Das könnte Ihnen auch gefallen

- CHEM Journal PG No 49RDokument1 SeiteCHEM Journal PG No 49RrrkabraNoch keine Bewertungen

- Asset Accounting IMGDokument314 SeitenAsset Accounting IMGrrkabraNoch keine Bewertungen

- Standard CostingDokument38 SeitenStandard CostingrrkabraNoch keine Bewertungen

- Understand How SAP Mobile Platform Solves Enterprises' Mobility NeedsDokument15 SeitenUnderstand How SAP Mobile Platform Solves Enterprises' Mobility NeedsrrkabraNoch keine Bewertungen

- White PaperDokument17 SeitenWhite PaperrrkabraNoch keine Bewertungen

- SAP Report PainterDokument85 SeitenSAP Report Painterdeepank80Noch keine Bewertungen

- User Exits in FicoDokument20 SeitenUser Exits in Ficonaveens9Noch keine Bewertungen

- SAP Witholding Tax Lower Deduction With LimitsDokument2 SeitenSAP Witholding Tax Lower Deduction With LimitsrrkabraNoch keine Bewertungen

- SAP Implementation Impact on Organizational StructureDokument24 SeitenSAP Implementation Impact on Organizational Structurerrkabra50% (2)

- HarmonicaDokument1 SeiteHarmonicarrkabraNoch keine Bewertungen

- SAP Convergence Solution Brief & Roadmap Builder: Beyond Technology AlignmentDokument9 SeitenSAP Convergence Solution Brief & Roadmap Builder: Beyond Technology AlignmentrrkabraNoch keine Bewertungen

- Animals and Birds of EuropeDokument3 SeitenAnimals and Birds of EuroperrkabraNoch keine Bewertungen

- Extra Questions Solutions JK ShahDokument16 SeitenExtra Questions Solutions JK ShahrrkabraNoch keine Bewertungen

- FI Configuration Document - LakshyaDokument103 SeitenFI Configuration Document - LakshyarrkabraNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Integrated Accounting SystemsDokument15 SeitenIntegrated Accounting SystemsSanjeev JayaratnaNoch keine Bewertungen

- Deloitte Tax Alert - Tax Is Deductible at Source On Year-End Provisions Created For Ascertained LiabilitiesDokument4 SeitenDeloitte Tax Alert - Tax Is Deductible at Source On Year-End Provisions Created For Ascertained LiabilitiesRajuNoch keine Bewertungen

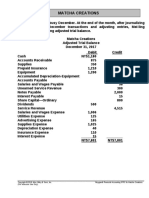

- MC4 Matcha Creations: (For Instructor Use Only)Dokument2 SeitenMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNoch keine Bewertungen

- APM Case Study (RegionFlyDokument14 SeitenAPM Case Study (RegionFlyVignesh Balachandar100% (3)

- Y9 Commercials Notes and Worksheet PDFDokument12 SeitenY9 Commercials Notes and Worksheet PDFBlack MusicNoch keine Bewertungen

- Chapter 6 Cost of CapitalDokument18 SeitenChapter 6 Cost of CapitalmedrekNoch keine Bewertungen

- Class 11 Accountancy NCERT Textbook Part-II Chapter 9 Financial Statement-IDokument46 SeitenClass 11 Accountancy NCERT Textbook Part-II Chapter 9 Financial Statement-IPathan KausarNoch keine Bewertungen

- The Formulas of All The Ratios: A. Financial Stability, Solvency, Liquidity, Balance Sheet RatiosDokument2 SeitenThe Formulas of All The Ratios: A. Financial Stability, Solvency, Liquidity, Balance Sheet RatiosAayush AgrawalNoch keine Bewertungen

- Soft Reviewer Sa Finance by Totowable..: Activity Cost and Cost Analysis TheoriesDokument9 SeitenSoft Reviewer Sa Finance by Totowable..: Activity Cost and Cost Analysis TheoriesRichard DuranNoch keine Bewertungen

- VAT RefundDokument45 SeitenVAT RefundPatrick Tan100% (1)

- Group Accounts: IFRS 10 Consolidated Financial StatementsDokument9 SeitenGroup Accounts: IFRS 10 Consolidated Financial StatementsHunairArshadNoch keine Bewertungen

- CEO Morning - 20200820 PDFDokument22 SeitenCEO Morning - 20200820 PDFChin Lip SohNoch keine Bewertungen

- Payroll ReportDokument7 SeitenPayroll ReportAndrhea GonzalesNoch keine Bewertungen

- Trial Balance (PD JAYA MOTOR)Dokument1 SeiteTrial Balance (PD JAYA MOTOR)Arum AnnisaNoch keine Bewertungen

- 2.1 Trade and Other ReceivablesDokument4 Seiten2.1 Trade and Other ReceivablesShally Lao-unNoch keine Bewertungen

- 1109021 (1)Dokument1 Seite1109021 (1)Cms Stl CmsNoch keine Bewertungen

- Dangote Cement PLC NGSE DANGCEM Financials SegmentsDokument6 SeitenDangote Cement PLC NGSE DANGCEM Financials SegmentsDavid HundeyinNoch keine Bewertungen

- Leadership Case StudyDokument18 SeitenLeadership Case Studystargirl1786Noch keine Bewertungen

- A Comparative Study On Performance of Tata Consultancy Services and Infosys For The Period 2013-2017 by Using Valuation RatiosDokument5 SeitenA Comparative Study On Performance of Tata Consultancy Services and Infosys For The Period 2013-2017 by Using Valuation RatiosSavy DhillonNoch keine Bewertungen

- Tire City Case SolutionDokument6 SeitenTire City Case SolutionShivam Bhasin60% (10)

- Theories (PPE)Dokument30 SeitenTheories (PPE)LDB Ashley Jeremiah Magsino - ABMNoch keine Bewertungen

- Brains Trust PPT - MR Gautam DoshiDokument31 SeitenBrains Trust PPT - MR Gautam DoshiIshanNoch keine Bewertungen

- Kind of Income Tax RateDokument2 SeitenKind of Income Tax RateTJ MerinNoch keine Bewertungen

- Residential StatusDokument4 SeitenResidential StatusShaji KuttyNoch keine Bewertungen

- Also Hy2023 en VIDokument21 SeitenAlso Hy2023 en VImihirbhojani603Noch keine Bewertungen

- DFB IncDokument1 SeiteDFB IncFachrurrozi BojayNoch keine Bewertungen

- Presentation1 ReshmaDokument26 SeitenPresentation1 ReshmaJOE NOBLE 2020519Noch keine Bewertungen

- IAS 36 Impairment of AssetsDokument7 SeitenIAS 36 Impairment of AssetsMazni Hanisah0% (1)

- Jawaban Kuis Uph Debt InvestmentDokument3 SeitenJawaban Kuis Uph Debt InvestmentSagita RajagukgukNoch keine Bewertungen

- ZomatoDokument6 SeitenZomatoChandra Sekhar GudaNoch keine Bewertungen