Das könnte Ihnen auch gefallen

- Written Ananlysis and Communications-1Dokument10 SeitenWritten Ananlysis and Communications-1nivecNoch keine Bewertungen

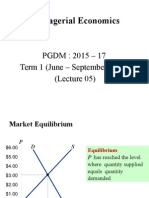

- Lecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationDokument80 SeitenLecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationnivecNoch keine Bewertungen

- Lecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationDokument80 SeitenLecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationnivecNoch keine Bewertungen

- Lecture 3 - Theory of FirmDokument15 SeitenLecture 3 - Theory of FirmnivecNoch keine Bewertungen

- Theory of The FirmDokument52 SeitenTheory of The FirmnivecNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- LP IV Lab Zdvzmanual Sem II fbsccAY 2019-20z 20-ConvxvzzertedDokument96 SeitenLP IV Lab Zdvzmanual Sem II fbsccAY 2019-20z 20-ConvxvzzertedVikas GuptaNoch keine Bewertungen

- Anticipate Problems Before They Emerge: White PaperDokument7 SeitenAnticipate Problems Before They Emerge: White PaperYotsapol KantaratNoch keine Bewertungen

- Product Differentiation and Market Segmentation As Alternative Marketing StrategiesDokument7 SeitenProduct Differentiation and Market Segmentation As Alternative Marketing StrategiesCaertiMNoch keine Bewertungen

- Linear Programming Models: Graphical and Computer MethodsDokument91 SeitenLinear Programming Models: Graphical and Computer MethodsFaith Reyna TanNoch keine Bewertungen

- Chapter 1 Critical Thin...Dokument7 SeitenChapter 1 Critical Thin...sameh06Noch keine Bewertungen

- CELTA Pre-Interview Grammar, Vocabulary and Pronunciation ExercisesDokument4 SeitenCELTA Pre-Interview Grammar, Vocabulary and Pronunciation ExercisesMichelJorge100% (2)

- HV 2Dokument80 SeitenHV 2Hafiz Mehroz KhanNoch keine Bewertungen

- Mitosis Quiz: Answers Each Question. Write The Answer On The Sheet ProvidedDokument5 SeitenMitosis Quiz: Answers Each Question. Write The Answer On The Sheet ProvidedJohn Osborne100% (1)

- Monetary System 1Dokument6 SeitenMonetary System 1priyankabgNoch keine Bewertungen

- Safety Data Sheet for Instant AdhesiveDokument6 SeitenSafety Data Sheet for Instant AdhesiveDiego S. FreitasNoch keine Bewertungen

- Mathematics Specimen Papers and Mark Schemes UG013054Dokument102 SeitenMathematics Specimen Papers and Mark Schemes UG013054minnie murphy86% (7)

- What Are Your Observations or Generalizations On How Text/ and or Images Are Presented?Dokument2 SeitenWhat Are Your Observations or Generalizations On How Text/ and or Images Are Presented?Darlene PanisaNoch keine Bewertungen

- Educating The PosthumanDokument50 SeitenEducating The PosthumanCatherine BrugelNoch keine Bewertungen

- Informed Consent: Ghaiath M. A. HusseinDokument26 SeitenInformed Consent: Ghaiath M. A. HusseinDocAxi Maximo Jr AxibalNoch keine Bewertungen

- Biology GCE 2010 June Paper 1 Mark SchemeDokument10 SeitenBiology GCE 2010 June Paper 1 Mark SchemeRicky MartinNoch keine Bewertungen

- Chick Lit: It's not a Gum, it's a Literary TrendDokument2 SeitenChick Lit: It's not a Gum, it's a Literary TrendspringzmeNoch keine Bewertungen

- V60 Ventilator Specifications PDFDokument4 SeitenV60 Ventilator Specifications PDFJonathan Issac Dominguez RamirezNoch keine Bewertungen

- Philosophy of Disciple Making PaperDokument5 SeitenPhilosophy of Disciple Making Paperapi-665038631Noch keine Bewertungen

- Laboratory SafetyDokument4 SeitenLaboratory SafetyLey DoydoraNoch keine Bewertungen

- PanimulaDokument4 SeitenPanimulaCharmayne DatorNoch keine Bewertungen

- Westford University College readies flagship campus with new programsDokument20 SeitenWestford University College readies flagship campus with new programsSaju JanardhananNoch keine Bewertungen

- BC Planning EvenDokument5 SeitenBC Planning EvenRuth KeziaNoch keine Bewertungen

- Compabloc Manual NewestDokument36 SeitenCompabloc Manual NewestAnonymous nw5AXJqjdNoch keine Bewertungen

- Readme cljM880fw 2305076 518488 PDFDokument37 SeitenReadme cljM880fw 2305076 518488 PDFjuan carlos MalagonNoch keine Bewertungen

- Component 2 Learner Statement Y2Dokument6 SeitenComponent 2 Learner Statement Y2api-426152133Noch keine Bewertungen

- Footprints 080311 For All Basic IcsDokument18 SeitenFootprints 080311 For All Basic IcsAmit PujarNoch keine Bewertungen

- Book 2 - Test 1Dokument2 SeitenBook 2 - Test 1Đức LongNoch keine Bewertungen

- 42U System Cabinet GuideDokument68 Seiten42U System Cabinet GuideGerman AndersNoch keine Bewertungen

- Color TheoryDokument28 SeitenColor TheoryEka HaryantoNoch keine Bewertungen

- Explore Spanish Lesson Plan - AnimalsDokument8 SeitenExplore Spanish Lesson Plan - Animalsapi-257582917Noch keine Bewertungen