Das könnte Ihnen auch gefallen

- Why Is Trust A "Hot Topic"?Dokument32 SeitenWhy Is Trust A "Hot Topic"?hariselvarajNoch keine Bewertungen

- Jobspeak Report Mar 2018Dokument12 SeitenJobspeak Report Mar 2018hariselvarajNoch keine Bewertungen

- Scheme OF Industry Institute Partnership Cell (IIPC) : All India Council For Technical EducationDokument28 SeitenScheme OF Industry Institute Partnership Cell (IIPC) : All India Council For Technical EducationhariselvarajNoch keine Bewertungen

- 8ecbb1 2Dokument1 Seite8ecbb1 2hariselvarajNoch keine Bewertungen

- Executive Program in Leadership: The Effective Use of Power: For More Information: HTTPS://WWW - Gsb.stanford - Edu/exec-EdDokument1 SeiteExecutive Program in Leadership: The Effective Use of Power: For More Information: HTTPS://WWW - Gsb.stanford - Edu/exec-EdhariselvarajNoch keine Bewertungen

- Journal of Small Business Management Oct 1997 35, 4 ABI/INFORM GlobalDokument12 SeitenJournal of Small Business Management Oct 1997 35, 4 ABI/INFORM GlobalhariselvarajNoch keine Bewertungen

- Protection of Women Against Domestic Violence Act, 2005Dokument31 SeitenProtection of Women Against Domestic Violence Act, 2005hariselvarajNoch keine Bewertungen

- Case Study Method 1Dokument7 SeitenCase Study Method 1hariselvarajNoch keine Bewertungen

- Abstract (Abstract) : Dheensaw, Cleve - Times - Colonist Victoria, B.C. (Victoria, B.C) 12 Feb 1999: C7Dokument4 SeitenAbstract (Abstract) : Dheensaw, Cleve - Times - Colonist Victoria, B.C. (Victoria, B.C) 12 Feb 1999: C7hariselvarajNoch keine Bewertungen

- US SurveyDokument3 SeitenUS SurveyhariselvarajNoch keine Bewertungen

- Room No. Designation Name Rly Tel No. (Off.) Rly Tel No. (Resi)Dokument32 SeitenRoom No. Designation Name Rly Tel No. (Off.) Rly Tel No. (Resi)hariselvarajNoch keine Bewertungen

- 3 - Identifying A Research ProblemDokument19 Seiten3 - Identifying A Research ProblemhariselvarajNoch keine Bewertungen

- Generation Bites BrochureDokument16 SeitenGeneration Bites BrochurehariselvarajNoch keine Bewertungen

- Lecture Method 1Dokument6 SeitenLecture Method 1hariselvarajNoch keine Bewertungen

- Without A Second: Infinith Infinith Infinith Infinithooooughts Ughts Ughts UghtsDokument2 SeitenWithout A Second: Infinith Infinith Infinith Infinithooooughts Ughts Ughts UghtshariselvarajNoch keine Bewertungen

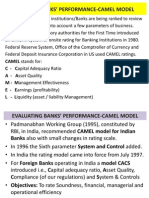

- Evaluating Banks' Performance-Camel ModelDokument8 SeitenEvaluating Banks' Performance-Camel ModelhariselvarajNoch keine Bewertungen

- HR AuditDokument4 SeitenHR AudithariselvarajNoch keine Bewertungen

- How Strong ManDokument4 SeitenHow Strong ManhariselvarajNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Indus Valley Annual Report 2022Dokument102 SeitenIndus Valley Annual Report 2022BharathNoch keine Bewertungen

- Assessing The Influence of Self-Efficacy On Entrepreneurial Intentions of Social EntrepreneursDokument76 SeitenAssessing The Influence of Self-Efficacy On Entrepreneurial Intentions of Social EntrepreneursDeisy Rabe LlantoNoch keine Bewertungen

- The Big Shot 2.0: Centre of EntrepreneurshipDokument5 SeitenThe Big Shot 2.0: Centre of EntrepreneurshipBhavya BansalNoch keine Bewertungen

- How To Start A Business Ultimate GuideDokument31 SeitenHow To Start A Business Ultimate GuideJean Fajardo BadilloNoch keine Bewertungen

- Why Startups Fail YcombinatorDokument18 SeitenWhy Startups Fail YcombinatorJohn PatlolNoch keine Bewertungen

- Beyond Licensing and IncubatorsDokument6 SeitenBeyond Licensing and IncubatorsThe Ewing Marion Kauffman FoundationNoch keine Bewertungen

- The Mom Test enDokument122 SeitenThe Mom Test enalirahebiNoch keine Bewertungen

- A Study On Women Entrepreneurs: Opportunities and Challenges in StartupDokument13 SeitenA Study On Women Entrepreneurs: Opportunities and Challenges in StartupAnkit VermaNoch keine Bewertungen

- REC@nnect Startup Boot Camp BrochureDokument72 SeitenREC@nnect Startup Boot Camp BrochureyuritziacostaNoch keine Bewertungen

- ILOwcms 191929Dokument167 SeitenILOwcms 191929Cece ChecheNoch keine Bewertungen

- A Phenomenological Study of The Lived ExperiencesDokument9 SeitenA Phenomenological Study of The Lived ExperiencesKyla ManaloNoch keine Bewertungen

- Global Online MBADokument38 SeitenGlobal Online MBAProtelcom EcuadorNoch keine Bewertungen

- Reasons Behind Success and Failures of Startups in Mysore CityDokument15 SeitenReasons Behind Success and Failures of Startups in Mysore Citysatish rajNoch keine Bewertungen

- Airbnb Growth StoryDokument38 SeitenAirbnb Growth StoryAvi jainNoch keine Bewertungen

- Mini Case Crowdfunding KenyaDokument11 SeitenMini Case Crowdfunding KenyaAhmed El KhateebNoch keine Bewertungen

- Systematic Literature Review of Critical Success Factors of Information Technology StartupsDokument23 SeitenSystematic Literature Review of Critical Success Factors of Information Technology StartupsAldo PutraNoch keine Bewertungen

- Granut Oil Product TionDokument18 SeitenGranut Oil Product TionAsk Melody100% (1)

- Entrepreneurship and Unemployment Edited.Dokument12 SeitenEntrepreneurship and Unemployment Edited.Shamseddine KebbeNoch keine Bewertungen

- Unit 2 The CompanyDokument4 SeitenUnit 2 The CompanyMai AnhNoch keine Bewertungen

- 52, 53 SMU MBA Assignment IV SemDokument119 Seiten52, 53 SMU MBA Assignment IV SemRanjan PalNoch keine Bewertungen

- FoodTech in Europe EN PDFDokument82 SeitenFoodTech in Europe EN PDFxavier marcenacNoch keine Bewertungen

- Dejen TVT Collage Project Proposal ofDokument38 SeitenDejen TVT Collage Project Proposal ofAbela DrrsNoch keine Bewertungen

- Sample Business PlanDokument5 SeitenSample Business Planpadmoretiara0Noch keine Bewertungen

- 10 Funding Options To Raise Startup Capital For BusinessDokument32 Seiten10 Funding Options To Raise Startup Capital For BusinessAnjani Kumar SinhaNoch keine Bewertungen

- WEEK 2-3 Introduction To Technologies For Entrepreneurship: IT14 TechnopreneurshipDokument24 SeitenWEEK 2-3 Introduction To Technologies For Entrepreneurship: IT14 TechnopreneurshipDylan AlbuquerqueNoch keine Bewertungen

- Intrep Module 1Dokument65 SeitenIntrep Module 1Wendy SoyosaNoch keine Bewertungen

- Business QuizDokument35 SeitenBusiness Quizdivya kalraNoch keine Bewertungen

- City of Chicago CWB Initiative ReportDokument48 SeitenCity of Chicago CWB Initiative ReportCameron BarnesNoch keine Bewertungen

- AIR2022 Web Online Final 211022Dokument266 SeitenAIR2022 Web Online Final 211022mark ceasarNoch keine Bewertungen

- Timeless Ventures PDFDokument43 SeitenTimeless Ventures PDFJohn SeyferthNoch keine Bewertungen