Das könnte Ihnen auch gefallen

- Ultra Vires Banks On Credit Loans and Void Contracts PDFDokument11 SeitenUltra Vires Banks On Credit Loans and Void Contracts PDFMartialArtist24100% (2)

- Secured Transactions: UCC Title 9Dokument17 SeitenSecured Transactions: UCC Title 9Rebel X86% (7)

- Super Day Secrets - Your Technical Interview GuideDokument24 SeitenSuper Day Secrets - Your Technical Interview GuideJithin RajanNoch keine Bewertungen

- Mini Case On Risk Return 1-SolutionDokument27 SeitenMini Case On Risk Return 1-Solutionjagrutic_09Noch keine Bewertungen

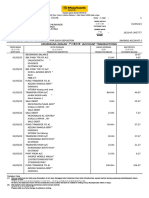

- Account Summary - 7382041247: ChecksDokument4 SeitenAccount Summary - 7382041247: ChecksJack SheldenNoch keine Bewertungen

- FEMA - Summary NotesDokument29 SeitenFEMA - Summary NotesCognitive BiasNoch keine Bewertungen

- Grade 5 English Module 1 FinalDokument19 SeitenGrade 5 English Module 1 FinalAlicia Nhs100% (4)

- Modified Put Butterfly - FidelityDokument6 SeitenModified Put Butterfly - FidelityNarendra BholeNoch keine Bewertungen

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsVon EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNoch keine Bewertungen

- Enterprise Risk Management A Complete Guide - 2019 EditionVon EverandEnterprise Risk Management A Complete Guide - 2019 EditionNoch keine Bewertungen

- Return and RiskDokument20 SeitenReturn and Riskdkriray100% (1)

- CFA Standards of Practice SummaryDokument12 SeitenCFA Standards of Practice SummaryAnonymous r99U5dPw5Noch keine Bewertungen

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryDokument19 SeitenCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiNoch keine Bewertungen

- Bond Valuations:: What Does "Bond Valuation" Mean?Dokument7 SeitenBond Valuations:: What Does "Bond Valuation" Mean?SandeepNoch keine Bewertungen

- Chapter 1 (Role of Financial Markets and Institutions)Dokument25 SeitenChapter 1 (Role of Financial Markets and Institutions)Momenul Islam Mridha Murad100% (2)

- Commercial Bank of EthiopiaDokument3 SeitenCommercial Bank of EthiopiaEmiru ayalew100% (1)

- 08 - Chapter 8Dokument71 Seiten08 - Chapter 8hunkieNoch keine Bewertungen

- Capital Asset Pricing Model and Modern Portfolio TheoryDokument12 SeitenCapital Asset Pricing Model and Modern Portfolio TheorylordaiztrandNoch keine Bewertungen

- Security Analysis: Chapter - 1Dokument47 SeitenSecurity Analysis: Chapter - 1Harsh GuptaNoch keine Bewertungen

- Chapter 6 - Time Value of MoneyDokument7 SeitenChapter 6 - Time Value of MoneyJean EliaNoch keine Bewertungen

- Capital Structure: Theory and PolicyDokument31 SeitenCapital Structure: Theory and PolicySuraj ShelarNoch keine Bewertungen

- Risk and ReturnDokument46 SeitenRisk and ReturnPavanNoch keine Bewertungen

- Business Research Methods ZikmundDokument28 SeitenBusiness Research Methods ZikmundSyed Rehan AhmedNoch keine Bewertungen

- Gitman Pmf13 Ppt08 GEDokument56 SeitenGitman Pmf13 Ppt08 GESajjad AhmadNoch keine Bewertungen

- Financial Statement Analysis PPT 3427Dokument25 SeitenFinancial Statement Analysis PPT 3427imroz_alamNoch keine Bewertungen

- M09 Gitman50803X 14 MF C09Dokument56 SeitenM09 Gitman50803X 14 MF C09dhfbbbbbbbbbbbbbbbbbhNoch keine Bewertungen

- Chapter 07 - Optimal Risky PortfoliosDokument62 SeitenChapter 07 - Optimal Risky PortfoliosJerine TanNoch keine Bewertungen

- Cost of Capital Lecture Slides in PDF FormatDokument18 SeitenCost of Capital Lecture Slides in PDF FormatLucy UnNoch keine Bewertungen

- Solutions Chap007Dokument13 SeitenSolutions Chap007Said Ur RahmanNoch keine Bewertungen

- Presentation Insurance PPTDokument11 SeitenPresentation Insurance PPTshuchiNoch keine Bewertungen

- Cost of CapitalDokument55 SeitenCost of CapitalSaritasaruNoch keine Bewertungen

- CH 05Dokument48 SeitenCH 05Ali SyedNoch keine Bewertungen

- Gitman 08Dokument30 SeitenGitman 08Samar Abdel RahmanNoch keine Bewertungen

- Assignment 3Dokument7 SeitenAssignment 3Abdullah ghauriNoch keine Bewertungen

- Financial Management 2: UCP-001BDokument3 SeitenFinancial Management 2: UCP-001BRobert RamirezNoch keine Bewertungen

- NESTLE Global StrategyDokument1 SeiteNESTLE Global StrategyMomenul Islam Mridha Murad100% (3)

- Accounting AnalysisDokument15 SeitenAccounting AnalysisMonoarul IslamNoch keine Bewertungen

- Capital StructureDokument24 SeitenCapital StructureSiddharth GautamNoch keine Bewertungen

- Practice Questions: Problem 1.1Dokument6 SeitenPractice Questions: Problem 1.1Micah Ng100% (1)

- Tax Quiz 4Dokument61 SeitenTax Quiz 4Seri CrisologoNoch keine Bewertungen

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsVon EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNoch keine Bewertungen

- Case AnalysisDokument3 SeitenCase AnalysisJoshua Adorco75% (12)

- Chapter 4 Financing Decisions PDFDokument72 SeitenChapter 4 Financing Decisions PDFChandra Bhatta100% (1)

- Discounted Cash Flow Valuation The Inputs: K.ViswanathanDokument47 SeitenDiscounted Cash Flow Valuation The Inputs: K.ViswanathanHardik VibhakarNoch keine Bewertungen

- CH 12 Cash Flow Estimatision and Risk AnalysisDokument39 SeitenCH 12 Cash Flow Estimatision and Risk AnalysisRidhoVerianNoch keine Bewertungen

- Chapter 07Dokument29 SeitenChapter 07LBL_LowkeeNoch keine Bewertungen

- Presentation 04 - Risk and Return 2012.11.15Dokument54 SeitenPresentation 04 - Risk and Return 2012.11.15SantaAgataNoch keine Bewertungen

- Chapter 6 Discounted Cash Flow ValuationDokument27 SeitenChapter 6 Discounted Cash Flow ValuationAhmed Fathelbab100% (1)

- Portfolio Selection Using Sharpe, Treynor & Jensen Performance IndexDokument15 SeitenPortfolio Selection Using Sharpe, Treynor & Jensen Performance Indexktkalai selviNoch keine Bewertungen

- Gitman pmf13 ppt05Dokument79 SeitenGitman pmf13 ppt05moonaafreenNoch keine Bewertungen

- Risk and Return AssignmentDokument2 SeitenRisk and Return AssignmentHuzaifa Bin SaeedNoch keine Bewertungen

- What's A Bond?: What's A Bond? Types of Bonds Bond Valuation Techniques The Bangladeshi Bond Market Problem SetDokument30 SeitenWhat's A Bond?: What's A Bond? Types of Bonds Bond Valuation Techniques The Bangladeshi Bond Market Problem SetpakhijuliNoch keine Bewertungen

- Chapter 11 - Cost of Capital - Text and End of Chapter QuestionsDokument63 SeitenChapter 11 - Cost of Capital - Text and End of Chapter QuestionsSaba Rajpoot50% (2)

- Chapter 10Dokument42 SeitenChapter 10LBL_LowkeeNoch keine Bewertungen

- Chapter 16Dokument23 SeitenChapter 16JJNoch keine Bewertungen

- Forward Rate AgreementDokument8 SeitenForward Rate AgreementNaveen BhatiaNoch keine Bewertungen

- Discounted Cash Flow (DCF) Definition - InvestopediaDokument2 SeitenDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532Noch keine Bewertungen

- CHP 6Dokument49 SeitenCHP 6Khaled A. M. El-sherifNoch keine Bewertungen

- Ross 9e FCF SMLDokument425 SeitenRoss 9e FCF SMLAlmayayaNoch keine Bewertungen

- Answers To Chapter 7 - Interest Rates and Bond ValuationDokument8 SeitenAnswers To Chapter 7 - Interest Rates and Bond ValuationbuwaleedNoch keine Bewertungen

- FM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFDokument28 SeitenFM CH 1natureoffinancialmanagement 120704104928 Phpapp01 PDFvasantharao100% (1)

- Corporate Finance and Investment AnalysisDokument80 SeitenCorporate Finance and Investment AnalysisCristina PopNoch keine Bewertungen

- Portfolio Management: Lecturer: Th.S. Le Phuoc Thanh (NCS)Dokument47 SeitenPortfolio Management: Lecturer: Th.S. Le Phuoc Thanh (NCS)Eli ZabethNoch keine Bewertungen

- CH 6 Making Capital Investment DecisionsDokument3 SeitenCH 6 Making Capital Investment DecisionsMuhammad abdul azizNoch keine Bewertungen

- Chapter 5Dokument28 SeitenChapter 5Shoaib ZaheerNoch keine Bewertungen

- Assignment 1 - Investment AnalysisDokument5 SeitenAssignment 1 - Investment Analysisphillimon zuluNoch keine Bewertungen

- BFC5935 - Tutorial 10 SolutionsDokument8 SeitenBFC5935 - Tutorial 10 SolutionsAlex YisnNoch keine Bewertungen

- Dillard R WK #7 Assignment Chapter 7Dokument2 SeitenDillard R WK #7 Assignment Chapter 7Rdillard12100% (1)

- Advanced Auditing Final Exam-Group QuestionsDokument12 SeitenAdvanced Auditing Final Exam-Group QuestionsAnna FlemingNoch keine Bewertungen

- Capital Budgeting Decisions A Clear and Concise ReferenceVon EverandCapital Budgeting Decisions A Clear and Concise ReferenceNoch keine Bewertungen

- Corporate Financial Analysis with Microsoft ExcelVon EverandCorporate Financial Analysis with Microsoft ExcelBewertung: 5 von 5 Sternen5/5 (1)

- Budgeting and Planning Complete Self-Assessment GuideVon EverandBudgeting and Planning Complete Self-Assessment GuideNoch keine Bewertungen

- Cost Of Capital A Complete Guide - 2020 EditionVon EverandCost Of Capital A Complete Guide - 2020 EditionBewertung: 4 von 5 Sternen4/5 (1)

- Credit Risk: Pricing, Measurement, and ManagementVon EverandCredit Risk: Pricing, Measurement, and ManagementBewertung: 1 von 5 Sternen1/5 (2)

- Business Research Methods: Information Systems and Knowledge ManagementDokument34 SeitenBusiness Research Methods: Information Systems and Knowledge ManagementNeha_Gupta_7619Noch keine Bewertungen

- Chapter 07 An Introduction To Portfolio Management Multiple Choice QuestionDokument19 SeitenChapter 07 An Introduction To Portfolio Management Multiple Choice QuestionMomenul Islam Mridha Murad100% (1)

- Cap 1Dokument74 SeitenCap 1Mej Beit Chabab100% (1)

- Weak-Form Efficiency Testimony of Dhaka Stock ExchangeDokument28 SeitenWeak-Form Efficiency Testimony of Dhaka Stock ExchangeMomenul Islam Mridha MuradNoch keine Bewertungen

- Globalization ImpactDokument2 SeitenGlobalization ImpactMomenul Islam Mridha MuradNoch keine Bewertungen

- Secondary Data Research in A Digital AgeDokument30 SeitenSecondary Data Research in A Digital AgeMomenul Islam Mridha MuradNoch keine Bewertungen

- Sample Designs and Sampling ProceduresDokument32 SeitenSample Designs and Sampling ProceduresMomenul Islam Mridha MuradNoch keine Bewertungen

- Survey ResearchDokument38 SeitenSurvey ResearchMomenul Islam Mridha MuradNoch keine Bewertungen

- Dispute Form PDFDokument1 SeiteDispute Form PDFJenn T LianNoch keine Bewertungen

- Activity Sheet 3 Ordinary AnnuityDokument4 SeitenActivity Sheet 3 Ordinary AnnuityFaith CalingoNoch keine Bewertungen

- BRPAT00098400000056652 NewDokument8 SeitenBRPAT00098400000056652 NewWorld WebNoch keine Bewertungen

- Ibs TMN Sri Serdang, S'Gor 1 31/05/23Dokument8 SeitenIbs TMN Sri Serdang, S'Gor 1 31/05/23jie skrttNoch keine Bewertungen

- Chapter 04 NotesDokument5 SeitenChapter 04 NotesNik Nur MunirahNoch keine Bewertungen

- GunsDokument2 SeitenGunsDaniela StoianNoch keine Bewertungen

- Kendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya DebbarmaDokument12 SeitenKendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya Debbarmaakash debbarmaNoch keine Bewertungen

- A Study On Performance Appraisal of Idbi Bank in IndiaDokument43 SeitenA Study On Performance Appraisal of Idbi Bank in Indiasj computersNoch keine Bewertungen

- Ultratech Balance SheetDokument2 SeitenUltratech Balance SheetPappu BhatiyaNoch keine Bewertungen

- Q Mar22Dokument9 SeitenQ Mar22user mrmysteryNoch keine Bewertungen

- Star Gifts and Promotions CC Postnet Suite 435 Privatebag X Lynnwoodrif 0040 Samanthak@Decadentgp - Co.ZaDokument4 SeitenStar Gifts and Promotions CC Postnet Suite 435 Privatebag X Lynnwoodrif 0040 Samanthak@Decadentgp - Co.ZaEmira FilaNoch keine Bewertungen

- SPDR Barclays Capital Intermediate Term Treasury ETF 1-10YDokument2 SeitenSPDR Barclays Capital Intermediate Term Treasury ETF 1-10YRoberto PerezNoch keine Bewertungen

- Kotak Mahindra Bank FinalDokument57 SeitenKotak Mahindra Bank FinalTejrajsinh100% (2)

- Introduction To FinanceDokument31 SeitenIntroduction To FinanceJean FlordelizNoch keine Bewertungen

- Barwa Real Estate Balance Sheet Particulars Note NoDokument28 SeitenBarwa Real Estate Balance Sheet Particulars Note NoMuhammad Irfan ZafarNoch keine Bewertungen

- Introduction of Banking SystemDokument10 SeitenIntroduction of Banking SystemMasy1210% (1)

- LAS ABM - FABM12 Ia B 1 Week 1Dokument9 SeitenLAS ABM - FABM12 Ia B 1 Week 1ROMMEL RABONoch keine Bewertungen

- Financial Performance Analysis of Lanka Bangla Finance Ltd.Dokument36 SeitenFinancial Performance Analysis of Lanka Bangla Finance Ltd.VagabondXiko50% (6)

- Accounting For Special TransactionDokument5 SeitenAccounting For Special TransactionNicole Gole CruzNoch keine Bewertungen