Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Real Estate Investing Guide - 7 Traps of Real Estate InvestingDokument18 SeitenReal Estate Investing Guide - 7 Traps of Real Estate InvestingScott Roemermann100% (4)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Return of The Quants - Risk-Based InvestingDokument13 SeitenReturn of The Quants - Risk-Based InvestingdoncalpeNoch keine Bewertungen

- GLTU Value CreationDokument9 SeitenGLTU Value CreationAnil GowdaNoch keine Bewertungen

- Sports Equipment Retail Business PlanDokument8 SeitenSports Equipment Retail Business PlanSachinNoch keine Bewertungen

- Assignment 1 SolutionDokument13 SeitenAssignment 1 Solutiondiksha_motwaniNoch keine Bewertungen

- Security Documentation FinalDokument37 SeitenSecurity Documentation Finaldiksha_motwaniNoch keine Bewertungen

- International Banking & Finance CaseDokument7 SeitenInternational Banking & Finance Casediksha_motwaniNoch keine Bewertungen

- BI - Fin ForecastDokument13 SeitenBI - Fin Forecastdiksha_motwaniNoch keine Bewertungen

- Ypothecation OF Ovable Achinery Letter OF Credit Packing CreditDokument38 SeitenYpothecation OF Ovable Achinery Letter OF Credit Packing Creditdiksha_motwaniNoch keine Bewertungen

- Letter of CreditDokument8 SeitenLetter of Creditdiksha_motwaniNoch keine Bewertungen

- BI - Fin ForecastDokument13 SeitenBI - Fin Forecastdiksha_motwaniNoch keine Bewertungen

- Group 1Dokument9 SeitenGroup 1diksha_motwaniNoch keine Bewertungen

- Creditratingagencycrappt 130306035605 Phpapp02Dokument17 SeitenCreditratingagencycrappt 130306035605 Phpapp02diksha_motwaniNoch keine Bewertungen

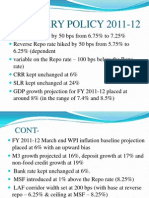

- RBI - Monetary PolicyDokument14 SeitenRBI - Monetary Policydiksha_motwaniNoch keine Bewertungen

- The Indian Contract Act 1872Dokument122 SeitenThe Indian Contract Act 1872Ramakrishna ReddyNoch keine Bewertungen

- InvestmentsDokument58 SeitenInvestmentsdiksha_motwaniNoch keine Bewertungen

- IpoDokument71 SeitenIpoBhumi GhoriNoch keine Bewertungen

- VCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicDokument4 SeitenVCE Summer Internship Program 2020: Name Email-ID Smart Task No. Project TopicYaShNoch keine Bewertungen

- Annual Report 2010-11-02Dokument151 SeitenAnnual Report 2010-11-02Harish BhardwajNoch keine Bewertungen

- 2 Project Financing ImplementationDokument9 Seiten2 Project Financing ImplementationyashNoch keine Bewertungen

- AfriStock Monthly Feb2010Dokument3 SeitenAfriStock Monthly Feb2010Afribiz Global Business and Investment CommunityNoch keine Bewertungen

- Acorn Investments - Systematic TradingDokument9 SeitenAcorn Investments - Systematic TradingAdam butlerNoch keine Bewertungen

- 15 - Investments - TheoryDokument8 Seiten15 - Investments - TheoryROMAR A. PIGANoch keine Bewertungen

- CHAPTER III: Linear Programming ApplicationsDokument24 SeitenCHAPTER III: Linear Programming ApplicationsLouisRemNoch keine Bewertungen

- SECs Final Rules - Venture Capital ExemptionDokument208 SeitenSECs Final Rules - Venture Capital Exemptionventurewire100% (1)

- SEBI Investor Survey 2014-15 EOIDokument16 SeitenSEBI Investor Survey 2014-15 EOIPushpendra KumarNoch keine Bewertungen

- 13th Annual Family Office Forum PDFDokument12 Seiten13th Annual Family Office Forum PDFgneymanNoch keine Bewertungen

- Black Friday - BTGDokument7 SeitenBlack Friday - BTGRenan Dantas SantosNoch keine Bewertungen

- Types of NegotiationDokument5 SeitenTypes of NegotiationDhiraj YAdavNoch keine Bewertungen

- Ltcma Full ReportDokument136 SeitenLtcma Full ReportSricharanNoch keine Bewertungen

- Types of Issues in the Primary MarketDokument16 SeitenTypes of Issues in the Primary MarketAnkit PatidarNoch keine Bewertungen

- Risk and Return Analysis of Stocks: A Literature ReviewDokument15 SeitenRisk and Return Analysis of Stocks: A Literature ReviewNitesh TripathyNoch keine Bewertungen

- Securities and Exchange Board of India (Sebi)Dokument20 SeitenSecurities and Exchange Board of India (Sebi)TaniaNoch keine Bewertungen

- The Modigliani-Miller Theorem HistoryDokument9 SeitenThe Modigliani-Miller Theorem HistoryAlejandra Estrella MadrigalNoch keine Bewertungen

- Impact of Accounting Information On Decision Making ProcessDokument11 SeitenImpact of Accounting Information On Decision Making ProcessRebar QaraxiNoch keine Bewertungen

- Correct Answers Are Shown in - Attempted Answers, If Wrong, Are inDokument5 SeitenCorrect Answers Are Shown in - Attempted Answers, If Wrong, Are insindhu123100% (1)

- Demo - Nism 5 A - Mutual Fund Module PDFDokument7 SeitenDemo - Nism 5 A - Mutual Fund Module PDFrinkesh barnwalNoch keine Bewertungen

- Wekeza Maisha Offer DocumentDokument83 SeitenWekeza Maisha Offer Documentapi-3748159Noch keine Bewertungen

- Bureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon CityDokument4 SeitenBureau of Internal Revenue: Republic of The Philippines Department of Finance Quezon CitygelskNoch keine Bewertungen

- Guide To Financial Markets Regulations - An African PerspectiveDokument241 SeitenGuide To Financial Markets Regulations - An African PerspectivenepadupNoch keine Bewertungen

- Presentation On Corporate Financing Decision and Efficient Capital MarketDokument12 SeitenPresentation On Corporate Financing Decision and Efficient Capital MarketM Mahfuzur RahmanNoch keine Bewertungen

- PP05Dokument73 SeitenPP05aahsaaanNoch keine Bewertungen