Das könnte Ihnen auch gefallen

- Cost Volume Profit Analysis Review NotesDokument17 SeitenCost Volume Profit Analysis Review NotesAlexis Kaye DayagNoch keine Bewertungen

- Lending and Borrowing in The Financial SystemDokument4 SeitenLending and Borrowing in The Financial Systemtekalign100% (2)

- MATERIAL # 9 - (Code of Ethics) Code of EthicsDokument6 SeitenMATERIAL # 9 - (Code of Ethics) Code of EthicsGlessey Mae Baito LuvidicaNoch keine Bewertungen

- Ias 28: Investment in Associates and Joint VenturesDokument7 SeitenIas 28: Investment in Associates and Joint VenturesDzulija TalipanNoch keine Bewertungen

- Managerial (Cost) Accounting Chapter's LecutersDokument710 SeitenManagerial (Cost) Accounting Chapter's LecutersMuhammad Fahim Khan100% (1)

- Distance Learning Module Advanced Taxation CFM-300 PDFDokument128 SeitenDistance Learning Module Advanced Taxation CFM-300 PDFKafonyi John100% (1)

- 9 Hostile TakeoverDokument35 Seiten9 Hostile TakeoverApril Angel Mateo MaribbayNoch keine Bewertungen

- 1.1 Assignment1 Internal Audit and The Audit Committee and Types of AuditDokument4 Seiten1.1 Assignment1 Internal Audit and The Audit Committee and Types of AuditXexiannaNoch keine Bewertungen

- Auditing I CH 6Dokument9 SeitenAuditing I CH 6Abrha636Noch keine Bewertungen

- Chapter 16 ProblemsDokument4 SeitenChapter 16 ProblemsOkiNoch keine Bewertungen

- IAS37Dokument2 SeitenIAS37Mohammad Faisal SaleemNoch keine Bewertungen

- Branch Accounting 1Dokument36 SeitenBranch Accounting 1Efa Agus100% (3)

- SarbanesDokument16 SeitenSarbanessreedhar72Noch keine Bewertungen

- FM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFDokument28 SeitenFM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFvasantharao100% (1)

- Ifrs at A Glance IFRS 15 Revenue From Contracts: With CustomersDokument7 SeitenIfrs at A Glance IFRS 15 Revenue From Contracts: With CustomersManoj GNoch keine Bewertungen

- Audit of InventoryDokument11 SeitenAudit of InventoryMr.AccntngNoch keine Bewertungen

- Ra 1405Dokument2 SeitenRa 1405Ron Ico RamosNoch keine Bewertungen

- Chapter 4 SolutionsDokument85 SeitenChapter 4 SolutionssevtenNoch keine Bewertungen

- Consolidation GAAPDokument77 SeitenConsolidation GAAPMisganaw DebasNoch keine Bewertungen

- IT-Audit Team2Dokument1 SeiteIT-Audit Team2Von Andrei MedinaNoch keine Bewertungen

- Module 1 Practice QuestionsDokument7 SeitenModule 1 Practice QuestionsEllah MaeNoch keine Bewertungen

- Chapter 18 Policies Estimates and ErrorsDokument28 SeitenChapter 18 Policies Estimates and ErrorsHammad Ahmad100% (1)

- Installment SalesDokument18 SeitenInstallment SaleswaqtawanNoch keine Bewertungen

- Sample Study Guide Chapter 05Dokument12 SeitenSample Study Guide Chapter 05AgentSkySkyNoch keine Bewertungen

- Ifrs 3Dokument4 SeitenIfrs 3Ken ZafraNoch keine Bewertungen

- Source Document of AccountancyDokument7 SeitenSource Document of AccountancyVinod GandhiNoch keine Bewertungen

- Vouching SummaryDokument7 SeitenVouching SummarySonu SawantNoch keine Bewertungen

- Related PartiesDokument3 SeitenRelated PartiesGerlie OpinionNoch keine Bewertungen

- Smieliauskas 6e - Solutions Manual - Chapter 01Dokument8 SeitenSmieliauskas 6e - Solutions Manual - Chapter 01scribdteaNoch keine Bewertungen

- Business TaxesDokument47 SeitenBusiness TaxesJoyce MorganNoch keine Bewertungen

- 13, 14 - Kieso - Inter - Ch22 - IfRS (Accounting Changes)Dokument59 Seiten13, 14 - Kieso - Inter - Ch22 - IfRS (Accounting Changes)hidaNoch keine Bewertungen

- Auditing in BangladeshDokument60 SeitenAuditing in BangladeshImran Kamal100% (1)

- Lecture 6 Business CombinationDokument23 SeitenLecture 6 Business CombinationSikderSharif100% (1)

- Finance QuizDokument2 SeitenFinance Quizshahidlatifhcc100% (1)

- Ethics, Fraud, and Internal ControlDokument49 SeitenEthics, Fraud, and Internal ControlAzizah Syarif100% (3)

- Section Managerial PDFDokument7 SeitenSection Managerial PDFFery AnnNoch keine Bewertungen

- Test Bank For Auditing and Assurance A Business Risk Approach 3rd Edition by JubbDokument19 SeitenTest Bank For Auditing and Assurance A Business Risk Approach 3rd Edition by Jubba878091955Noch keine Bewertungen

- Module 1B - PFRS For Medium Entities NotesDokument25 SeitenModule 1B - PFRS For Medium Entities NotesLee SuarezNoch keine Bewertungen

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokument38 SeitenPrepared by Coby Harmon University of California, Santa Barbara Westmont Collegee s tNoch keine Bewertungen

- CASEDokument18 SeitenCASEJay SabioNoch keine Bewertungen

- Ias 10 Events After The Reporting PeriodDokument9 SeitenIas 10 Events After The Reporting PeriodTawanda Tatenda HerbertNoch keine Bewertungen

- Internal Control WeaknessesDokument3 SeitenInternal Control WeaknessesRosaly JadraqueNoch keine Bewertungen

- Chapter One Accounting Principles and Professional PracticeDokument22 SeitenChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- BUSCOMDokument5 SeitenBUSCOMGeoreyGNoch keine Bewertungen

- Financial Management IDokument58 SeitenFinancial Management Igelango124419Noch keine Bewertungen

- For Students Capital BudgetingDokument3 SeitenFor Students Capital Budgetingwew123Noch keine Bewertungen

- LeasesDokument57 SeitenLeasesnati50% (2)

- Chapter 6 Audit of The Capital Acquisition and Repayment CycleDokument23 SeitenChapter 6 Audit of The Capital Acquisition and Repayment CyclebikilahussenNoch keine Bewertungen

- The Revenue Cycle PDFDokument64 SeitenThe Revenue Cycle PDFIan De Dios0% (1)

- Solutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsDokument26 SeitenSolutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsStefany Mie MosendeNoch keine Bewertungen

- Auditing - 3 Materiality PDFDokument10 SeitenAuditing - 3 Materiality PDFSaad ShehryarNoch keine Bewertungen

- Chapter 3 - IllustrationsDokument97 SeitenChapter 3 - IllustrationsAccounting Materials0% (1)

- TMIF Chapter OneDokument46 SeitenTMIF Chapter OneYibeltal AssefaNoch keine Bewertungen

- When A Thing Is Designated Merely by Its Class or Genus Without Any Particular Designation or Physical Segregation From All Others of The Same ClassDokument6 SeitenWhen A Thing Is Designated Merely by Its Class or Genus Without Any Particular Designation or Physical Segregation From All Others of The Same ClassJimmy Boy DiazNoch keine Bewertungen

- Blackwood Industries Manufactures Die Machinery To Meet Its ExpDokument1 SeiteBlackwood Industries Manufactures Die Machinery To Meet Its ExpAmit PandeyNoch keine Bewertungen

- Corporate Financial Analysis with Microsoft ExcelVon EverandCorporate Financial Analysis with Microsoft ExcelBewertung: 5 von 5 Sternen5/5 (1)

- Management Reporting A Complete Guide - 2019 EditionVon EverandManagement Reporting A Complete Guide - 2019 EditionNoch keine Bewertungen

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityVon EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNoch keine Bewertungen

- Ind Ibeqae-2011 PDFDokument121 SeitenInd Ibeqae-2011 PDFmaleendaNoch keine Bewertungen

- Guidance Note On Audit of InventoriesDokument21 SeitenGuidance Note On Audit of InventoriesmaleendaNoch keine Bewertungen

- Internal Control ConceptsDokument14 SeitenInternal Control Conceptsmaleenda100% (1)

- 03 Internal Audit Report - StocktakesDokument4 Seiten03 Internal Audit Report - StocktakesmaleendaNoch keine Bewertungen

- Project Management For Construction Book - 2008Dokument504 SeitenProject Management For Construction Book - 2008sentinelionNoch keine Bewertungen

- 1.project Plan TemplateDokument31 Seiten1.project Plan TemplatemaleendaNoch keine Bewertungen

- 1 Audit Program ExpensesDokument14 Seiten1 Audit Program Expensesmaleenda100% (3)

- 1 - OPM - Costing - SetupDokument27 Seiten1 - OPM - Costing - SetupAhmedNoch keine Bewertungen

- Understanding Average Cost VarianceDokument16 SeitenUnderstanding Average Cost VarianceShashikant WakharkarNoch keine Bewertungen

- SCM AssignmentDokument15 SeitenSCM AssignmentBhawana SinhaNoch keine Bewertungen

- Chapter 3 Cost Accounting Cycle Multiple Choice - TheoriesDokument36 SeitenChapter 3 Cost Accounting Cycle Multiple Choice - TheoriesAyra Pelenio100% (2)

- BP Op Entpr S4hana1709 04 Prerequisites Matrix en UsDokument38 SeitenBP Op Entpr S4hana1709 04 Prerequisites Matrix en UskiranNoch keine Bewertungen

- Value Stream Mapping at SysIntegDokument16 SeitenValue Stream Mapping at SysIntegAsher RamishNoch keine Bewertungen

- CH 06Dokument72 SeitenCH 06Lenny FransiskaNoch keine Bewertungen

- WIKI - The Statement of Cost of Goods SoldDokument5 SeitenWIKI - The Statement of Cost of Goods SoldHanna GeguillanNoch keine Bewertungen

- Inventory Management: Dr. Anurag Tiwari IIM RohtakDokument68 SeitenInventory Management: Dr. Anurag Tiwari IIM RohtakBinodini SenNoch keine Bewertungen

- Cost Accounting Part 1 (University of Cebu) Cost Accounting Part 1 (University of Cebu)Dokument6 SeitenCost Accounting Part 1 (University of Cebu) Cost Accounting Part 1 (University of Cebu)Shane TorrieNoch keine Bewertungen

- How Much Money Will You Save?: EXACT'S Warehouse Management SystemDokument2 SeitenHow Much Money Will You Save?: EXACT'S Warehouse Management SystemCarlos Manuel ParionaNoch keine Bewertungen

- Types of Business According To ActivitiesDokument2 SeitenTypes of Business According To ActivitiesKayzelleNoch keine Bewertungen

- InventoryDokument93 SeitenInventoryCarmelo John DelacruzNoch keine Bewertungen

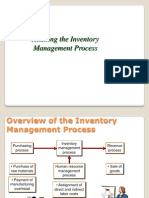

- Auditing The Inventory Management ProcessDokument15 SeitenAuditing The Inventory Management ProcessGohar Mahmood100% (1)

- Materials ManagementDokument39 SeitenMaterials ManagementBinuNoch keine Bewertungen

- Financial Ratio Analysis of Indus Motor Company LTDDokument40 SeitenFinancial Ratio Analysis of Indus Motor Company LTDAurang ZaibNoch keine Bewertungen

- Fitter Snacker 2 Production ProcessDokument4 SeitenFitter Snacker 2 Production ProcessKay Hydee Pabellon100% (2)

- Template For Breakout Activity 2Dokument6 SeitenTemplate For Breakout Activity 2M Rahman0% (3)

- Gunny Bags Inventory Case AnalysisDokument3 SeitenGunny Bags Inventory Case AnalysisAnish Gulati100% (1)

- Depreciation Practice in BangladeshDokument17 SeitenDepreciation Practice in Bangladeshgregs_asif67% (3)

- Week 2 AssignmentDokument2 SeitenWeek 2 AssignmentsaturnelNoch keine Bewertungen

- Inventory Managemnt, Inventory Control, and Benfits of Inventory CotrolDokument6 SeitenInventory Managemnt, Inventory Control, and Benfits of Inventory CotroltomNoch keine Bewertungen

- Sales Return, Credit, and Debit MemoDokument2 SeitenSales Return, Credit, and Debit MemoKnp ChowdaryNoch keine Bewertungen

- 5 Main Categories of ObsoleteDokument3 Seiten5 Main Categories of ObsoleteSoorajKrishnanNoch keine Bewertungen

- Mcqs On Accounting For Business Decision (Chapter 3 To 5) : (A) Can Not (B) Can (C) May or May Not (D) MustDokument10 SeitenMcqs On Accounting For Business Decision (Chapter 3 To 5) : (A) Can Not (B) Can (C) May or May Not (D) MustUsha Ananda ramugadeNoch keine Bewertungen

- Financial Statement AnalysisDokument28 SeitenFinancial Statement AnalysisSachin Methree75% (4)

- Inventory Key Figures in 0IC - C03 CubeDokument1 SeiteInventory Key Figures in 0IC - C03 CubegetsudhanshuNoch keine Bewertungen

- Sap Copc 12 PgsDokument12 SeitenSap Copc 12 PgsJose Luis Becerril Burgos100% (1)

- Questions 1 & 2 Are Based On The Following InformationDokument3 SeitenQuestions 1 & 2 Are Based On The Following InformationBella AyabNoch keine Bewertungen

- 01BF250682E948FB9B248B2273097D9CDokument3 Seiten01BF250682E948FB9B248B2273097D9CjalanayushNoch keine Bewertungen