Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

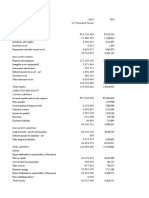

- Flextronics International LTDDokument306 SeitenFlextronics International LTDPriyanka PriyaNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- B.B.A (2013 Pattern)Dokument142 SeitenB.B.A (2013 Pattern)Priyanka PriyaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Aptitude Analysis Syl Lab UsDokument10 SeitenAptitude Analysis Syl Lab UsPriyanka PriyaNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Mayo College, Ajmer: Egistration ORMDokument2 SeitenMayo College, Ajmer: Egistration ORMPriyanka PriyaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Legal For Start-Ups: Nsrcel - Iim-B Quasar LegalDokument18 SeitenLegal For Start-Ups: Nsrcel - Iim-B Quasar LegalPriyanka PriyaNoch keine Bewertungen

- RKDokument4 SeitenRKPriyanka PriyaNoch keine Bewertungen

- Shree Swami Samarth EnterprisesDokument1 SeiteShree Swami Samarth EnterprisesPriyanka PriyaNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Curriculum-Vitae: Adhesh Kumar RamDokument2 SeitenCurriculum-Vitae: Adhesh Kumar RamPriyanka PriyaNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Email Id:: Curriculum Vitae Technical Skills Ramesh S. SutarDokument2 SeitenEmail Id:: Curriculum Vitae Technical Skills Ramesh S. SutarPriyanka PriyaNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Web Inter Form j2012Dokument3 SeitenWeb Inter Form j2012Priyanka PriyaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Financial ManagementDokument145 SeitenFinancial Managementmanuj_uniyal89Noch keine Bewertungen

- Finc600 Week 4 Required Quiz 1Dokument10 SeitenFinc600 Week 4 Required Quiz 1Donald112100% (1)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- 2009-2010 DevolpiDokument54 Seiten2009-2010 DevolpiEmmanuel Benedict Bosque IcaranomNoch keine Bewertungen

- Four P'sDokument2 SeitenFour P'sankitagupNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Risk and Return 1-1Dokument13 SeitenRisk and Return 1-1hero66Noch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- SBI Mutual FundDokument12 SeitenSBI Mutual FundSriram MuthuNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Active Gear Historical Income Statement Operating Results Revenue Gross ProfitDokument20 SeitenActive Gear Historical Income Statement Operating Results Revenue Gross ProfitJoan Alejandro MéndezNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- HSBC InvestmentsDokument52 SeitenHSBC Investmentstacamp daNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Sterling Equities Group Unveils $25 MLN PE Commercial Real Estate FundDokument3 SeitenSterling Equities Group Unveils $25 MLN PE Commercial Real Estate FundPR.comNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Dow TheoryDokument5 SeitenDow TheoryChandra RaviNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Globe PLDT 2014 Financial RatiosDokument6 SeitenGlobe PLDT 2014 Financial RatiosSamNoch keine Bewertungen

- Pivot Points and CandlesticksDokument4 SeitenPivot Points and CandlesticksMisterSimpleNoch keine Bewertungen

- Grandfather RuleDokument6 SeitenGrandfather RulepatNoch keine Bewertungen

- Smallcap Growth StrategyDokument4 SeitenSmallcap Growth StrategyyashNoch keine Bewertungen

- United Breweries Limited MisDokument24 SeitenUnited Breweries Limited MisManishNoch keine Bewertungen

- A Comparative Study of Commercial Bank of NepalDokument10 SeitenA Comparative Study of Commercial Bank of NepalSandeep RanaNoch keine Bewertungen

- Cost of CapitalDokument15 SeitenCost of Capitalসুজয় দত্তNoch keine Bewertungen

- Industry AnalysisDokument24 SeitenIndustry AnalysisSaurabh Krishna SinghNoch keine Bewertungen

- Comp-Xm® Inquirer WordDokument37 SeitenComp-Xm® Inquirer WordAnonymous TAV9RvNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Pro Real Time - ProscreenerDokument36 SeitenPro Real Time - Proscreener11727Noch keine Bewertungen

- Micheal Burry MSN Money Articles 2000Dokument3 SeitenMicheal Burry MSN Money Articles 2000cts5131Noch keine Bewertungen

- BA544 Chap 004Dokument46 SeitenBA544 Chap 004Umit Kaukenova100% (1)

- NISM XA - Investment Adviser 1 Short Notes PDFDokument41 SeitenNISM XA - Investment Adviser 1 Short Notes PDFSAMBIT SAHOO100% (1)

- Torrent Power 20190319 Mosl Ic Pg034Dokument34 SeitenTorrent Power 20190319 Mosl Ic Pg034Poonam AggarwalNoch keine Bewertungen

- MCQ On FDDokument25 SeitenMCQ On FDArun MaxwellNoch keine Bewertungen

- Web Chapter 18 Real Estate and Other Tangible InvestmentsDokument5 SeitenWeb Chapter 18 Real Estate and Other Tangible InvestmentsChevalier ChevalierNoch keine Bewertungen

- Valuation Gordon Growth ModelDokument25 SeitenValuation Gordon Growth ModelwaldyraeNoch keine Bewertungen

- Benefits of ULIPsDokument5 SeitenBenefits of ULIPsanand98809880Noch keine Bewertungen

- Warren Buffett's Latest Annual Letter 2018Dokument4 SeitenWarren Buffett's Latest Annual Letter 2018maheshtech760% (1)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 2009-01-14Dokument16 Seiten2009-01-14Tufts DailyNoch keine Bewertungen