Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- ERPLO DeemedExport 200614 0653 1304Dokument4 SeitenERPLO DeemedExport 200614 0653 1304SivaprasadVasireddyNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- ERP SAP Rel471Dokument46 SeitenERP SAP Rel471Albet StrausNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- SAP Shortcut Keys PDFDokument5 SeitenSAP Shortcut Keys PDFHarish KumarNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Material MM User ManualDokument314 SeitenMaterial MM User ManualPushparaj PatelNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Updating The Details in Table... : Sudharsanan SDokument2 SeitenUpdating The Details in Table... : Sudharsanan SAlbet StrausNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Kee Engine LogDokument41 SeitenKee Engine LogAlbet StrausNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Rfq-Sap MMDokument12 SeitenRfq-Sap MMashish sawantNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Export/Import Process: Dipak MukherjeeDokument1 SeiteExport/Import Process: Dipak MukherjeeAlbet StrausNoch keine Bewertungen

- Rfq-Sap MMDokument12 SeitenRfq-Sap MMashish sawantNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- W Bs DictionaryDokument321 SeitenW Bs DictionaryAlbet StrausNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Mysap Healthcare Focus AreassDokument19 SeitenMysap Healthcare Focus AreassAlbet StrausNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- EY-Indirect Tax 2014Dokument100 SeitenEY-Indirect Tax 2014manNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- How To Check If SAP Note Is Already AppliedDokument2 SeitenHow To Check If SAP Note Is Already AppliedAlbet StrausNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- SAP Is H HealthCareDokument8 SeitenSAP Is H HealthCareAlbet StrausNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- SAP Patient Management: The Patient-Centric SolutionDokument24 SeitenSAP Patient Management: The Patient-Centric SolutionAlbet StrausNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Holiday List - 2015: Holiday Date Day DescriptionDokument1 SeiteHoliday List - 2015: Holiday Date Day DescriptionAlbet StrausNoch keine Bewertungen

- SAP S Solution Portfolio For The Healthcare CommunityDokument41 SeitenSAP S Solution Portfolio For The Healthcare CommunityAlbet StrausNoch keine Bewertungen

- TRDokument3 SeitenTRAlbet StrausNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- A1 UpdationDokument2 SeitenA1 UpdationAlbet StrausNoch keine Bewertungen

- NCERT Class 12 Accountancy Part 2Dokument329 SeitenNCERT Class 12 Accountancy Part 2KishorVedpathak100% (2)

- SM G7102Dokument129 SeitenSM G7102Albet StrausNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- WBS StructureDokument10 SeitenWBS StructureAlbet StrausNoch keine Bewertungen

- Std11 Acct EMDokument159 SeitenStd11 Acct EMniaz1788100% (1)

- NCERT Class 11 Accountancy Part 2Dokument296 SeitenNCERT Class 11 Accountancy Part 2AnoojxNoch keine Bewertungen

- India Localization With Respect To SD: T.MuthyalappaDokument77 SeitenIndia Localization With Respect To SD: T.MuthyalappadavinkuNoch keine Bewertungen

- Find Out T-Code in Different Ways in SPRODokument9 SeitenFind Out T-Code in Different Ways in SPROAlbet StrausNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

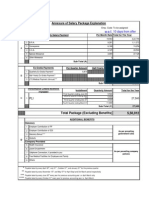

- Annexure of Salary Package Explanation: Emp. Code To Be AssignedDokument1 SeiteAnnexure of Salary Package Explanation: Emp. Code To Be AssignedAlbet StrausNoch keine Bewertungen

- CBSC Class XI - Accounting For BusinessDokument228 SeitenCBSC Class XI - Accounting For BusinessSachin KheveriaNoch keine Bewertungen

- Std11 Acct EMDokument159 SeitenStd11 Acct EMniaz1788100% (1)

- Provisional Selct List Neet-Ug 2021 Round-2Dokument88 SeitenProvisional Selct List Neet-Ug 2021 Round-2Debopriya BhattacharjeeNoch keine Bewertungen

- CarfaxDokument7 SeitenCarfaxAnonymous wvAFftNGNSNoch keine Bewertungen

- Cambridge International AS & A Level: SOCIOLOGY 9699/41Dokument4 SeitenCambridge International AS & A Level: SOCIOLOGY 9699/41maharanaanauyaNoch keine Bewertungen

- Gardner DenverDokument25 SeitenGardner DenverConstantin WellsNoch keine Bewertungen

- 559 Big Landlord Tenant OutlineDokument89 Seiten559 Big Landlord Tenant Outlinemoury227100% (1)

- DetailsDokument28 SeitenDetailsNeerajNoch keine Bewertungen

- Iso-Iec 19770-1Dokument2 SeitenIso-Iec 19770-1Ajai Srivastava50% (2)

- Capitalism Vs SocialismDokument14 SeitenCapitalism Vs Socialismrajesh_scribd1984100% (1)

- VM PresentationDokument29 SeitenVM Presentationoshin charuNoch keine Bewertungen

- Cai Wu v. Atty Gen USA, 3rd Cir. (2010)Dokument5 SeitenCai Wu v. Atty Gen USA, 3rd Cir. (2010)Scribd Government DocsNoch keine Bewertungen

- GC University, Faisalabad: Controller of Examinations Affiliated Institutions Semester ExaminationsDokument1 SeiteGC University, Faisalabad: Controller of Examinations Affiliated Institutions Semester ExaminationsIrfan Mohammad IrfanNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Order Granting Motion For Entry of DefaultDokument8 SeitenOrder Granting Motion For Entry of DefaultJames Alan Bush100% (2)

- Memo Writing WorkshopDokument17 SeitenMemo Writing Workshopkcope412Noch keine Bewertungen

- National Human Rights CommissionDokument15 SeitenNational Human Rights CommissionVDNoch keine Bewertungen

- Lifetime License ApplicationDokument2 SeitenLifetime License ApplicationBibhaas ojhaNoch keine Bewertungen

- Text of CorrectionDokument3 SeitenText of CorrectionKim Chung Trần Thị0% (1)

- Solution To Ch14 P13 Build A ModelDokument6 SeitenSolution To Ch14 P13 Build A ModelALI HAIDERNoch keine Bewertungen

- Spark Notes - Julius Caesar - Themes, Motifs & SymbolsDokument3 SeitenSpark Notes - Julius Caesar - Themes, Motifs & SymbolsLeonis MyrtilNoch keine Bewertungen

- Filipinas Synthetic Fiber Corporation vs. CA, Cta, and CirDokument1 SeiteFilipinas Synthetic Fiber Corporation vs. CA, Cta, and CirmwaikeNoch keine Bewertungen

- Evidence Case DigestDokument4 SeitenEvidence Case DigestBrenda de la GenteNoch keine Bewertungen

- Contreras V MacaraigDokument4 SeitenContreras V MacaraigDanilo Dela ReaNoch keine Bewertungen

- Program From Ncip MaeDokument3 SeitenProgram From Ncip Maeset netNoch keine Bewertungen

- Napolcom ReviewerDokument23 SeitenNapolcom ReviewerEmsNoch keine Bewertungen

- Plextol R 4152Dokument1 SeitePlextol R 4152Phạm Việt DũngNoch keine Bewertungen

- First Amended Complaint Stardock v. Paul Reiche and Fred FordDokument98 SeitenFirst Amended Complaint Stardock v. Paul Reiche and Fred FordPolygondotcomNoch keine Bewertungen

- Adjusting EntryDokument38 SeitenAdjusting EntryNicaela Margareth YusoresNoch keine Bewertungen

- DUTY of Counsel - ClientDokument30 SeitenDUTY of Counsel - ClientKhairul Iman78% (9)

- Loan SyndicationDokument57 SeitenLoan SyndicationSandya Gundeti100% (1)

- II Bauböck 2006Dokument129 SeitenII Bauböck 2006OmarNoch keine Bewertungen

- My Phillips Family 000-010Dokument138 SeitenMy Phillips Family 000-010Joni Coombs-HaynesNoch keine Bewertungen

- Arizona, Utah & New Mexico: A Guide to the State & National ParksVon EverandArizona, Utah & New Mexico: A Guide to the State & National ParksBewertung: 4 von 5 Sternen4/5 (1)

- The Bahamas a Taste of the Islands ExcerptVon EverandThe Bahamas a Taste of the Islands ExcerptBewertung: 4 von 5 Sternen4/5 (1)