Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Filinvest Land INCDokument28 SeitenFilinvest Land INCKris MacuhaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Stock ValuationDokument24 SeitenStock ValuationMohit TewaryNoch keine Bewertungen

- Pre-Incorporation Contracts Provisional Contracts: All Distinguish Between (16 Marks)Dokument10 SeitenPre-Incorporation Contracts Provisional Contracts: All Distinguish Between (16 Marks)Ragini SharmaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- InventoriesDokument35 SeitenInventoriesJay PinedaNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- M&A - Valuation - Expanded - BV - SS EQUIPODokument3 SeitenM&A - Valuation - Expanded - BV - SS EQUIPOGianina Mendoza NestaresNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Befa Unit 1Dokument19 SeitenBefa Unit 1Naresh Guduru89% (71)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Instructions. Choose The BEST Answer For Each of The Following ItemsDokument3 SeitenInstructions. Choose The BEST Answer For Each of The Following ItemsDiomela BionganNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Laporan Keuangan PT BTEL 31 Des 2021Dokument141 SeitenLaporan Keuangan PT BTEL 31 Des 2021Muhammad Mahdi HakimNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- IC3 Corporate Finance Photocopiable8Dokument1 SeiteIC3 Corporate Finance Photocopiable8Оля ИгнатенкоNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Accounting TermDokument7 SeitenAccounting TermThangdong QuayNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Acctg 321 A and B - Quiz - PPE - CSDokument5 SeitenAcctg 321 A and B - Quiz - PPE - CSGet BurnNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Ration Analysis: 7.3 Parties Interested in Ratio AnalysisDokument17 SeitenRation Analysis: 7.3 Parties Interested in Ratio AnalysisMuhammad NoumanNoch keine Bewertungen

- Real Estate Investment AnalysisDokument25 SeitenReal Estate Investment AnalysisHarpreet Dhillon100% (1)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Advanced Entrepreneurship - Full TextDokument117 SeitenAdvanced Entrepreneurship - Full TextOyewole OlayemiNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

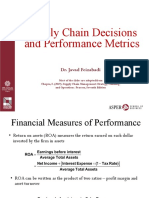

- 3-Supply Chain Decisions and Performance Metrics (A)Dokument21 Seiten3-Supply Chain Decisions and Performance Metrics (A)eeman kNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Fin Model of Hydro Power PlantDokument7 SeitenFin Model of Hydro Power PlantVivek SinghalNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Gold ManDokument5 SeitenGold Manyuvrajs554Noch keine Bewertungen

- Week 2 Excel AssignmentDokument8 SeitenWeek 2 Excel AssignmentadomahattafuahNoch keine Bewertungen

- SASF Mock Exam Answers December 2004 - Level I Page 4 of 30Dokument2 SeitenSASF Mock Exam Answers December 2004 - Level I Page 4 of 30SmileOYNoch keine Bewertungen

- PRELIMSDokument4 SeitenPRELIMSJadon MejiaNoch keine Bewertungen

- IFS International Equity MarketDokument36 SeitenIFS International Equity MarketVrinda GargNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Chap 013 Financial Accounting (Statement of Cash Flow)Dokument39 SeitenChap 013 Financial Accounting (Statement of Cash Flow)salman saeed100% (2)

- Mutual Fund Insight Sep 23Dokument68 SeitenMutual Fund Insight Sep 23Bhupendra Sengar100% (1)

- Plagiarism Scan Report: Plagiarism Unique Plagiarized Sentences Unique SentencesDokument8 SeitenPlagiarism Scan Report: Plagiarism Unique Plagiarized Sentences Unique SentencesPrachi ParabNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Course ObjectiveDokument11 SeitenCourse ObjectivePeter DenNoch keine Bewertungen

- Financial Audit AOL 2Dokument4 SeitenFinancial Audit AOL 2Natasha HerlianaNoch keine Bewertungen

- Homework Chapter 6Dokument10 SeitenHomework Chapter 6Le Nguyen Thu UyenNoch keine Bewertungen

- ACP 311 My Test Bank Problem SolvingDokument22 SeitenACP 311 My Test Bank Problem SolvingJamaica DavidNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Company Name: 2go Group, Inc. List of Top 100 Stockholders As of September 30, 2020Dokument18 SeitenCompany Name: 2go Group, Inc. List of Top 100 Stockholders As of September 30, 2020Jan Ellard CruzNoch keine Bewertungen

- Solution Design Document: Implementation of SAP Business One at Boston - ProperDokument109 SeitenSolution Design Document: Implementation of SAP Business One at Boston - ProperArbabNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)