Das könnte Ihnen auch gefallen

- Eine Liebesgeschichte PDFDokument49 SeitenEine Liebesgeschichte PDFCarolina Queiroz100% (3)

- Conversation - 1. I Live in Pasadena PDFDokument1 SeiteConversation - 1. I Live in Pasadena PDFCarolina QueirozNoch keine Bewertungen

- Checking Into The Hotel - Conversation 3 PDFDokument1 SeiteChecking Into The Hotel - Conversation 3 PDFCarolina QueirozNoch keine Bewertungen

- Checking Into The Hotel - Conversation 1 PDFDokument1 SeiteChecking Into The Hotel - Conversation 1 PDFCarolina QueirozNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Building g5Dokument45 SeitenBuilding g5ammarsteel68Noch keine Bewertungen

- Plantas Con Madre Plants That Teach and PDFDokument15 SeitenPlantas Con Madre Plants That Teach and PDFJetNoch keine Bewertungen

- Leadership Nursing and Patient SafetyDokument172 SeitenLeadership Nursing and Patient SafetyRolena Johnette B. PiñeroNoch keine Bewertungen

- Milestone BillingDokument3 SeitenMilestone BillingJagadeesh Kumar RayuduNoch keine Bewertungen

- Program Need Analysis Questionnaire For DKA ProgramDokument6 SeitenProgram Need Analysis Questionnaire For DKA ProgramAzman Bin TalibNoch keine Bewertungen

- ParaphrasingDokument11 SeitenParaphrasingAntiiSukmaNoch keine Bewertungen

- Highway Journal Feb 2023Dokument52 SeitenHighway Journal Feb 2023ShaileshRastogiNoch keine Bewertungen

- Yaskawa V7 ManualsDokument155 SeitenYaskawa V7 ManualsAnonymous GbfoQcCNoch keine Bewertungen

- Day 2 - Evident's Official ComplaintDokument18 SeitenDay 2 - Evident's Official ComplaintChronicle Herald100% (1)

- SUNGLAO - TM PortfolioDokument60 SeitenSUNGLAO - TM PortfolioGIZELLE SUNGLAONoch keine Bewertungen

- DLL - English 5 - Q3 - W8Dokument8 SeitenDLL - English 5 - Q3 - W8Merlyn S. Al-osNoch keine Bewertungen

- RMC No. 122 2022 9.6.2022Dokument6 SeitenRMC No. 122 2022 9.6.2022RUFO BULILANNoch keine Bewertungen

- Introduction To Templates in C++Dokument16 SeitenIntroduction To Templates in C++hammarbytpNoch keine Bewertungen

- Editorial WritingDokument38 SeitenEditorial WritingMelanie Antonio - Paino100% (1)

- TOK Assessed Student WorkDokument10 SeitenTOK Assessed Student WorkPeter Jun Park100% (1)

- Module 0-Course Orientation: Objectives OutlineDokument2 SeitenModule 0-Course Orientation: Objectives OutlineEmmanuel CausonNoch keine Bewertungen

- Pin Joint en PDFDokument1 SeitePin Joint en PDFCicNoch keine Bewertungen

- Trainer Manual Internal Quality AuditDokument32 SeitenTrainer Manual Internal Quality AuditMuhammad Erwin Yamashita100% (5)

- SCHEMA - Amsung 214TDokument76 SeitenSCHEMA - Amsung 214TmihaiNoch keine Bewertungen

- Model Personal StatementDokument2 SeitenModel Personal StatementSwayam Tripathy100% (1)

- Calculus of Finite Differences: Andreas KlappeneckerDokument30 SeitenCalculus of Finite Differences: Andreas KlappeneckerSouvik RoyNoch keine Bewertungen

- Activity 6 Product Disassembly ChartDokument5 SeitenActivity 6 Product Disassembly Chartapi-504977947Noch keine Bewertungen

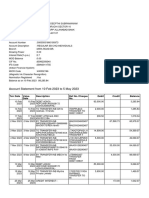

- Feb-May SBI StatementDokument2 SeitenFeb-May SBI StatementAshutosh PandeyNoch keine Bewertungen

- Case StudyDokument15 SeitenCase StudyChaitali moreyNoch keine Bewertungen

- M4110 Leakage Reactance InterfaceDokument2 SeitenM4110 Leakage Reactance InterfaceGuru MishraNoch keine Bewertungen

- Car Section 2 Series (H) Part-IiDokument6 SeitenCar Section 2 Series (H) Part-Iipandurang nalawadeNoch keine Bewertungen

- Ccie R&s Expanded-BlueprintDokument12 SeitenCcie R&s Expanded-BlueprintAftab AlamNoch keine Bewertungen

- Normal Consistency of Hydraulic CementDokument15 SeitenNormal Consistency of Hydraulic CementApril Lyn SantosNoch keine Bewertungen

- Asian Paints Final v1Dokument20 SeitenAsian Paints Final v1Mukul MundleNoch keine Bewertungen

- IJISRT23JUL645Dokument11 SeitenIJISRT23JUL645International Journal of Innovative Science and Research TechnologyNoch keine Bewertungen