Das könnte Ihnen auch gefallen

- 1040 Exam Prep Module X: Small Business Income and ExpensesVon Everand1040 Exam Prep Module X: Small Business Income and ExpensesNoch keine Bewertungen

- Profits and Gains of Business or Profession3Dokument24 SeitenProfits and Gains of Business or Profession3KUSUM YADAVNoch keine Bewertungen

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesVon EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNoch keine Bewertungen

- Profits and Gains of Business or Profession4Dokument24 SeitenProfits and Gains of Business or Profession4Soni SinghNoch keine Bewertungen

- Profits and Gains of Business or Profession in MBADokument24 SeitenProfits and Gains of Business or Profession in MBALakhan ChhapruNoch keine Bewertungen

- Income TaxationDokument38 SeitenIncome TaxationElson TalotaloNoch keine Bewertungen

- Profits and Gains of Business or Profession-2Dokument15 SeitenProfits and Gains of Business or Profession-2Dr. Mustafa KozhikkalNoch keine Bewertungen

- Tax II Chapter IDokument49 SeitenTax II Chapter IsejalNoch keine Bewertungen

- Final Tax Audit-JigarDokument20 SeitenFinal Tax Audit-JigarJigar MehtaNoch keine Bewertungen

- Income From Business 23Dokument27 SeitenIncome From Business 23kalyani baviskarNoch keine Bewertungen

- PGBPDokument61 SeitenPGBPJyoti Kalotra0% (1)

- Unit 3 Profits On Business ADokument19 SeitenUnit 3 Profits On Business AAnshu kumarNoch keine Bewertungen

- Income Tax - 3-28-12 Ganer FinalDokument85 SeitenIncome Tax - 3-28-12 Ganer Finaljeromie163Noch keine Bewertungen

- Income From Business and ProfessionDokument14 SeitenIncome From Business and Professionimdadul haqueNoch keine Bewertungen

- Final MF0003 2nd AssigDokument6 SeitenFinal MF0003 2nd Assignigistwold5192Noch keine Bewertungen

- Profit and Gain of Business ProfessionDokument21 SeitenProfit and Gain of Business ProfessionSamar GautamNoch keine Bewertungen

- Income Tax TableDokument10 SeitenIncome Tax TableChelissaRojasNoch keine Bewertungen

- In Come Tax Tables Annex BDokument9 SeitenIn Come Tax Tables Annex BigorotknightNoch keine Bewertungen

- Profits and Gains of Business and ProfessionDokument41 SeitenProfits and Gains of Business and ProfessionEsha BafnaNoch keine Bewertungen

- Corporate Tax PlanningDokument139 SeitenCorporate Tax PlanningDr Linda Mary SimonNoch keine Bewertungen

- It 2Dokument44 SeitenIt 2Business RecoveryNoch keine Bewertungen

- Subu Income From Other Sources Final - 2Dokument5 SeitenSubu Income From Other Sources Final - 2Nitesh BhuraNoch keine Bewertungen

- Special Itemized Deductions, NOLCO & OSDDokument13 SeitenSpecial Itemized Deductions, NOLCO & OSDdianne caballero100% (1)

- Gross Income Deductions - Lecture Handout PDFDokument4 SeitenGross Income Deductions - Lecture Handout PDFKarl RendonNoch keine Bewertungen

- Business and ProfessionDokument21 SeitenBusiness and ProfessionKailash MotwaniNoch keine Bewertungen

- Income Tax Law and It's Computation Sandeep KumarDokument33 SeitenIncome Tax Law and It's Computation Sandeep KumarThe PaletteNoch keine Bewertungen

- Statutory Income Assessable Income Chargeable IncomeDokument4 SeitenStatutory Income Assessable Income Chargeable IncomeKelvin Lim Wei LiangNoch keine Bewertungen

- Income From Business and ProfessionDokument23 SeitenIncome From Business and ProfessionAmit KumarNoch keine Bewertungen

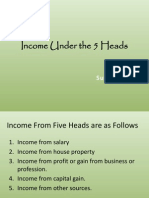

- Income Under The 5 Heads: Sudhir YadavDokument21 SeitenIncome Under The 5 Heads: Sudhir YadavpreetkaurrandhawaNoch keine Bewertungen

- In Come Tax TableDokument9 SeitenIn Come Tax TablejorjirubiNoch keine Bewertungen

- Profits and Gains of Business or ProfessionDokument17 SeitenProfits and Gains of Business or ProfessionAman hingoraniNoch keine Bewertungen

- ItlpDokument14 SeitenItlpA_saravanavelNoch keine Bewertungen

- Profits and Gains of Business or ProfessionDokument17 SeitenProfits and Gains of Business or Professionapi-3832224Noch keine Bewertungen

- Tax Cheat SheetDokument2 SeitenTax Cheat SheetJean Pingfang Koh100% (3)

- Tax Audit Taxing Audit!!... : By:-CA. Krishan Vrind JainDokument52 SeitenTax Audit Taxing Audit!!... : By:-CA. Krishan Vrind JainVrind JainNoch keine Bewertungen

- Income TaxDokument85 SeitenIncome TaxvicsNoch keine Bewertungen

- PGBP New SlidesDokument40 SeitenPGBP New SlidesSachin Jain100% (2)

- Annex B: Income Tax Tables: Table 1 Tax Rates For IndividualsDokument9 SeitenAnnex B: Income Tax Tables: Table 1 Tax Rates For Individualshaze_toledo5077Noch keine Bewertungen

- Income From Business: Carry Forward of LossesDokument2 SeitenIncome From Business: Carry Forward of LossesArunaMLNoch keine Bewertungen

- F6 Tax RulesDokument2 SeitenF6 Tax RulesLavneesh ShibduthNoch keine Bewertungen

- Icitss Project FileDokument21 SeitenIcitss Project FileShrey JainNoch keine Bewertungen

- Income TaxDokument31 SeitenIncome TaxUday KumarNoch keine Bewertungen

- PGBP NotesDokument5 SeitenPGBP NotesRadhika DuttaNoch keine Bewertungen

- Profits and Gains of Business or ProfessionDokument35 SeitenProfits and Gains of Business or ProfessionnikkiNoch keine Bewertungen

- 1 Deductions From Gross Income-FinalDokument24 Seiten1 Deductions From Gross Income-FinalSharon Ann BasulNoch keine Bewertungen

- CPA Regulation (Reg) Notes 2013Dokument7 SeitenCPA Regulation (Reg) Notes 2013amichalek0820100% (3)

- Income From Business or ProfessionDokument24 SeitenIncome From Business or ProfessionRahulMalikNoch keine Bewertungen

- Deductions From Gross Income Lesson 13Dokument72 SeitenDeductions From Gross Income Lesson 13Mikaela SamonteNoch keine Bewertungen

- Allowable Deductions NotesDokument5 SeitenAllowable Deductions NotesPaula Mae DacanayNoch keine Bewertungen

- PGBPDokument14 SeitenPGBPSaurav MedhiNoch keine Bewertungen

- Income From Business TheoryDokument5 SeitenIncome From Business TheoryYashin Y HNoch keine Bewertungen

- JPIA Review S3 Installment 2 (Business Tax)Dokument30 SeitenJPIA Review S3 Installment 2 (Business Tax)rylNoch keine Bewertungen

- Various Sections in PGBP Are Briefly Discussed Below:: PGBP (Profits and Gains From Business or Profession) Sec 28-44Dokument4 SeitenVarious Sections in PGBP Are Briefly Discussed Below:: PGBP (Profits and Gains From Business or Profession) Sec 28-44Abhishek MishraNoch keine Bewertungen

- Lecture 3 - Income Taxation (Corporate)Dokument8 SeitenLecture 3 - Income Taxation (Corporate)Lovenia Magpatoc50% (2)

- Intax 03Dokument15 SeitenIntax 03khyla Marie NooraNoch keine Bewertungen

- Tax Management NotesDokument21 SeitenTax Management NotesChetan GKNoch keine Bewertungen

- Notes On Income From Business or ProfessionDokument15 SeitenNotes On Income From Business or Professionnitinsuba1980Noch keine Bewertungen

- Income Tax in IndiaDokument19 SeitenIncome Tax in IndiaConcepts TreeNoch keine Bewertungen

- PDF of PGBPDokument7 SeitenPDF of PGBPCHENDUCHAITHUNoch keine Bewertungen

- 634568674096644622Dokument17 Seiten634568674096644622Anitha GirigoudruNoch keine Bewertungen

- Project IciciDokument72 SeitenProject IciciundefinedmohitNoch keine Bewertungen

- Balance of Trade and Balance of PaymentDokument21 SeitenBalance of Trade and Balance of Paymentfazilshareef1885Noch keine Bewertungen

- WTO, Objectives, Scope and Functions 2nd January 2012Dokument30 SeitenWTO, Objectives, Scope and Functions 2nd January 2012Anitha Girigoudru33% (3)

- Income From Business & ProfessionDokument8 SeitenIncome From Business & ProfessionAnitha GirigoudruNoch keine Bewertungen

- Modes of Entry Into An International BusinessDokument6 SeitenModes of Entry Into An International Businessrabinosss95% (22)

- Credit Guranatee Fund Trust Scheme For MicroDokument4 SeitenCredit Guranatee Fund Trust Scheme For MicroAnitha GirigoudruNoch keine Bewertungen

- International FinanceDokument207 SeitenInternational FinanceAnitha Girigoudru50% (2)

- Meaning of Strategy FormulationDokument13 SeitenMeaning of Strategy FormulationNeenu VargheseNoch keine Bewertungen

- Modes of Entry Into An International BusinessDokument6 SeitenModes of Entry Into An International Businessrabinosss95% (22)

- Wealth ManagementDokument45 SeitenWealth ManagementAnitha GirigoudruNoch keine Bewertungen

- Icici PrudentialDokument38 SeitenIcici PrudentialAnitha GirigoudruNoch keine Bewertungen

- Balance of Payment (BOP)Dokument27 SeitenBalance of Payment (BOP)Fardeen KhanNoch keine Bewertungen

- Sources of CapitalDokument2 SeitenSources of CapitalAnitha GirigoudruNoch keine Bewertungen

- Project IciciDokument72 SeitenProject IciciundefinedmohitNoch keine Bewertungen

- 634568674096644622Dokument17 Seiten634568674096644622Anitha GirigoudruNoch keine Bewertungen

- Sources of CapitalDokument2 SeitenSources of CapitalAnitha GirigoudruNoch keine Bewertungen

- International Financal MangamentDokument206 SeitenInternational Financal MangamentRoopa RoyNoch keine Bewertungen

- The Top Three Business Benefits of Clearly Setting and Aligning Organizational Goals Across Your CompanyDokument18 SeitenThe Top Three Business Benefits of Clearly Setting and Aligning Organizational Goals Across Your CompanyAnitha GirigoudruNoch keine Bewertungen

- Working Capital FinanceDokument17 SeitenWorking Capital FinanceAnitha GirigoudruNoch keine Bewertungen

- International Financal MangamentDokument206 SeitenInternational Financal MangamentRoopa RoyNoch keine Bewertungen

- Factor Endowment TheoryDokument4 SeitenFactor Endowment TheoryAnitha GirigoudruNoch keine Bewertungen

- Curriculum Vitae: ObjectiveDokument2 SeitenCurriculum Vitae: ObjectiveAnitha GirigoudruNoch keine Bewertungen

- Project IciciDokument72 SeitenProject IciciundefinedmohitNoch keine Bewertungen

- 634568674096644622Dokument17 Seiten634568674096644622Anitha GirigoudruNoch keine Bewertungen

- CTDokument55 SeitenCTAnitha GirigoudruNoch keine Bewertungen

- Project IciciDokument72 SeitenProject IciciundefinedmohitNoch keine Bewertungen

- 4 BankingDokument95 Seiten4 BankingAnitha GirigoudruNoch keine Bewertungen

- 634568674096644622Dokument17 Seiten634568674096644622Anitha GirigoudruNoch keine Bewertungen