

- Ethical Issues in Advertising in PakistanDokument14 SeitenEthical Issues in Advertising in PakistanOwaisNoch keine Bewertungen

- Resume Felicia AkligoDokument1 SeiteResume Felicia AkligoFallon AshleeNoch keine Bewertungen

- Fuqua Casebook 2010 For Case Interview Practice - MasterTheCaseDokument112 SeitenFuqua Casebook 2010 For Case Interview Practice - MasterTheCaseMasterTheCase.com100% (2)

- Presentation CRMDokument10 SeitenPresentation CRMdchaudharayNoch keine Bewertungen

- Relationship Marketing in The New Economy: Evert GummessonDokument22 SeitenRelationship Marketing in The New Economy: Evert GummessonFreddy Rocky MasonNoch keine Bewertungen

- Masterdata: I) NielsenidDokument4 SeitenMasterdata: I) NielsenidHarry KonnectNoch keine Bewertungen

- International Marketing Semina DurexDokument1 SeiteInternational Marketing Semina DurexThanhHoàiNguyễnNoch keine Bewertungen

- Spoken English Guru Ebook 1 PDFDokument4 SeitenSpoken English Guru Ebook 1 PDFMohd Mudassir AshrafNoch keine Bewertungen

- 2020 Hult Prize SCORECARD PACKAGE PDFDokument11 Seiten2020 Hult Prize SCORECARD PACKAGE PDFFrancisco Javier Rosales RiveraNoch keine Bewertungen

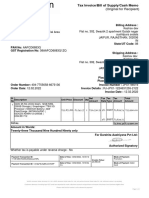

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokument1 SeiteTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)erjasdNoch keine Bewertungen

- The Road Trip - 14.05.2016 - V2Dokument5 SeitenThe Road Trip - 14.05.2016 - V2barkha raniNoch keine Bewertungen

- Introduction To StudyDokument65 SeitenIntroduction To StudyArchana AdavihallimathNoch keine Bewertungen

- Managerial Economics Unit-1Dokument5 SeitenManagerial Economics Unit-1Venkatarathnam NakkaNoch keine Bewertungen

- Case Study On FintechDokument3 SeitenCase Study On FintechTorikul IslamNoch keine Bewertungen

- Jongha-Lim Paper DistressedDokument63 SeitenJongha-Lim Paper DistressedChris TrampeNoch keine Bewertungen

- Agricultural Free Patent Study July 20 2015Dokument23 SeitenAgricultural Free Patent Study July 20 2015Gladys Laureta GarciaNoch keine Bewertungen

- Ask Chuck-Casestudy 1Dokument1 SeiteAsk Chuck-Casestudy 1Phương Ngô QuỳnhNoch keine Bewertungen

- Chapter Four International Marketing Product PolicyDokument53 SeitenChapter Four International Marketing Product PolicyEyob ZekariyasNoch keine Bewertungen

- Marketing Strategy - LaksprayDokument12 SeitenMarketing Strategy - LaksprayChathurika Wijayawardana83% (6)

- Hindustan Unilever LTD.: Trend AnalysisDokument7 SeitenHindustan Unilever LTD.: Trend AnalysisAnkitaBansalNoch keine Bewertungen

- Egyptian Electrical Cables Increases 6.3% in Past YearDokument18 SeitenEgyptian Electrical Cables Increases 6.3% in Past YearAhmed Ali HefnawyNoch keine Bewertungen

- Valuations 1: Introduction To Methods of ValuationDokument17 SeitenValuations 1: Introduction To Methods of ValuationNormande RyanNoch keine Bewertungen

- Kraft and CadburyDokument2 SeitenKraft and CadburyRezaHakimNoch keine Bewertungen

- Market Structure: Firms ProductsDokument4 SeitenMarket Structure: Firms Products여자마비Noch keine Bewertungen

- Marketing Management Assignment Saregama India LTD.: Repositioning The Value PropositionDokument9 SeitenMarketing Management Assignment Saregama India LTD.: Repositioning The Value PropositionPriyansh SinghNoch keine Bewertungen

- SHSQC TuitionDokument1 SeiteSHSQC TuitionroarmikeNoch keine Bewertungen

- Argentina and AustraliaDokument83 SeitenArgentina and Australialectoris100% (1)

- Types of POS SystemsDokument3 SeitenTypes of POS SystemsCabdulahi CumarNoch keine Bewertungen