Das könnte Ihnen auch gefallen

- Investment Appraisal: A Simple IntroductionVon EverandInvestment Appraisal: A Simple IntroductionBewertung: 4 von 5 Sternen4/5 (6)

- How A Company Is Valued - An Overview of Valuation Methods and Their Application PDFDokument20 SeitenHow A Company Is Valued - An Overview of Valuation Methods and Their Application PDFopopppoNoch keine Bewertungen

- Applied Corporate Finance. What is a Company worth?Von EverandApplied Corporate Finance. What is a Company worth?Bewertung: 3 von 5 Sternen3/5 (2)

- Capital BudgetingDokument20 SeitenCapital BudgetingHazel MigalbinNoch keine Bewertungen

- Presented By: Muhammad Taimoor Baig Uzair-ul-Atiq Kashif Bashir Salman Zafar Syed Ali RazaDokument40 SeitenPresented By: Muhammad Taimoor Baig Uzair-ul-Atiq Kashif Bashir Salman Zafar Syed Ali RazaSalman ZafarNoch keine Bewertungen

- Chapter 4 Share ValuationDokument18 SeitenChapter 4 Share ValuationAlamgir MollahNoch keine Bewertungen

- Corporate Valuation Mod IDokument29 SeitenCorporate Valuation Mod IRavichandran RamadassNoch keine Bewertungen

- ValuationDokument7 SeitenValuationSiva SankariNoch keine Bewertungen

- Module 2 CVR Notes PDFDokument8 SeitenModule 2 CVR Notes PDFDr. Shalini H SNoch keine Bewertungen

- Business Valuation MethodsDokument1 SeiteBusiness Valuation MethodsanusuyakrishnanNoch keine Bewertungen

- Task 3 - Investment AppraisalDokument12 SeitenTask 3 - Investment AppraisalYashmi BhanderiNoch keine Bewertungen

- Corporate AccountingDokument17 SeitenCorporate AccountingShriyaNoch keine Bewertungen

- Valuations & Acquisitions CMDokument9 SeitenValuations & Acquisitions CMnsnhemachenaNoch keine Bewertungen

- Navjeet Singh SobtiDokument18 SeitenNavjeet Singh SobtiShreyans GirathNoch keine Bewertungen

- What Is Stock ValuationDokument3 SeitenWhat Is Stock ValuationGeralyn RefugioNoch keine Bewertungen

- Financial Feasibility StudyDokument13 SeitenFinancial Feasibility StudyAriadne Ramos CorderoNoch keine Bewertungen

- Valuation of Target CompanyDokument25 SeitenValuation of Target Companym.shahnawaz0% (2)

- Valuation MethodsDokument21 SeitenValuation Methodsbluisss100% (1)

- Residual Income ValuationDokument6 SeitenResidual Income ValuationKumar AbhishekNoch keine Bewertungen

- CapitDokument8 SeitenCapitjanice100% (1)

- ABC&EVADokument20 SeitenABC&EVAArjun SubhashNoch keine Bewertungen

- 7 Lecture Performance Measurement & CompensationDokument20 Seiten7 Lecture Performance Measurement & CompensationJingwen YangNoch keine Bewertungen

- Corporate Valuation and Value Based ManagementDokument10 SeitenCorporate Valuation and Value Based ManagementjhatpatzeroNoch keine Bewertungen

- Valuation AcquisitionDokument4 SeitenValuation AcquisitionKnt Nallasamy GounderNoch keine Bewertungen

- IAPM Unit 2 - Fundamental AnalysisDokument27 SeitenIAPM Unit 2 - Fundamental AnalysisArpita ArtaniNoch keine Bewertungen

- Techniques of Investment AnalysisDokument32 SeitenTechniques of Investment AnalysisPranjal Verma0% (1)

- Unit 4 IAPM FM 01Dokument42 SeitenUnit 4 IAPM FM 01areumkim261Noch keine Bewertungen

- Why Value Stocks?: R (R) R + B (E (R) - R)Dokument8 SeitenWhy Value Stocks?: R (R) R + B (E (R) - R)Vishal AgarwalNoch keine Bewertungen

- Merrill Lynch 2007 Analyst Valuation TrainingDokument74 SeitenMerrill Lynch 2007 Analyst Valuation TrainingJose Garcia100% (21)

- Unit 1 Theory - Business ValuationDokument7 SeitenUnit 1 Theory - Business ValuationPrathmesh AmbulkarNoch keine Bewertungen

- Business ValuationDokument8 SeitenBusiness ValuationKomalNoch keine Bewertungen

- Fixed Assets, DepreciationDokument30 SeitenFixed Assets, Depreciationnahar570Noch keine Bewertungen

- Market-Based Valuation Method - BLK 3Dokument34 SeitenMarket-Based Valuation Method - BLK 3Kim GeminoNoch keine Bewertungen

- Economic FeasibilityDokument40 SeitenEconomic FeasibilityKristoffer Jesus Lopez OrdoñoNoch keine Bewertungen

- Valuation Mergers and AcquisitionDokument41 SeitenValuation Mergers and AcquisitionSubrahmanya Sringeri100% (1)

- Valuation Methods Used in Mergers & Acquisition: Roshankumar S PimpalkarDokument6 SeitenValuation Methods Used in Mergers & Acquisition: Roshankumar S PimpalkarSharad KumarNoch keine Bewertungen

- Value Measurement PresentationDokument18 SeitenValue Measurement Presentationrishit_93Noch keine Bewertungen

- Valuation Theory M& ADokument6 SeitenValuation Theory M& AbharatNoch keine Bewertungen

- Assignment On FaseelDokument6 SeitenAssignment On FaseelAbdul KhanNoch keine Bewertungen

- Share ValuationDokument7 SeitenShare ValuationroseNoch keine Bewertungen

- Resumen FinancesDokument11 SeitenResumen Financesfranchesca guillenNoch keine Bewertungen

- Buyer 3Dokument3 SeitenBuyer 3Arjit GuptaNoch keine Bewertungen

- Nism CH 10Dokument13 SeitenNism CH 10Darshan JainNoch keine Bewertungen

- Acca F9 Business ValuationsDokument6 SeitenAcca F9 Business ValuationsHaseeb SethyNoch keine Bewertungen

- Final FSA Exam PreparationDokument3 SeitenFinal FSA Exam PreparationHannah ZhangNoch keine Bewertungen

- Corporate Valuation - 2-V-2 - Module - 2 and 3Dokument11 SeitenCorporate Valuation - 2-V-2 - Module - 2 and 3Ravichandran RamadassNoch keine Bewertungen

- Capital BudgetingDokument16 SeitenCapital BudgetingNikhil BapnaNoch keine Bewertungen

- Regulatory EnvironmentDokument63 SeitenRegulatory EnvironmentAayushi AroraNoch keine Bewertungen

- Dinda Putri Novanti - Summary Measuring and Controlling Asset EmployedDokument5 SeitenDinda Putri Novanti - Summary Measuring and Controlling Asset EmployedDinda Putri NovantiNoch keine Bewertungen

- Financial Modelling Shareholder Value CreationDokument6 SeitenFinancial Modelling Shareholder Value Creationshubhagyaldh6253Noch keine Bewertungen

- Return On Investment: Assignment-2Dokument7 SeitenReturn On Investment: Assignment-2Vineet AgrawalNoch keine Bewertungen

- Equity AnalysisDokument6 SeitenEquity AnalysisVarsha Sukhramani100% (1)

- ACF Long AnswersDokument14 SeitenACF Long AnswersTwinkle ChettriNoch keine Bewertungen

- 10 ProfitabilityDokument15 Seiten10 ProfitabilityJamaica May SuficienciaNoch keine Bewertungen

- Capital Budgeting 2Dokument102 SeitenCapital Budgeting 2atharpimt100% (1)

- Shareholder Value Creation: An OverviewDokument5 SeitenShareholder Value Creation: An OverviewggeettNoch keine Bewertungen

- NotesFMF FinalDokument52 SeitenNotesFMF FinalKyrelle Mae LozadaNoch keine Bewertungen

- ICAI Corporate ValuationDokument47 SeitenICAI Corporate Valuationqamaraleem1_25038318Noch keine Bewertungen

- Rupee ConvertabiliryDokument6 SeitenRupee ConvertabilirySanthosh PrabhuNoch keine Bewertungen

- Human Resource PlanningDokument12 SeitenHuman Resource PlanningSanthosh PrabhuNoch keine Bewertungen

- KamranAhmad 2661 13278 1/session 6Dokument40 SeitenKamranAhmad 2661 13278 1/session 6Anum AhmadNoch keine Bewertungen

- Chapter 1 LawDokument58 SeitenChapter 1 LawSanthosh PrabhuNoch keine Bewertungen

- Karnataka Minimum Wage 2016-17 PDFDokument133 SeitenKarnataka Minimum Wage 2016-17 PDFSanthosh Prabhu100% (2)

- Factory Act Draft PDFDokument71 SeitenFactory Act Draft PDFsarvansasNoch keine Bewertungen

- 2 Industrial Dispute Act 1947Dokument155 Seiten2 Industrial Dispute Act 1947Santhosh PrabhuNoch keine Bewertungen

- Human Resource PlanningDokument12 SeitenHuman Resource PlanningSanthosh PrabhuNoch keine Bewertungen

- Performance AppraisalDokument42 SeitenPerformance AppraisalSanthosh PrabhuNoch keine Bewertungen

- Corporate CrimeDokument47 SeitenCorporate CrimeSanthosh Prabhu100% (1)

- Payment of Bonus Act 19651Dokument36 SeitenPayment of Bonus Act 19651Santhosh Prabhu100% (1)

- Liberalization Privatization GlobalizationDokument23 SeitenLiberalization Privatization GlobalizationSanthosh PrabhuNoch keine Bewertungen

- Rupee ConvertabiliryDokument6 SeitenRupee ConvertabilirySanthosh PrabhuNoch keine Bewertungen

- Financial Statement & Ratio AnalysisDokument37 SeitenFinancial Statement & Ratio AnalysisNeha BhayaniNoch keine Bewertungen

- The Factories Act 1948Dokument9 SeitenThe Factories Act 1948Gokul VattackattuNoch keine Bewertungen

- Introduction To Entrepreneurship: Unlocking The Secrets of Wealth Creation April 16, 2011Dokument61 SeitenIntroduction To Entrepreneurship: Unlocking The Secrets of Wealth Creation April 16, 2011Santhosh PrabhuNoch keine Bewertungen

- Job Analysis and Job DesignDokument40 SeitenJob Analysis and Job DesignSanthosh PrabhuNoch keine Bewertungen

- Inventory ManagementDokument17 SeitenInventory ManagementSanthosh PrabhuNoch keine Bewertungen

- Social Responsibility of Business and Business EthicsDokument48 SeitenSocial Responsibility of Business and Business EthicsSanthosh Prabhu100% (1)

- Tax Avoidance 5.4Dokument13 SeitenTax Avoidance 5.4Santhosh PrabhuNoch keine Bewertungen

- 12 Chapter 5Dokument39 Seiten12 Chapter 5Santhosh PrabhuNoch keine Bewertungen

- The Factories Act 1948Dokument9 SeitenThe Factories Act 1948Gokul VattackattuNoch keine Bewertungen

- Income Tax Slabs Rates For AY 2016-17 PDFDokument5 SeitenIncome Tax Slabs Rates For AY 2016-17 PDFSanthosh PrabhuNoch keine Bewertungen

- C2 Recruitment1Dokument118 SeitenC2 Recruitment1Santhosh PrabhuNoch keine Bewertungen

- MNCDokument44 SeitenMNCSanthosh Prabhu100% (1)

- Labour MarketDokument22 SeitenLabour MarketSanthosh PrabhuNoch keine Bewertungen

- Current Affairs Questions Answers February 2016 PDFDokument54 SeitenCurrent Affairs Questions Answers February 2016 PDFSanthosh Prabhu100% (1)

- FMDokument11 SeitenFMSanthosh PrabhuNoch keine Bewertungen

- Chapter 1 LawDokument19 SeitenChapter 1 LawSanthosh PrabhuNoch keine Bewertungen

- Case StudyDokument17 SeitenCase StudySanthosh Prabhu100% (1)

- KLBFDokument2 SeitenKLBFKhaerudin RangersNoch keine Bewertungen

- FM Graphs and Ratios TableDokument10 SeitenFM Graphs and Ratios TableNehal SharmaNoch keine Bewertungen

- 12th ACCOUNTANCY MATERIAL 2022-23Dokument29 Seiten12th ACCOUNTANCY MATERIAL 2022-23GANEShNoch keine Bewertungen

- Akuntansi KeuanganDokument20 SeitenAkuntansi KeuanganCenxi TVNoch keine Bewertungen

- Assets Non-Current Assets: Equity and Liabilities Share Capital and ReservesDokument10 SeitenAssets Non-Current Assets: Equity and Liabilities Share Capital and ReservesM Bilal KNoch keine Bewertungen

- W Final ExamDokument42 SeitenW Final ExamAnna TaylorNoch keine Bewertungen

- Copia de Caso Healthy Bear 2022Dokument4 SeitenCopia de Caso Healthy Bear 2022rataNoch keine Bewertungen

- Corporate Finance Present ValueDokument37 SeitenCorporate Finance Present ValueTalib DoaNoch keine Bewertungen

- AC 301 - CH 8 HWDokument2 SeitenAC 301 - CH 8 HWsaladinikNoch keine Bewertungen

- (C) Present Value of Future Benefits: Multiple Choice Questions (MCQS)Dokument8 Seiten(C) Present Value of Future Benefits: Multiple Choice Questions (MCQS)Z the officerNoch keine Bewertungen

- 5 Herman Miller Presentation Group Final 1Dokument31 Seiten5 Herman Miller Presentation Group Final 1lynklynkNoch keine Bewertungen

- Break-Even Analysis Unit IiDokument24 SeitenBreak-Even Analysis Unit IiAjeeth KumarNoch keine Bewertungen

- Inventory Cost Flow Deadline Aug 23 PDFDokument7 SeitenInventory Cost Flow Deadline Aug 23 PDFGrace ReyesNoch keine Bewertungen

- Chapter 2 Cost Terms, Concepts, and ClassificationsDokument4 SeitenChapter 2 Cost Terms, Concepts, and ClassificationsQurat SaboorNoch keine Bewertungen

- Accounting For Income TaxDokument4 SeitenAccounting For Income TaxRed YuNoch keine Bewertungen

- Closing and Post-Closing EntriesDokument13 SeitenClosing and Post-Closing EntriesBrian Reyes GangcaNoch keine Bewertungen

- Tugas Ke 2Dokument2 SeitenTugas Ke 2Laras atiNoch keine Bewertungen

- Accountancy Set 1 QPDokument6 SeitenAccountancy Set 1 QPShaurya JainNoch keine Bewertungen

- Bài tập lớnDokument9 SeitenBài tập lớnHà Chi NguyễnNoch keine Bewertungen

- Corporate Finance Case 2 ამხოსნაDokument3 SeitenCorporate Finance Case 2 ამხოსნაIrakli SaliaNoch keine Bewertungen

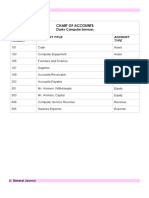

- ACTIVITY 2. Setting Up of Chart of Accounts and Journalizing of Entries ActivityDokument2 SeitenACTIVITY 2. Setting Up of Chart of Accounts and Journalizing of Entries Activityfernandez 4Noch keine Bewertungen

- Consolidated Financial StatementsDokument29 SeitenConsolidated Financial StatementsPramad BhattacharjeeNoch keine Bewertungen

- IMT - Ceres - Tarun Singh ChauhanDokument6 SeitenIMT - Ceres - Tarun Singh ChauhanTarun Singh ChauhanNoch keine Bewertungen

- Acctg EquationDokument8 SeitenAcctg EquationAlma Dimaranan-AcuñaNoch keine Bewertungen

- Relevant CostingDokument3 SeitenRelevant CostingMaria DyNoch keine Bewertungen

- Unit 7-Income TaxesDokument4 SeitenUnit 7-Income TaxesJean Pierre IsipNoch keine Bewertungen

- Computation of Income: Nazneen Mohammed Javed ShaikhDokument3 SeitenComputation of Income: Nazneen Mohammed Javed ShaikhRahul RampalNoch keine Bewertungen

- Cost of Capital ExcercisesDokument3 SeitenCost of Capital ExcercisesLinh Ha Nguyen Khanh100% (1)

- Principle of Accounting I Final ExamDokument3 SeitenPrinciple of Accounting I Final ExamAbrha Giday100% (4)

- Nike Case AnalysisDokument9 SeitenNike Case AnalysisUyen Thao Dang96% (54)