Das könnte Ihnen auch gefallen

- Business Skills: Finance, Money Management, and MarketingVon EverandBusiness Skills: Finance, Money Management, and MarketingNoch keine Bewertungen

- Short-Term Investments and ReceivablesDokument55 SeitenShort-Term Investments and ReceivablesBookAddict721Noch keine Bewertungen

- Cambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersVon EverandCambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersBewertung: 2 von 5 Sternen2/5 (4)

- Accounting Lecture V HandoutsDokument34 SeitenAccounting Lecture V HandoutsКамилла МолдалиеваNoch keine Bewertungen

- Business Skills: Money Management, Accounting, and Communication for Small BusinessesVon EverandBusiness Skills: Money Management, Accounting, and Communication for Small BusinessesNoch keine Bewertungen

- Ac101 ch7Dokument15 SeitenAc101 ch7infinite_dreamsNoch keine Bewertungen

- Accounting 101 Chapter 7 - Accounts and Notes Receivable Prof. JohnsonDokument6 SeitenAccounting 101 Chapter 7 - Accounts and Notes Receivable Prof. JohnsonbikilahussenNoch keine Bewertungen

- Unit 9Dokument5 SeitenUnit 9Anonymous Fn7Ko5riKTNoch keine Bewertungen

- Accounts ReceivableDokument21 SeitenAccounts ReceivableMurtaza Hussain SyedNoch keine Bewertungen

- Chapter 06 PDFDokument21 SeitenChapter 06 PDFnsfaheemNoch keine Bewertungen

- Chapter 9Dokument45 SeitenChapter 9mziabdNoch keine Bewertungen

- Chapter 7Dokument39 SeitenChapter 7juls100% (1)

- Notes 08Dokument11 SeitenNotes 08FantayNoch keine Bewertungen

- Financial AccountingDokument66 SeitenFinancial AccountingFaisal SaleemNoch keine Bewertungen

- TopiC 5 (2) Asset - CA Receivables - ADDTNLDokument14 SeitenTopiC 5 (2) Asset - CA Receivables - ADDTNLPrince RyanNoch keine Bewertungen

- ACC101 Chapter7new PDFDokument23 SeitenACC101 Chapter7new PDFJana Kryzl DibdibNoch keine Bewertungen

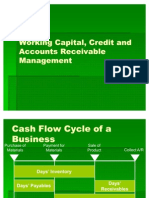

- Working Capital, Credit and Accounts Receivable ManagementDokument31 SeitenWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNoch keine Bewertungen

- Accounting For Receivables PDFDokument23 SeitenAccounting For Receivables PDFjess calderonNoch keine Bewertungen

- 05 ReceivablesDokument15 Seiten05 ReceivablesJean BritoNoch keine Bewertungen

- Accounts Receivable ManagementDokument21 SeitenAccounts Receivable ManagementNeris SaturdayNoch keine Bewertungen

- Welcomeback: Workshop SixDokument55 SeitenWelcomeback: Workshop SixLeah StonesNoch keine Bewertungen

- Lecture On Nature of ReceivablesDokument3 SeitenLecture On Nature of ReceivablesSara AlbinaNoch keine Bewertungen

- Accounting For ReceivablesDokument23 SeitenAccounting For ReceivablesFelekePhiliphosNoch keine Bewertungen

- Accounts Receivable Inventory Management - .DocmDokument11 SeitenAccounts Receivable Inventory Management - .DocmellishNoch keine Bewertungen

- Accounts Receivables and Payables A&BDokument9 SeitenAccounts Receivables and Payables A&BAb PiousNoch keine Bewertungen

- ACC 255 08 OutlineDokument9 SeitenACC 255 08 Outlineadi zilbrshtiinNoch keine Bewertungen

- 3311 Class 11 GSDokument19 Seiten3311 Class 11 GSkatharine1981100% (2)

- Accounts Receivable and Notes Receivable Chapter 6Dokument47 SeitenAccounts Receivable and Notes Receivable Chapter 6Rupesh PolNoch keine Bewertungen

- Warren SM Ch.09 FinalDokument23 SeitenWarren SM Ch.09 FinalAA BB MMNoch keine Bewertungen

- Monitoring of Credit and Collection FundsDokument24 SeitenMonitoring of Credit and Collection FundsADALIA BEATRIZ ONGNoch keine Bewertungen

- IFA Chapter 3Dokument97 SeitenIFA Chapter 3kqk07829Noch keine Bewertungen

- 08 Notes Accounts ReceivableDokument3 Seiten08 Notes Accounts ReceivablePeter KoprdaNoch keine Bewertungen

- Account Recivable Bet Teacher NoteDokument39 SeitenAccount Recivable Bet Teacher NoteHaftom YitbarekNoch keine Bewertungen

- Topic 9 (Part 1) SolutionsDokument8 SeitenTopic 9 (Part 1) SolutionsLiang BochengNoch keine Bewertungen

- Acc CH 4Dokument15 SeitenAcc CH 4Bicaaqaa M. AbdiisaaNoch keine Bewertungen

- CH07Dokument32 SeitenCH07asflkhaf2Noch keine Bewertungen

- Chap 1 Acct For ReceivablesDokument34 SeitenChap 1 Acct For ReceivablesEthiopia NismNoch keine Bewertungen

- Particulars Amount Amount Rs. (DR.) Rs. (DR.)Dokument14 SeitenParticulars Amount Amount Rs. (DR.) Rs. (DR.)Alka DwivediNoch keine Bewertungen

- Receivables: Credit Standards, Length of Credit Period, Cash Discount, Discount Period EtcDokument7 SeitenReceivables: Credit Standards, Length of Credit Period, Cash Discount, Discount Period EtcKristine RazonabeNoch keine Bewertungen

- Net Credit Sales: August 19, 2017Dokument10 SeitenNet Credit Sales: August 19, 2017Armira Rodriguez ConchaNoch keine Bewertungen

- ReceivableDokument24 SeitenReceivableMaria MushtaqueNoch keine Bewertungen

- Week 5: Revenue Recognition and ReceivablesDokument24 SeitenWeek 5: Revenue Recognition and ReceivablesKapil GoyalNoch keine Bewertungen

- C4 Alternative Receivables Collection TechniquesDokument7 SeitenC4 Alternative Receivables Collection TechniquesTENGKU ANIS TENGKU YUSMANoch keine Bewertungen

- Acc CH 4Dokument16 SeitenAcc CH 4Tajudin Abba RagooNoch keine Bewertungen

- Test 3 Fall Section HADokument5 SeitenTest 3 Fall Section HAVin JohnNoch keine Bewertungen

- Budjet and PlannigDokument10 SeitenBudjet and Plannigprakash009kNoch keine Bewertungen

- Aging Schedule Chap 8Dokument4 SeitenAging Schedule Chap 8Uno HajimeNoch keine Bewertungen

- Reimers Finacct03 Sm04Dokument46 SeitenReimers Finacct03 Sm04Maxime HinnekensNoch keine Bewertungen

- Accounting Ratio PDFDokument10 SeitenAccounting Ratio PDFMuhammad KaleemNoch keine Bewertungen

- 2011 Aug Tutorial 10 Working Capital ManagementDokument10 Seiten2011 Aug Tutorial 10 Working Capital ManagementHarmony TeeNoch keine Bewertungen

- Chapter 7 SolutionsDokument64 SeitenChapter 7 SolutionssevtenNoch keine Bewertungen

- Accounts Receivable ManagementDokument3 SeitenAccounts Receivable ManagementzadarunNoch keine Bewertungen

- Accounts ReceivableDokument9 SeitenAccounts ReceivableTrang LeNoch keine Bewertungen

- Akuntansi Bab9Dokument7 SeitenAkuntansi Bab9AKT21Yola Jovita SilabanNoch keine Bewertungen

- ReceivablesDokument61 SeitenReceivablesJeanetteNoch keine Bewertungen

- Accounting Principles 2: Mr. Mohammed AliDokument43 SeitenAccounting Principles 2: Mr. Mohammed AliramiNoch keine Bewertungen

- Excellence in Financial ManagementDokument196 SeitenExcellence in Financial ManagementaimanahmadNoch keine Bewertungen

- Stern CorporationsDokument30 SeitenStern CorporationsShubham MallikNoch keine Bewertungen

- Chapter 3 ReceivablesDokument22 SeitenChapter 3 ReceivablesCale Robert RascoNoch keine Bewertungen

- RecivablesDokument20 SeitenRecivableszynab123Noch keine Bewertungen

- Bank Reconciliation: Everett Community College Tutoring CenterDokument3 SeitenBank Reconciliation: Everett Community College Tutoring Centerehab_ghazallaNoch keine Bewertungen

- 1.5 Scatter Plots and Least Squares LinesDokument6 Seiten1.5 Scatter Plots and Least Squares Linesehab_ghazallaNoch keine Bewertungen

- Chapter 11 Corporations: Organization, Capital Stock Transactions, and DividendsDokument12 SeitenChapter 11 Corporations: Organization, Capital Stock Transactions, and Dividendsehab_ghazallaNoch keine Bewertungen

- Bank ReconciliationDokument21 SeitenBank Reconciliationehab_ghazallaNoch keine Bewertungen

- CH 03Dokument35 SeitenCH 03ehab_ghazallaNoch keine Bewertungen

- 2printable Flash CardsDokument5 Seiten2printable Flash Cardsehab_ghazallaNoch keine Bewertungen

- The Type of Logical Database Model That Treats Data As If They Were Stored in TwoDokument2 SeitenThe Type of Logical Database Model That Treats Data As If They Were Stored in Twoehab_ghazallaNoch keine Bewertungen

- Preparing a bank reconciliation and journal entries (20鈥�25 min) P7 ...Dokument5 SeitenPreparing a bank reconciliation and journal entries (20鈥�25 min) P7 ...ehab_ghazallaNoch keine Bewertungen

- VVVV ImpIT Answers Week 3Dokument7 SeitenVVVV ImpIT Answers Week 3ehab_ghazallaNoch keine Bewertungen

- Problem Set 4Dokument9 SeitenProblem Set 4ehab_ghazallaNoch keine Bewertungen

- My ch04Dokument44 SeitenMy ch04ehab_ghazallaNoch keine Bewertungen

- BankrecDokument24 SeitenBankrecehab_ghazallaNoch keine Bewertungen

- Chapter 12 SolutionsDokument9 SeitenChapter 12 Solutionsehab_ghazallaNoch keine Bewertungen

- Principles of Management MidteDokument7 SeitenPrinciples of Management Midteehab_ghazallaNoch keine Bewertungen

- Introducción A Las MicrofinanzasDokument21 SeitenIntroducción A Las MicrofinanzasNitzia VazquezNoch keine Bewertungen

- Evaluation Form SupervisorsDokument8 SeitenEvaluation Form Supervisorsnitesh2891Noch keine Bewertungen

- ACC 505 Case Study 1Dokument6 SeitenACC 505 Case Study 1Vitor QueirozNoch keine Bewertungen

- Dissertation ReportDokument94 SeitenDissertation ReportgaryrinkuNoch keine Bewertungen

- Angel Broking Project Report Copy AviDokument76 SeitenAngel Broking Project Report Copy AviAvi Solanki100% (2)

- Business English IDokument171 SeitenBusiness English ISofija100% (2)

- The Political Implications of The Peer To Peer Revolution - BawensDokument10 SeitenThe Political Implications of The Peer To Peer Revolution - BawenskosmasgNoch keine Bewertungen

- Customer Relationship Management: Summer Internship ProjectDokument16 SeitenCustomer Relationship Management: Summer Internship ProjectSoniNitinNoch keine Bewertungen

- (John O' Connor, Eamonn Galvin, Martin Evans) (UTS)Dokument454 Seiten(John O' Connor, Eamonn Galvin, Martin Evans) (UTS)Fahmi Alfaroqi100% (1)

- Oracle InventoryDokument207 SeitenOracle InventorySandeep Sharma100% (1)

- Shekhar - Business Ecosystem Analysis For Strategic Decision MakingDokument82 SeitenShekhar - Business Ecosystem Analysis For Strategic Decision MakingTuladhar LindaNoch keine Bewertungen

- CV Victor Morales English 2016 V4Dokument3 SeitenCV Victor Morales English 2016 V4Juan C Ramirez FloresNoch keine Bewertungen

- En HaynesPro Newsletter 20140912Dokument8 SeitenEn HaynesPro Newsletter 20140912A-c RoNoch keine Bewertungen

- Food Laws and RegulationsDokument8 SeitenFood Laws and RegulationsGajendra Singh RaghavNoch keine Bewertungen

- SAP SD Transaction Codes and TablesDokument5 SeitenSAP SD Transaction Codes and TablesKhitish RishiNoch keine Bewertungen

- Generator Service 0750614536Dokument3 SeitenGenerator Service 0750614536Digital pallet weighing scales in Kampala UgandaNoch keine Bewertungen

- Entrepreneurship Development ProgrammeDokument10 SeitenEntrepreneurship Development ProgrammeJitendra KoliNoch keine Bewertungen

- 02kertas Keja BB FixDokument23 Seiten02kertas Keja BB FixFanjili Gratia MamontoNoch keine Bewertungen

- Gates Piaggio GP 180Dokument2 SeitenGates Piaggio GP 180aeroengineer1100% (1)

- 2018 9 Audit Observations and RecommendationsDokument76 Seiten2018 9 Audit Observations and RecommendationsMOTC INTERNAL AUDIT SECTIONNoch keine Bewertungen

- Tendernotice 1Dokument116 SeitenTendernotice 1Abhinav GNoch keine Bewertungen

- Dish TVDokument8 SeitenDish TVLekh RajNoch keine Bewertungen

- At The Hotel - BusuuDokument5 SeitenAt The Hotel - BusuuAida TeskeredžićNoch keine Bewertungen

- Audit of InventoryDokument9 SeitenAudit of InventoryEliyah JhonsonNoch keine Bewertungen

- Butlers ChocolatesDokument2 SeitenButlers ChocolatesIshita JainNoch keine Bewertungen

- Ak - Keu (Problem)Dokument51 SeitenAk - Keu (Problem)RAMA100% (9)

- HUNGERDokument1 SeiteHUNGERA3 VenturesNoch keine Bewertungen

- Group4 Report - Managerial EconomicsDokument37 SeitenGroup4 Report - Managerial EconomicsThuyDuongNoch keine Bewertungen

- Marketing Cas StudyDokument4 SeitenMarketing Cas StudyRejitha RamanNoch keine Bewertungen

- 2007A-MKTG754002-d95a1f85 - Syllabus 5Dokument7 Seiten2007A-MKTG754002-d95a1f85 - Syllabus 5Yashita VoNoch keine Bewertungen