Das könnte Ihnen auch gefallen

- Chapter 3 - Accounting Cycle For Service EnterpriseDokument22 SeitenChapter 3 - Accounting Cycle For Service EnterpriseAnimaw YayehNoch keine Bewertungen

- Module 3 - The Adjusting ProcessDokument2 SeitenModule 3 - The Adjusting ProcessTBA PacificNoch keine Bewertungen

- Accounting 101 - Final Exam Part 4Dokument15 SeitenAccounting 101 - Final Exam Part 4AuroraNoch keine Bewertungen

- Ccounting Principles,: Weygandt, Kieso, & KimmelDokument58 SeitenCcounting Principles,: Weygandt, Kieso, & Kimmelpiash246100% (2)

- Chapter 3Dokument15 SeitenChapter 3clara2300181Noch keine Bewertungen

- Financial Reporting BasicsDokument30 SeitenFinancial Reporting BasicslelahakuNoch keine Bewertungen

- The Accounting EquationDokument49 SeitenThe Accounting EquationsweetEmie031Noch keine Bewertungen

- Principles of Accounting Help Lesson #4: Adjusting EntriesDokument23 SeitenPrinciples of Accounting Help Lesson #4: Adjusting EntriesRuffa Garcia100% (1)

- Adjusting Entries Lecture 301Dokument10 SeitenAdjusting Entries Lecture 301Tricia GorozaNoch keine Bewertungen

- Chapter 3 - The Adjusting ProcessDokument60 SeitenChapter 3 - The Adjusting ProcessAzrielNoch keine Bewertungen

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDokument131 SeitenFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Adjusting EntriesDokument23 SeitenAdjusting Entriestoobaahmedkhan100% (1)

- NLKTDokument25 SeitenNLKTBá Thiên Kim NguyễnNoch keine Bewertungen

- FabmDokument68 SeitenFabmAllyzza Jayne Abelido100% (1)

- ADJUSTING ENTRIES FOR FINANCIAL STATEMENTSDokument32 SeitenADJUSTING ENTRIES FOR FINANCIAL STATEMENTSAyniNuyda100% (1)

- POA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809amDokument65 SeitenPOA WK 7 LECT 2 VER 1 28032021 115402am 17112022 110442am 06052023 101809ammuhammad atifNoch keine Bewertungen

- Pleting The Accounting CycleDokument65 SeitenPleting The Accounting Cycleyow jing peiNoch keine Bewertungen

- Chapter-2 Accounting CycleDokument18 SeitenChapter-2 Accounting CycleTsegaye BelayNoch keine Bewertungen

- Fiscal vs Calendar Year Adjusting EntriesDokument9 SeitenFiscal vs Calendar Year Adjusting EntriesGmef Syme FerreraNoch keine Bewertungen

- Accounting Fundamentals ExplainedDokument77 SeitenAccounting Fundamentals ExplainedBernice Jayne MondingNoch keine Bewertungen

- ABM 1 - PPT - Chapter 4 - Recorded LectureDokument62 SeitenABM 1 - PPT - Chapter 4 - Recorded LectureCalyx OxfordNoch keine Bewertungen

- Ch03 WRD25e InstructorDokument70 SeitenCh03 WRD25e InstructorFiskal Reguler 15Noch keine Bewertungen

- Accounting Equation and Financial Statements ReviewDokument21 SeitenAccounting Equation and Financial Statements ReviewNeil Stechschulte100% (1)

- Adjusting Entries PDFDokument6 SeitenAdjusting Entries PDFJan ryanNoch keine Bewertungen

- Business School: ACCT1501 Accounting and Financial Management 1A Session 1 2015Dokument14 SeitenBusiness School: ACCT1501 Accounting and Financial Management 1A Session 1 2015Patricia ArgeseanuNoch keine Bewertungen

- ACCT220 Week 2 Homework ProblemsDokument22 SeitenACCT220 Week 2 Homework ProblemswilliamsNoch keine Bewertungen

- Financial Accounting Answers June 2022Dokument8 SeitenFinancial Accounting Answers June 2022sanhitaNoch keine Bewertungen

- Statement of Financial Position (SFP) : Lesson 1Dokument29 SeitenStatement of Financial Position (SFP) : Lesson 1Dianne Saragena100% (1)

- Financial Accounting Chapter 3: The Adjusting Process: The Accrual Basis of Accounting vs. The Cash Basis of AccountingDokument2 SeitenFinancial Accounting Chapter 3: The Adjusting Process: The Accrual Basis of Accounting vs. The Cash Basis of AccountingMardhiah RamlanNoch keine Bewertungen

- Adjusting EntriesDokument4 SeitenAdjusting EntriesNoj WerdnaNoch keine Bewertungen

- Ac101 ch3Dokument21 SeitenAc101 ch3Alex ChewNoch keine Bewertungen

- Adjusting EntriesDokument24 SeitenAdjusting EntriesHasnainNoch keine Bewertungen

- Mba Eekm W2Dokument28 SeitenMba Eekm W2Mon ThuNoch keine Bewertungen

- Financial Accounting Part 7Dokument43 SeitenFinancial Accounting Part 7dannydoly100% (2)

- Acc 100 Quiz AnswersDokument9 SeitenAcc 100 Quiz Answersscribdpdfs100% (1)

- Chapter 4 PowerpointDokument25 SeitenChapter 4 Powerpointapi-248607804Noch keine Bewertungen

- Final AccountDokument14 SeitenFinal AccountStiloflexindia Enterprise100% (1)

- WK 3 Accrual Accounting Concepts 2 Slides Per PageDokument23 SeitenWK 3 Accrual Accounting Concepts 2 Slides Per PageThùy Linh Lê Thị100% (1)

- Financial Accounting BasicsDokument24 SeitenFinancial Accounting BasicsMonirHRNoch keine Bewertungen

- Adjusting EntriesDokument27 SeitenAdjusting EntriesLien LaurethNoch keine Bewertungen

- Accounting & Financial AnalysisDokument35 SeitenAccounting & Financial AnalysisVishal Ranjan100% (2)

- Review of Ch 1 & 2 Key ConceptsDokument46 SeitenReview of Ch 1 & 2 Key ConceptsBookAddict721Noch keine Bewertungen

- BUS 501 Chapter 3Dokument72 SeitenBUS 501 Chapter 3Abu Tawbid Khan BadhanNoch keine Bewertungen

- 300 per monthDokument62 Seiten300 per monthNayeem Ahamed AdorNoch keine Bewertungen

- Chap2+3 1Dokument36 SeitenChap2+3 1Tarif IslamNoch keine Bewertungen

- Adjusting Entry - LectureDokument9 SeitenAdjusting Entry - LectureMaDine 19100% (2)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Dokument20 SeitenReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB Cloyd100% (1)

- Fabm 2 Week 1Dokument60 SeitenFabm 2 Week 1Camille Cornelio100% (1)

- Adjusting Quiz 6Dokument5 SeitenAdjusting Quiz 6Jyasmine Aura V. AgustinNoch keine Bewertungen

- Chapter 3 PresentationDokument48 SeitenChapter 3 Presentationhosie.oqbeNoch keine Bewertungen

- Financial Accounting NotesDokument27 SeitenFinancial Accounting NotesLauraNoch keine Bewertungen

- Acctng 1 - 1st Lecture PDFDokument31 SeitenAcctng 1 - 1st Lecture PDFJunlymar Rusiana CalumbaNoch keine Bewertungen

- Fundamentals of ABM1 - Q4 - LAS2 DRAFTDokument10 SeitenFundamentals of ABM1 - Q4 - LAS2 DRAFTSitti Halima Amilbahar AdgesNoch keine Bewertungen

- Adjusting Entries Explained for Accruals and PrepaymentsDokument3 SeitenAdjusting Entries Explained for Accruals and PrepaymentsJamie ToriagaNoch keine Bewertungen

- Basics of AccountingDokument38 SeitenBasics of AccountingAathirai AsokanNoch keine Bewertungen

- Lesson 2Dokument10 SeitenLesson 2Winoah HubaldeNoch keine Bewertungen

- PPT2-Adjusting The Accounts and Completing The Accounting CycleDokument46 SeitenPPT2-Adjusting The Accounts and Completing The Accounting CycleGriselda Aurelie100% (1)

- Financial Accounting and Reporting Study Guide NotesVon EverandFinancial Accounting and Reporting Study Guide NotesBewertung: 1 von 5 Sternen1/5 (1)

- Mid SemesterExam.Q ADokument4 SeitenMid SemesterExam.Q Ayow jing pei100% (4)

- Week1a.introduction To CourseDokument7 SeitenWeek1a.introduction To Courseyow jing peiNoch keine Bewertungen

- Week1b IntroductionDokument34 SeitenWeek1b Introductionyow jing peiNoch keine Bewertungen

- CHAPTER 3 - Accounting EquationDokument16 SeitenCHAPTER 3 - Accounting Equationyow jing pei100% (2)

- Ebf1013 Assignment 1 RatiosDokument2 SeitenEbf1013 Assignment 1 Ratiosyow jing peiNoch keine Bewertungen

- LedgerDokument4 SeitenLedgeryow jing peiNoch keine Bewertungen

- List of Companies ASSIGNMENT 1Dokument2 SeitenList of Companies ASSIGNMENT 1yow jing peiNoch keine Bewertungen

- Ebf1013 Assignment 1 RatiosDokument3 SeitenEbf1013 Assignment 1 Ratiosyow jing peiNoch keine Bewertungen

- Cash Flow StatementsDokument19 SeitenCash Flow Statementsyow jing peiNoch keine Bewertungen

- Week2a ManualDoubleEntrySystem PPTTPDokument40 SeitenWeek2a ManualDoubleEntrySystem PPTTPyow jing peiNoch keine Bewertungen

- Week3a.journals LedgersDokument10 SeitenWeek3a.journals Ledgersyow jing peiNoch keine Bewertungen

- Week1c.introduction - Exercises WithoutAnswersDokument8 SeitenWeek1c.introduction - Exercises WithoutAnswersyow jing peiNoch keine Bewertungen

- Week12 AccountingEthicsDokument15 SeitenWeek12 AccountingEthicsyow jing peiNoch keine Bewertungen

- Accounting Framework and ConceptsDokument30 SeitenAccounting Framework and Conceptsyow jing peiNoch keine Bewertungen

- Week2b.manualDoubleEntrySystem - Exercises WithoutAnswersDokument4 SeitenWeek2b.manualDoubleEntrySystem - Exercises WithoutAnswersyow jing peiNoch keine Bewertungen

- Week11 BudgetingDokument38 SeitenWeek11 Budgetingyow jing peiNoch keine Bewertungen

- Property, Plant & Equipment (Fixed Assets) : Reeve Warren DuchacDokument33 SeitenProperty, Plant & Equipment (Fixed Assets) : Reeve Warren Duchacyow jing peiNoch keine Bewertungen

- Warehouse Study Management ProjectDokument46 SeitenWarehouse Study Management Projectyow jing peiNoch keine Bewertungen

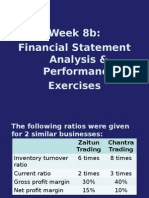

- Week 8: Financial Statement Analysis & PerformanceDokument41 SeitenWeek 8: Financial Statement Analysis & Performanceyow jing peiNoch keine Bewertungen

- Week7.Partnerships Corporations OtherOrganisationsDokument40 SeitenWeek7.Partnerships Corporations OtherOrganisationsyow jing peiNoch keine Bewertungen

- Supplier Relationship Management in The Context of Supply Chain ManagementDokument12 SeitenSupplier Relationship Management in The Context of Supply Chain Managementyow jing peiNoch keine Bewertungen

- Week6 AComprehensiveIllustrationDokument86 SeitenWeek6 AComprehensiveIllustrationyow jing pei89% (28)

- Pleting The Accounting CycleDokument65 SeitenPleting The Accounting Cycleyow jing peiNoch keine Bewertungen

- Week8b.financialStatementsAnalysis Performance - ExercisesDokument12 SeitenWeek8b.financialStatementsAnalysis Performance - Exercisesyow jing peiNoch keine Bewertungen

- Week6 SampleExamQuestionDokument16 SeitenWeek6 SampleExamQuestionyow jing pei67% (3)

- Week3c ReceivablesDokument14 SeitenWeek3c Receivablesyow jing peiNoch keine Bewertungen

- Supply Chain Management (3rd Edition)Dokument17 SeitenSupply Chain Management (3rd Edition)Shashank SharmaNoch keine Bewertungen

- Supply Chain Management: A Presentation by A.V. VedpuriswarDokument54 SeitenSupply Chain Management: A Presentation by A.V. Vedpuriswarramasb4uNoch keine Bewertungen

- Bank Reconciliation StatementDokument17 SeitenBank Reconciliation Statementyow jing pei100% (1)

- Philippine College Accountancy Program OverviewDokument19 SeitenPhilippine College Accountancy Program OverviewCharo Gironella67% (3)

- Ifrs Study Material 2021Dokument17 SeitenIfrs Study Material 2021Sagheer AhmedNoch keine Bewertungen

- SlyabusDokument7 SeitenSlyabusLlyod Francis LaylayNoch keine Bewertungen

- Accounting For Non-Profit OrganizationsDokument39 SeitenAccounting For Non-Profit Organizationsrevel_13193% (29)

- Introduction To Financial Statements 1Dokument22 SeitenIntroduction To Financial Statements 1Sarbani Mishra100% (1)

- Tar Ge T 100: JS AccountancyDokument33 SeitenTar Ge T 100: JS Accountancyvishal joshiNoch keine Bewertungen

- Arise AB (ARISE) : Financial and Strategic SWOT Analysis ReviewDokument34 SeitenArise AB (ARISE) : Financial and Strategic SWOT Analysis ReviewPartha SarathyNoch keine Bewertungen

- 20 Admission of PartnerDokument12 Seiten20 Admission of PartnerNadeem Manzoor100% (1)

- Interest Rate and RiskDokument42 SeitenInterest Rate and RiskchandoraNoch keine Bewertungen

- Review Handouts and Materials: Semester First Semester School Year 2019-2020 Subject Handout # TopicDokument34 SeitenReview Handouts and Materials: Semester First Semester School Year 2019-2020 Subject Handout # TopicWilson TanNoch keine Bewertungen

- Sample AssignmentDokument31 SeitenSample Assignmentits2kool50% (2)

- Chapter 31 Practical Acctg 1 ValixDokument10 SeitenChapter 31 Practical Acctg 1 ValixloiseNoch keine Bewertungen

- Dupont Analysis For The FinancialDokument19 SeitenDupont Analysis For The FinancialInternational Journal of Innovative Science and Research TechnologyNoch keine Bewertungen

- Infosys Stock Fundamental Analysis - Financial Results & Equity Research - Investyadnya Stock-o-MeterDokument7 SeitenInfosys Stock Fundamental Analysis - Financial Results & Equity Research - Investyadnya Stock-o-MeterPramod KulkarniNoch keine Bewertungen

- Deutsche BrauereiDokument22 SeitenDeutsche Brauereiusergurl0% (2)

- 09-DOH2020 Part2-Observations and RecommDokument100 Seiten09-DOH2020 Part2-Observations and RecommPamela Ledesma SusonNoch keine Bewertungen

- Acct Principles and Assumption - Week1Dokument4 SeitenAcct Principles and Assumption - Week1Hà Chi NguyễnNoch keine Bewertungen

- Report MIC 2022Dokument87 SeitenReport MIC 2022dwi handariniNoch keine Bewertungen

- Dwnload Full Cornerstones of Financial Accounting Canadian 2nd Edition Rich Test Bank PDFDokument35 SeitenDwnload Full Cornerstones of Financial Accounting Canadian 2nd Edition Rich Test Bank PDFjayden77evans100% (11)

- RMYC Cup 2 - RevDokument9 SeitenRMYC Cup 2 - RevJasper Andrew AdjaraniNoch keine Bewertungen

- Chap 12 - Cost of Capital - EditedDokument17 SeitenChap 12 - Cost of Capital - EditedRusselle Therese Daitol100% (1)

- FABM2 Mod2Dokument27 SeitenFABM2 Mod2Angelo PeraltaNoch keine Bewertungen

- SampaSoln EXCELDokument4 SeitenSampaSoln EXCELRasika Pawar-HaldankarNoch keine Bewertungen

- 03.1 The Case of The Unidentified Industries-2018Dokument2 Seiten03.1 The Case of The Unidentified Industries-2018maryam rizwanNoch keine Bewertungen

- Engineers India (ENGR IN) Rating: BUY | CMP: Rs108 | TP: Rs139Dokument7 SeitenEngineers India (ENGR IN) Rating: BUY | CMP: Rs108 | TP: Rs139Praveen KumarNoch keine Bewertungen

- Journalizing transactions and preparing a trial balanceDokument8 SeitenJournalizing transactions and preparing a trial balanceshowshang0% (1)

- Financial Accounting BasicsDokument63 SeitenFinancial Accounting BasicsCharu MalhotraNoch keine Bewertungen

- Plant Assets Chapter Study GuideDokument1 SeitePlant Assets Chapter Study GuideAcho Jie100% (1)

- Kani Na Gid Animal 1Dokument30 SeitenKani Na Gid Animal 1Jeane Mae BooNoch keine Bewertungen

- Project BS ItemsDokument25 SeitenProject BS ItemsSumeet BhatereNoch keine Bewertungen