Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Case Study Royal Bank of CanadaDokument10 SeitenCase Study Royal Bank of Canadandgharat100% (1)

- Quick Revisionary NoteDokument22 SeitenQuick Revisionary Noteshivamdubey12Noch keine Bewertungen

- The Role of SEBI in Corporate GovernanceDokument8 SeitenThe Role of SEBI in Corporate GovernanceHarshit Sultania100% (1)

- What Is Order of Operations - Definition, Facts & ExampleDokument7 SeitenWhat Is Order of Operations - Definition, Facts & Examplepujarze2Noch keine Bewertungen

- Kostantinos Constas Gust MICHALOS 1866-1928 - Ancestry®Dokument4 SeitenKostantinos Constas Gust MICHALOS 1866-1928 - Ancestry®pujarze2Noch keine Bewertungen

- Symbols Adinkra and VeVeDokument4 SeitenSymbols Adinkra and VeVepujarze2100% (1)

- The Vodou Dead - Baron, Brijit and GedeDokument3 SeitenThe Vodou Dead - Baron, Brijit and Gedepujarze2100% (1)

- Understanding The Science of Yoga: January 2011Dokument12 SeitenUnderstanding The Science of Yoga: January 2011pujarze2Noch keine Bewertungen

- Fundamentals of College AlgebraDokument130 SeitenFundamentals of College Algebrapujarze2Noch keine Bewertungen

- Fundamentals of College AlgebraDokument107 SeitenFundamentals of College Algebrapujarze2Noch keine Bewertungen

- Male Porn Stars Share Their Secrets For Staying Hard On Set - Men's HealthDokument9 SeitenMale Porn Stars Share Their Secrets For Staying Hard On Set - Men's Healthpujarze2Noch keine Bewertungen

- Martin Coleman Archives - Seo HelruneDokument6 SeitenMartin Coleman Archives - Seo Helrunepujarze2100% (1)

- Using Restorex: Pathright Medical Recommends The FollowingDokument8 SeitenUsing Restorex: Pathright Medical Recommends The Followingpujarze2Noch keine Bewertungen

- Vodou Flags PDFDokument24 SeitenVodou Flags PDFpujarze2Noch keine Bewertungen

- Male Pelvic Floor - Advanced Massage and Bodywork PDFDokument6 SeitenMale Pelvic Floor - Advanced Massage and Bodywork PDFpujarze2Noch keine Bewertungen

- The Bent Middle Finger - Opinions and Viewpoints. - God Given GlyphsDokument2 SeitenThe Bent Middle Finger - Opinions and Viewpoints. - God Given Glyphspujarze2Noch keine Bewertungen

- I Tried A Penis Extender To Make My Penis Longer. Here's What HappenedDokument11 SeitenI Tried A Penis Extender To Make My Penis Longer. Here's What Happenedpujarze2Noch keine Bewertungen

- How To Fix An Anterior Tilt in The Pelvis - Tips For The Therapist & ClientDokument14 SeitenHow To Fix An Anterior Tilt in The Pelvis - Tips For The Therapist & Clientpujarze2Noch keine Bewertungen

- Weighted Average Cost of CapitalDokument20 SeitenWeighted Average Cost of CapitalSamuel NjengaNoch keine Bewertungen

- Exam Practice Question MBADokument11 SeitenExam Practice Question MBAsudhakar dhunganaNoch keine Bewertungen

- ASSIGNMENT 1 - HDI - Janki Solanki - 1813051Dokument57 SeitenASSIGNMENT 1 - HDI - Janki Solanki - 1813051Janki SolankiNoch keine Bewertungen

- Mba Project On LoanDokument47 SeitenMba Project On Loanshuhel100% (1)

- VouchingDokument2 SeitenVouchingguptrakeshNoch keine Bewertungen

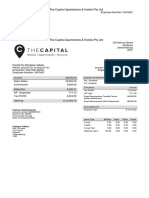

- Payslip 2023-07-31Dokument1 SeitePayslip 2023-07-31Elmarie Elize SmithNoch keine Bewertungen

- Acc 107 Finals Quiz 3Dokument1 SeiteAcc 107 Finals Quiz 3Jezz CulangNoch keine Bewertungen

- Corporate Tax Planning PDFDokument152 SeitenCorporate Tax Planning PDFdimple0% (1)

- Ind-AS 19Dokument42 SeitenInd-AS 19amarNoch keine Bewertungen

- 2-4 Audited Financial StatementsDokument9 Seiten2-4 Audited Financial StatementsJustine Joyce GabiaNoch keine Bewertungen

- Capital Structure - 1Dokument25 SeitenCapital Structure - 1bakhtiar2014Noch keine Bewertungen

- SGCH 12Dokument13 SeitenSGCH 12Charles John CatanNoch keine Bewertungen

- Business Strategy, Corporate Restructuring and Take Overs - R. Ramesh ChandraDokument36 SeitenBusiness Strategy, Corporate Restructuring and Take Overs - R. Ramesh ChandraDominic GouveiaNoch keine Bewertungen

- Form 1607022022 205546Dokument2 SeitenForm 1607022022 205546Mahesh VayiboyinaNoch keine Bewertungen

- Comprehensive Financial PaperDokument17 SeitenComprehensive Financial PaperIvy Joy UbinaNoch keine Bewertungen

- Air Canada V CIRDokument2 SeitenAir Canada V CIRnilesrevillaNoch keine Bewertungen

- Milan D Smith Financial Disclosure Report For 2010Dokument16 SeitenMilan D Smith Financial Disclosure Report For 2010Judicial Watch, Inc.Noch keine Bewertungen

- Q3 - Financial Accounting and Reporting (Partnership Accounting) All About Partnership DissolutionDokument3 SeitenQ3 - Financial Accounting and Reporting (Partnership Accounting) All About Partnership DissolutionALMA MORENANoch keine Bewertungen

- TR 47Dokument2 SeitenTR 47Anoop Chandran SavithriNoch keine Bewertungen

- CIR Vs Gen FoodsDokument12 SeitenCIR Vs Gen FoodsOlivia JaneNoch keine Bewertungen

- Contract of LeaseDokument6 SeitenContract of LeaseNombs NomNoch keine Bewertungen

- Working Capital Management - PharmaDokument26 SeitenWorking Capital Management - PharmaKshitij MittalNoch keine Bewertungen

- Internship Report On Meezan Bank Limited Mansehra Road Branch Abbottabad (1501)Dokument9 SeitenInternship Report On Meezan Bank Limited Mansehra Road Branch Abbottabad (1501)Faisal AwanNoch keine Bewertungen

- Eeff Kallpa q2-2023Dokument25 SeitenEeff Kallpa q2-2023carlos cribilleroNoch keine Bewertungen

- Executive Summary: 1.1 ObjectivesDokument24 SeitenExecutive Summary: 1.1 Objectivesakarsh_devNoch keine Bewertungen

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDokument1 SeiteIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruKaustabha DasNoch keine Bewertungen

- Chapter1 Final 1Dokument96 SeitenChapter1 Final 1Mạnh Đỗ ĐứcNoch keine Bewertungen