Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Final Exam 2013cDokument4 SeitenFinal Exam 2013cphuthuymiNoch keine Bewertungen

- Econ-1042 Sample Mcqs1120Dokument3 SeitenEcon-1042 Sample Mcqs1120phuthuymiNoch keine Bewertungen

- ECON1268 Final Exam S2 2011Dokument7 SeitenECON1268 Final Exam S2 2011phuthuymiNoch keine Bewertungen

- ECON1268 Final Exam S2 2011Dokument7 SeitenECON1268 Final Exam S2 2011phuthuymiNoch keine Bewertungen

- Econ-1042 Sample Mcqs110Dokument3 SeitenEcon-1042 Sample Mcqs110phuthuymiNoch keine Bewertungen

- ECON1268 Final Exam S2 2011Dokument7 SeitenECON1268 Final Exam S2 2011phuthuymiNoch keine Bewertungen

- EF 210 Sample Multiple Choice Questions Semester 1 2008 AnswerDokument1 SeiteEF 210 Sample Multiple Choice Questions Semester 1 2008 AnswerphuthuymiNoch keine Bewertungen

- EF 210 Sample Multiple Choice Questions Semester 1 2008: Sheet1Dokument1 SeiteEF 210 Sample Multiple Choice Questions Semester 1 2008: Sheet1phuthuymiNoch keine Bewertungen

- Demonstration Lecture 5: Suggested SolutionsDokument2 SeitenDemonstration Lecture 5: Suggested SolutionsphuthuymiNoch keine Bewertungen

- EF 210 Sample Multiple Choice Questions Semester 1 2008: Sheet1Dokument1 SeiteEF 210 Sample Multiple Choice Questions Semester 1 2008: Sheet1phuthuymiNoch keine Bewertungen

- Demonstration Lecture 3: Suggested SolutionsDokument2 SeitenDemonstration Lecture 3: Suggested SolutionsphuthuymiNoch keine Bewertungen

- Demonstration Lecture 4: Suggested SolutionsDokument2 SeitenDemonstration Lecture 4: Suggested SolutionsphuthuymiNoch keine Bewertungen

- DEMOLEC1Dokument9 SeitenDEMOLEC1phuthuymiNoch keine Bewertungen

- Topic 1 Introduction To Business FinanceDokument28 SeitenTopic 1 Introduction To Business FinancephuthuymiNoch keine Bewertungen

- Mid-Term Exam Sem 3 2012Dokument9 SeitenMid-Term Exam Sem 3 2012phuthuymiNoch keine Bewertungen

- Topic 4 Capital Budgeting Part 2Dokument42 SeitenTopic 4 Capital Budgeting Part 2phuthuymiNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Gabriel Marcel - Sketch of A Phenomenology and A Metaphysic of HopeDokument6 SeitenGabriel Marcel - Sketch of A Phenomenology and A Metaphysic of HopeHazel Dawn PaticaNoch keine Bewertungen

- Cover LetterDokument2 SeitenCover LetterGeorgy Khalatov100% (4)

- 4 Marine Insurance 10-8-6Dokument53 Seiten4 Marine Insurance 10-8-6Eunice Saavedra100% (1)

- Water Conference InvitationDokument2 SeitenWater Conference InvitationDonna MelgarNoch keine Bewertungen

- GAAR Slide Deck 13072019Dokument38 SeitenGAAR Slide Deck 13072019Sandeep GolaniNoch keine Bewertungen

- TS06C Jibril, Garba 5915Dokument13 SeitenTS06C Jibril, Garba 5915Umar SunusiNoch keine Bewertungen

- 6 Habits of True Strategic ThinkersDokument64 Seiten6 Habits of True Strategic ThinkersPraveen Kumar JhaNoch keine Bewertungen

- Bainbridge - Smith v. Van GorkomDokument33 SeitenBainbridge - Smith v. Van GorkomMiguel CasanovaNoch keine Bewertungen

- Excerpted From Watching FoodDokument4 SeitenExcerpted From Watching Foodsoc2003Noch keine Bewertungen

- India's Cultural Diplomacy: Present Dynamics, Challenges and Future ProspectsDokument11 SeitenIndia's Cultural Diplomacy: Present Dynamics, Challenges and Future ProspectsMAHANTESH GNoch keine Bewertungen

- Zlodjela Bolesnog UmaDokument106 SeitenZlodjela Bolesnog UmaDZENAN SARACNoch keine Bewertungen

- 30 Iconic Filipino SongsDokument9 Seiten30 Iconic Filipino SongsAlwynBaloCruzNoch keine Bewertungen

- What Is Supply Chain ManagementDokument3 SeitenWhat Is Supply Chain ManagementozkanyilmazNoch keine Bewertungen

- Chapter 4 ProjDokument15 SeitenChapter 4 ProjEphrem ChernetNoch keine Bewertungen

- Manufacturing ConsentDokument3 SeitenManufacturing ConsentSaif Khalid100% (1)

- Summary (SDL: Continuing The Evolution)Dokument2 SeitenSummary (SDL: Continuing The Evolution)ahsanlone100% (2)

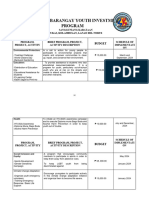

- Annual Barangay Youth Investment ProgramDokument4 SeitenAnnual Barangay Youth Investment ProgramBarangay MukasNoch keine Bewertungen

- DEED OF ABSOLUTE SALE-Paul Wilde HatulanDokument4 SeitenDEED OF ABSOLUTE SALE-Paul Wilde HatulanLanie LeiNoch keine Bewertungen

- StudioArabiyaTimes Magazine Spring 2022Dokument58 SeitenStudioArabiyaTimes Magazine Spring 2022Ali IshaanNoch keine Bewertungen

- Braintrain: Summer Camp WorksheetDokument9 SeitenBraintrain: Summer Camp WorksheetPadhmennNoch keine Bewertungen

- Big Enabler Solutions ProfileDokument6 SeitenBig Enabler Solutions ProfileTecbind UniversityNoch keine Bewertungen

- IBA High Frequency Words PDFDokument18 SeitenIBA High Frequency Words PDFReduanul Chowdhury NitulNoch keine Bewertungen

- Empower Catalog Ca6721en MsDokument138 SeitenEmpower Catalog Ca6721en MsSurya SamoerNoch keine Bewertungen

- Ashok Leyland - Industry Visit ReportDokument7 SeitenAshok Leyland - Industry Visit Reportabikrishna1989Noch keine Bewertungen

- Ltma Lu DissertationDokument5 SeitenLtma Lu DissertationPayToWriteMyPaperUK100% (1)

- SMART Goal Worksheet (Action Plan)Dokument2 SeitenSMART Goal Worksheet (Action Plan)Tiaan de Jager100% (1)

- CT-e: Legal Change: Configuration GuideDokument14 SeitenCT-e: Legal Change: Configuration GuidecamillagouveaNoch keine Bewertungen

- Juarez, Jenny Brozas - Activity 2 MidtermDokument4 SeitenJuarez, Jenny Brozas - Activity 2 MidtermJenny Brozas JuarezNoch keine Bewertungen

- Historical Allusions in The Book of Habakkuk: Aron PinkerDokument10 SeitenHistorical Allusions in The Book of Habakkuk: Aron Pinkerstefa74Noch keine Bewertungen

- Program Notes, Texts, and Translations For The Senior Recital of M. Evan Meisser, BartioneDokument10 SeitenProgram Notes, Texts, and Translations For The Senior Recital of M. Evan Meisser, Bartione123Noch keine Bewertungen