Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- A Study On Consumer's Perception For Life Insurance PoliciesDokument63 SeitenA Study On Consumer's Perception For Life Insurance PoliciesBANTYNoch keine Bewertungen

- Classification of Insurance BusinessDokument67 SeitenClassification of Insurance BusinessAarthee Sundaram100% (1)

- MOCK EXAM: Insurance Commission: Module 1 - Principles of Life InsuranceDokument25 SeitenMOCK EXAM: Insurance Commission: Module 1 - Principles of Life InsuranceTGiF TravelNoch keine Bewertungen

- M9 EMockDokument23 SeitenM9 EMockjjjj0% (1)

- Sample Solved Question Papers For IRDA 50 Hours Agents Training ExamDokument15 SeitenSample Solved Question Papers For IRDA 50 Hours Agents Training ExamPurnendu Sarkar75% (4)

- Great Pacific Life Insurance v. CADokument2 SeitenGreat Pacific Life Insurance v. CAErxha LadoNoch keine Bewertungen

- IC VAR LIFE - Reviewer With Answer KeyDokument15 SeitenIC VAR LIFE - Reviewer With Answer KeyDalton Jay LuzaNoch keine Bewertungen

- VUL Mock ExamDokument5 SeitenVUL Mock ExamMillet Plaza Abrigo93% (14)

- Rap Exam Question Paper Model 2Dokument28 SeitenRap Exam Question Paper Model 2Hemant Dhande40% (10)

- A Research Project ON: "Comparative Study of HDFC Standard Life Insurance Co. With Icici & Lic."Dokument90 SeitenA Research Project ON: "Comparative Study of HDFC Standard Life Insurance Co. With Icici & Lic."Nagar PawanNoch keine Bewertungen

- Guaranteed Income GoalDokument6 SeitenGuaranteed Income GoalNeelamani SamalNoch keine Bewertungen

- My Project On UlipsDokument83 SeitenMy Project On UlipsAlok KumarNoch keine Bewertungen

- Absa Global Growth Basket InvestmentDokument21 SeitenAbsa Global Growth Basket Investmentmarko joosteNoch keine Bewertungen

- Consumer Awareness Towards Insurance ProductsDokument86 SeitenConsumer Awareness Towards Insurance ProductsMohit kolliNoch keine Bewertungen

- Guaranteed Income GoalDokument6 SeitenGuaranteed Income Goalsb RogerdatNoch keine Bewertungen

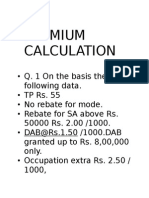

- 2.5 Premmium CalculationDokument21 Seiten2.5 Premmium Calculationashutosh kumarNoch keine Bewertungen

- Amit by Life Insurance FinalDokument6 SeitenAmit by Life Insurance FinalFozle Rabby 182-11-5893Noch keine Bewertungen

- POSTAL LIFE INSURANCE Ppt-PrintDokument17 SeitenPOSTAL LIFE INSURANCE Ppt-PrintPranav Choudhary100% (1)

- Project Report ON: University of MumbaiDokument55 SeitenProject Report ON: University of MumbaiNayak SandeshNoch keine Bewertungen

- Premium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDokument23 SeitenPremium Calculation: Juhi Sharma Rajat Gupta Deepak SinghDeepak SinghNoch keine Bewertungen

- Summer Training Project Report On Study of Life Insurance PoliciesDokument88 SeitenSummer Training Project Report On Study of Life Insurance PoliciesSatish Sandhu0% (1)

- Idbi Federal InsuranceDokument37 SeitenIdbi Federal InsuranceJanani Rani100% (1)

- English Top 200 QuestionsDokument20 SeitenEnglish Top 200 Questionsmarutijadhav2506Noch keine Bewertungen

- Appertaining Thereto or Connected Therewith (Sec. 181) - Life Insurance CoversDokument10 SeitenAppertaining Thereto or Connected Therewith (Sec. 181) - Life Insurance CoversPaulo VillarinNoch keine Bewertungen

- Which Statement Regarding The Risk of Investment in Variable Life Is TRUEDokument2 SeitenWhich Statement Regarding The Risk of Investment in Variable Life Is TRUEFranz JosephNoch keine Bewertungen

- Chap 5Dokument18 SeitenChap 5yhikmet613Noch keine Bewertungen

- VL Mock Exam Set 1Dokument12 SeitenVL Mock Exam Set 1Arvin AltamiaNoch keine Bewertungen

- 4.2. InsuranceDokument11 Seiten4.2. InsuranceThobo PeterNoch keine Bewertungen

- Meghna Life InsuranceDokument20 SeitenMeghna Life InsuranceSadman Shariar Biswas100% (1)

- Life Insurance Linked With InvestmentDokument14 SeitenLife Insurance Linked With InvestmentWyatt HurleyNoch keine Bewertungen