Das könnte Ihnen auch gefallen

- Management AccountingDokument10 SeitenManagement Accountingnikhilgangwani100% (3)

- Decision Making 36 Practice Questions SolutionsDokument33 SeitenDecision Making 36 Practice Questions SolutionsVias TikaNoch keine Bewertungen

- CVP AnalysisDokument5 SeitenCVP AnalysisAnne BacolodNoch keine Bewertungen

- CH 07 DOitDokument4 SeitenCH 07 DOitHanna DizonNoch keine Bewertungen

- Intermediate Review For Funal Chapter 9-10Dokument11 SeitenIntermediate Review For Funal Chapter 9-10Peter Nguyen0% (1)

- Decision MakingDokument33 SeitenDecision Makingali100% (1)

- Study ProbesDokument48 SeitenStudy ProbesRose VeeNoch keine Bewertungen

- Multinational Business Finance 10th Edition Solution ManualDokument8 SeitenMultinational Business Finance 10th Edition Solution ManualrspkamalgmailcomNoch keine Bewertungen

- MA3 Sample Exams Plus SolutionsDokument89 SeitenMA3 Sample Exams Plus Solutionsbooks_sumiNoch keine Bewertungen

- Sample Interview PlanDokument8 SeitenSample Interview Planpam7779100% (2)

- Reviewer Mas 2Dokument56 SeitenReviewer Mas 2Maria Priencess AcostaNoch keine Bewertungen

- The Great Divide Over Market EfficicnecyDokument10 SeitenThe Great Divide Over Market EfficicnecynamgapNoch keine Bewertungen

- Examples Transfer PricingDokument15 SeitenExamples Transfer PricingRajat RathNoch keine Bewertungen

- Sec A - Group 8Dokument2 SeitenSec A - Group 8SagarNoch keine Bewertungen

- Decision Making 36 Practice Questions & SolutionsDokument33 SeitenDecision Making 36 Practice Questions & SolutionsAbdullah Naeem57% (7)

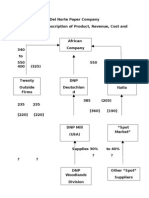

- Del Norte Teaching Note - DiagramDokument3 SeitenDel Norte Teaching Note - Diagramgeorge_eldhoNoch keine Bewertungen

- Select Solutions Zimm 2009 1-5Dokument40 SeitenSelect Solutions Zimm 2009 1-5AdamNoch keine Bewertungen

- 13 - 47, 48Dokument2 Seiten13 - 47, 48Binar Arum NurmawatiNoch keine Bewertungen

- An Individual Assignment For Acc2 For MGMT2Dokument123 SeitenAn Individual Assignment For Acc2 For MGMT2Amanuel GirmaNoch keine Bewertungen

- Sample ExamDokument8 SeitenSample ExamJennifer W.A.Noch keine Bewertungen

- Ch19 Guan Hansen MowenDokument38 SeitenCh19 Guan Hansen MowenratuhsNoch keine Bewertungen

- Agenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingDokument33 SeitenAgenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingApoorvNoch keine Bewertungen

- REquisition and StudiesDokument2 SeitenREquisition and StudiesCHI-SQUARED STATISTICSNoch keine Bewertungen

- Costs and Breakeven SlidesDokument19 SeitenCosts and Breakeven SlidesAnubhuti SharmaNoch keine Bewertungen

- CH 011 AIA 5e PDFDokument7 SeitenCH 011 AIA 5e PDFfaizthemeNoch keine Bewertungen

- Homework - 1 BCAC 423ATRDokument5 SeitenHomework - 1 BCAC 423ATRg6cmqw8ctzNoch keine Bewertungen

- Break Even ChartDokument20 SeitenBreak Even ChartKarim ManjiyaniNoch keine Bewertungen

- Class Note - Chpt12 Decision MakingDokument19 SeitenClass Note - Chpt12 Decision MakingNicole LinNoch keine Bewertungen

- Dynatronics CaseDokument6 SeitenDynatronics CaseScribdTranslationsNoch keine Bewertungen

- CH 5 QuizDokument11 SeitenCH 5 QuizCha Chi BossNoch keine Bewertungen

- A. Calculate The Break-Even Dollar Sales For The MonthDokument25 SeitenA. Calculate The Break-Even Dollar Sales For The MonthMohitNoch keine Bewertungen

- Exam 1 - VI SolutionsDokument9 SeitenExam 1 - VI Solutionssyeda hifzaNoch keine Bewertungen

- Session 08: Tactical Decision MakingDokument18 SeitenSession 08: Tactical Decision MakingFrancisco Pedro SantosNoch keine Bewertungen

- Managerial Accounting Assignment 1 - Model AnswerDokument2 SeitenManagerial Accounting Assignment 1 - Model AnswerYousif Zaki 3100% (1)

- BG 615 Final Exam Three ProblemsDokument3 SeitenBG 615 Final Exam Three ProblemsDoreenNoch keine Bewertungen

- Unit 1Dokument5 SeitenUnit 1Baba Baby NathNoch keine Bewertungen

- Course TitleDokument5 SeitenCourse TitleSolomon G ShNoch keine Bewertungen

- Chapters 8 - 13 - 14 - 15 QuestionsDokument5 SeitenChapters 8 - 13 - 14 - 15 QuestionsJamie N Clint BrendleNoch keine Bewertungen

- Chapter13 Transfer PricingDokument5 SeitenChapter13 Transfer PricingDayan DudosNoch keine Bewertungen

- Questions: TH THDokument4 SeitenQuestions: TH THVivian CácedaNoch keine Bewertungen

- CVP AnalysisDokument16 SeitenCVP AnalysisMustafa ArshadNoch keine Bewertungen

- Long-Term Financial Planning: Plans: Strategic, Operating, and Financial Pro Forma Financial StatementsDokument50 SeitenLong-Term Financial Planning: Plans: Strategic, Operating, and Financial Pro Forma Financial StatementsSyed MohdNoch keine Bewertungen

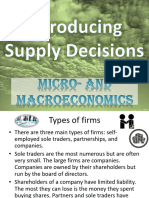

- Micro - and Macroeconomics - 6 - Introducing Supply DecisionsDokument41 SeitenMicro - and Macroeconomics - 6 - Introducing Supply DecisionsPatrick Ajuno SesayNoch keine Bewertungen

- Management Accounting - M1: Examination: Mid TermDokument3 SeitenManagement Accounting - M1: Examination: Mid TermZargham AliNoch keine Bewertungen

- Individual Assignment For Acct For MGMTDokument4 SeitenIndividual Assignment For Acct For MGMTSujib Barman88% (8)

- ACC 302second MidtermDokument8 SeitenACC 302second MidtermvirgofairiesNoch keine Bewertungen

- At 4Dokument7 SeitenAt 4Ley EsguerraNoch keine Bewertungen

- Accounting For The Merchandising Firm Chapter 7Dokument56 SeitenAccounting For The Merchandising Firm Chapter 7Rupesh PolNoch keine Bewertungen

- Mglmod 9Dokument15 SeitenMglmod 9Joyce Anne TilanNoch keine Bewertungen

- ACCT 611 CHP 22BDokument25 SeitenACCT 611 CHP 22BkwameNoch keine Bewertungen

- Budgeting Problem Set SolutionDokument21 SeitenBudgeting Problem Set SolutionJosephThomasNoch keine Bewertungen

- Managerial Accounting 5th Edition Jiambalvo Solutions ManualDokument25 SeitenManagerial Accounting 5th Edition Jiambalvo Solutions Manualnhattranel7k1100% (28)

- Managerial Accounting 6th Edition Jiambalvo Solutions ManualDokument24 SeitenManagerial Accounting 6th Edition Jiambalvo Solutions Manualgenevievetruong9ajpr100% (28)

- Break Even AnalysisDokument4 SeitenBreak Even AnalysisOwen Hudson0% (1)

- Summary Multiple Steps Income Statements & ExercisesDokument19 SeitenSummary Multiple Steps Income Statements & ExercisesrayNoch keine Bewertungen

- Mansci ProblemsDokument6 SeitenMansci ProblemsRojun Kristufer MedenillaNoch keine Bewertungen

- OEM Paints & Finishes World Summary: Market Sector Values & Financials by CountryVon EverandOEM Paints & Finishes World Summary: Market Sector Values & Financials by CountryNoch keine Bewertungen

- Clay Refractory Products World Summary: Market Sector Values & Financials by CountryVon EverandClay Refractory Products World Summary: Market Sector Values & Financials by CountryNoch keine Bewertungen

- Inboard-Outdrive Boats World Summary: Market Sector Values & Financials by CountryVon EverandInboard-Outdrive Boats World Summary: Market Sector Values & Financials by CountryNoch keine Bewertungen

- Agents & Brokers, Durable Goods Revenues World Summary: Market Values & Financials by CountryVon EverandAgents & Brokers, Durable Goods Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Introduction to Business English (Words and Their Secrets)Von EverandIntroduction to Business English (Words and Their Secrets)Noch keine Bewertungen

- Piece Goods, Notions, Dry Good Wholesale Revenues World Summary: Market Values & Financials by CountryVon EverandPiece Goods, Notions, Dry Good Wholesale Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Millwork World Summary: Market Values & Financials by CountryVon EverandMillwork World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- What Are Pricing Techniques: The Pricing Method You Select Provides Direction On How To Set Your Product PriceDokument24 SeitenWhat Are Pricing Techniques: The Pricing Method You Select Provides Direction On How To Set Your Product Pricepam7779Noch keine Bewertungen

- College CatalogDokument206 SeitenCollege Catalogpam7779Noch keine Bewertungen

- College CatalogDokument206 SeitenCollege Catalogpam7779Noch keine Bewertungen

- What Are Pricing Techniques: The Pricing Method You Select Provides Direction On How To Set Your Product PriceDokument24 SeitenWhat Are Pricing Techniques: The Pricing Method You Select Provides Direction On How To Set Your Product Pricepam7779Noch keine Bewertungen

- Business Week (2009-09-14)Dokument84 SeitenBusiness Week (2009-09-14)pam7779Noch keine Bewertungen

- Interview Skills TutorialDokument19 SeitenInterview Skills Tutorialpam7779Noch keine Bewertungen

- Interview Skills TutorialDokument19 SeitenInterview Skills Tutorialpam7779Noch keine Bewertungen

- Customer Insight ToolkitDokument33 SeitenCustomer Insight Toolkitpam7779100% (1)

- Consultant Nation - NYTimesDokument5 SeitenConsultant Nation - NYTimespam7779Noch keine Bewertungen

- Heteroskedasticity and Autocorrelation Consistent Standard ErrorsDokument33 SeitenHeteroskedasticity and Autocorrelation Consistent Standard Errorspam7779Noch keine Bewertungen

- Cargill - Inside The Quiet Giant That Rules The Food Business - Oct. 27, 2011Dokument8 SeitenCargill - Inside The Quiet Giant That Rules The Food Business - Oct. 27, 2011pam7779Noch keine Bewertungen

- Turning A Global Epidemic Into A Business OpportunityDokument10 SeitenTurning A Global Epidemic Into A Business Opportunitypam7779Noch keine Bewertungen

- Barco CaseDokument9 SeitenBarco CaseMamud DakoNoch keine Bewertungen

- Subsecretaría de Educación Básica Coordinación de Idiomas CICLO ESCOLAR 2020-2021Dokument17 SeitenSubsecretaría de Educación Básica Coordinación de Idiomas CICLO ESCOLAR 2020-2021Daniel IbarraNoch keine Bewertungen

- Argus-Phosphate - Phosphoric Acid Price Metholodogy PDFDokument11 SeitenArgus-Phosphate - Phosphoric Acid Price Metholodogy PDFsharemwNoch keine Bewertungen

- Mungerspeech June 95Dokument21 SeitenMungerspeech June 95caitlynharveyNoch keine Bewertungen

- Maths Book 2 FinalDokument18 SeitenMaths Book 2 FinalAjal P100% (1)

- Agile Analytics - Peer-Reviewed Assignment (Coursera)Dokument6 SeitenAgile Analytics - Peer-Reviewed Assignment (Coursera)Felipe LordãoNoch keine Bewertungen

- Reviewer in Marketing ManagementDokument16 SeitenReviewer in Marketing ManagementMarc Myer De AsisNoch keine Bewertungen

- Fac22a2 SuppDokument11 SeitenFac22a2 Suppsacey20.hbNoch keine Bewertungen

- A Case Study of Tesco PLC - UKDokument17 SeitenA Case Study of Tesco PLC - UKsaleem razaNoch keine Bewertungen

- MCS - First Visayas Holding Company - LT9Dokument4 SeitenMCS - First Visayas Holding Company - LT9Apoorv SinghalNoch keine Bewertungen

- Determinants of Interest RatesDokument42 SeitenDeterminants of Interest RatesJigar LakhaniNoch keine Bewertungen

- Tender For Tamping MachineDokument90 SeitenTender For Tamping MachineMasood Ahmad NajarNoch keine Bewertungen

- Amzn1.Tortuga.3.Bc55a94a 9d6d 4883 A54c 888faa4c62c0.T23B1PWXCPIVJPDokument392 SeitenAmzn1.Tortuga.3.Bc55a94a 9d6d 4883 A54c 888faa4c62c0.T23B1PWXCPIVJPJyoti ThakurNoch keine Bewertungen

- Atlantic ComputersDokument14 SeitenAtlantic ComputersRohit KumarNoch keine Bewertungen

- Marketing Case StudyDokument7 SeitenMarketing Case StudySuraj ShiwakotiNoch keine Bewertungen

- General Terms and Conditions of Business of Cleverbridge AGDokument8 SeitenGeneral Terms and Conditions of Business of Cleverbridge AGRashid SaidNoch keine Bewertungen

- Chapter # 8Dokument17 SeitenChapter # 8Rooh Ullah KhanNoch keine Bewertungen

- Model Question Financial Accounting - IIDokument3 SeitenModel Question Financial Accounting - IIEswari Gk100% (1)

- British AirwaysDokument29 SeitenBritish AirwaysAddy D'silva0% (1)

- Customer SatisfactionDokument45 SeitenCustomer Satisfactionsohaib638100% (1)

- Chapter 10 Testbank Used For Online QuizzesDokument57 SeitenChapter 10 Testbank Used For Online QuizzesTrinh Lê100% (1)

- Economic Survey of Maharashtra 2016-17Dokument306 SeitenEconomic Survey of Maharashtra 2016-17Ssk KumarNoch keine Bewertungen

- Principles of Economics Australia and New Zealand 6th Edition Gans Test BankDokument29 SeitenPrinciples of Economics Australia and New Zealand 6th Edition Gans Test Bankjclarku7100% (17)

- Strategy and Competitive AdvantageDokument23 SeitenStrategy and Competitive AdvantageshaieeeeeeNoch keine Bewertungen

- Marco Island ALPRs Purchase Order 210177 - Nov. 2020Dokument6 SeitenMarco Island ALPRs Purchase Order 210177 - Nov. 2020Omar Rodriguez OrtizNoch keine Bewertungen

- Topic 6 MARKETINGDokument42 SeitenTopic 6 MARKETINGlolipopzeeNoch keine Bewertungen

- Reply To EnquiryDokument15 SeitenReply To EnquiryluhsukertiNoch keine Bewertungen

- Forward Contracts Prohibitions On PDFDokument23 SeitenForward Contracts Prohibitions On PDFIqbal PramaditaNoch keine Bewertungen

- Mikias PaperDokument60 SeitenMikias PaperMeadot MikiasNoch keine Bewertungen