Das könnte Ihnen auch gefallen

- Cost & Managerial Accounting II EssentialsVon EverandCost & Managerial Accounting II EssentialsBewertung: 4 von 5 Sternen4/5 (1)

- Module 3Dokument45 SeitenModule 3Gandeti SantoshNoch keine Bewertungen

- Ass. Om Prof 4. EleraDokument3 SeitenAss. Om Prof 4. EleraBA 13 Jun kateleen eleraNoch keine Bewertungen

- ECONOMICDokument2 SeitenECONOMICKimberly HipolitoNoch keine Bewertungen

- STRATA Reviewer 1Dokument6 SeitenSTRATA Reviewer 1Ria BagoNoch keine Bewertungen

- Q1.Solu:-: Fixed Budget:-A Budget Which Is Made Without Regard To PotentialDokument8 SeitenQ1.Solu:-: Fixed Budget:-A Budget Which Is Made Without Regard To PotentialkumarranachauhanNoch keine Bewertungen

- Chapter 7 - FullDokument35 SeitenChapter 7 - FullrasmimoqbelNoch keine Bewertungen

- Introduction To CostsDokument7 SeitenIntroduction To CostsLisaNoch keine Bewertungen

- Topic 2.2 - Financial Planning Learning Outcome The Aim of This Section Is For Students To Understand The FollowingDokument15 SeitenTopic 2.2 - Financial Planning Learning Outcome The Aim of This Section Is For Students To Understand The FollowinggeorgianaNoch keine Bewertungen

- Methos of PricingDokument18 SeitenMethos of PricingKhelin ShahNoch keine Bewertungen

- Marketing Management.Dokument12 SeitenMarketing Management.Purvi ShethNoch keine Bewertungen

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageVon EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageBewertung: 5 von 5 Sternen5/5 (1)

- Method of CostingDokument28 SeitenMethod of CostingMohammed Imran HossainNoch keine Bewertungen

- CHP 3.2 Costs and RevenuesDokument19 SeitenCHP 3.2 Costs and RevenuesDana MneimneNoch keine Bewertungen

- How To Price Your ProductDokument11 SeitenHow To Price Your ProductNayan MhetreNoch keine Bewertungen

- Cost AcctngDokument22 SeitenCost AcctngJINKY TOLENTINONoch keine Bewertungen

- Opportunity CostsDokument10 SeitenOpportunity CostsAditi WaliaNoch keine Bewertungen

- Ethan Menezes Fybcom B 088 Topic: Cost Analysis Busniess Economics 8928885792Dokument20 SeitenEthan Menezes Fybcom B 088 Topic: Cost Analysis Busniess Economics 8928885792The CarnageNoch keine Bewertungen

- Differential Analysis Lecture Notes 1Dokument18 SeitenDifferential Analysis Lecture Notes 1Yesaya SetiawanNoch keine Bewertungen

- Unit 4Dokument32 SeitenUnit 4Benjamin Adelwini BugriNoch keine Bewertungen

- Managerial Uses of BEPDokument31 SeitenManagerial Uses of BEPACADEMICS007Noch keine Bewertungen

- Strategic Cost Management - Semester SummaryDokument15 SeitenStrategic Cost Management - Semester SummaryivandimaunahannnNoch keine Bewertungen

- Admas University College of Business and Economics 2020: Chapter Five Relevant Information and Decision MakingDokument4 SeitenAdmas University College of Business and Economics 2020: Chapter Five Relevant Information and Decision MakingKalkidan SolomonNoch keine Bewertungen

- Pricing of Product PDFDokument17 SeitenPricing of Product PDFChinmay LearningNoch keine Bewertungen

- Unit - 4: Accounting and Economic CostsDokument21 SeitenUnit - 4: Accounting and Economic CostsRohit JoshiNoch keine Bewertungen

- MARGINAL COSTING (Ai1)Dokument13 SeitenMARGINAL COSTING (Ai1)Iris TitoNoch keine Bewertungen

- CASE STUDY REVENUEDokument15 SeitenCASE STUDY REVENUEbotato. exeNoch keine Bewertungen

- Chapter 4Dokument35 SeitenChapter 4AbdulAzeemNoch keine Bewertungen

- PricingDokument26 SeitenPricingDr. Smita ChoudharyNoch keine Bewertungen

- UNIT 5 - Pricing DecisionsDokument47 SeitenUNIT 5 - Pricing Decisionsp nishithaNoch keine Bewertungen

- Assignment 1Dokument11 SeitenAssignment 1Hai NinhNoch keine Bewertungen

- Fixed Cost ExamplesDokument2 SeitenFixed Cost ExamplesPratyay DasNoch keine Bewertungen

- Expense Forecasting: Jewel Bergonia Krystal Ontoy Claire RamirezDokument60 SeitenExpense Forecasting: Jewel Bergonia Krystal Ontoy Claire RamirezKrystal Ontoy100% (1)

- Cost Management Accounting April 2021Dokument10 SeitenCost Management Accounting April 2021Nageshwar SinghNoch keine Bewertungen

- MA MidtermDokument3 SeitenMA MidtermTRUNG NGUYỄN KIÊNNoch keine Bewertungen

- CostDokument11 SeitenCostBD EntertainmentNoch keine Bewertungen

- 4a - Decision Making and Marginal CostingDokument23 Seiten4a - Decision Making and Marginal CostingCindy ClollyNoch keine Bewertungen

- Types of Relevant CostsDokument5 SeitenTypes of Relevant CostsSheila Mae AramanNoch keine Bewertungen

- Target Costing Approach To PricingDokument11 SeitenTarget Costing Approach To Pricingarch1491Noch keine Bewertungen

- TLE ExploratoryCookery7 Q1M5Week6 OKDokument9 SeitenTLE ExploratoryCookery7 Q1M5Week6 OKAmelita Benignos OsorioNoch keine Bewertungen

- Chapter 5 Production of Goods and ServicesDokument11 SeitenChapter 5 Production of Goods and Serviceshey cuteNoch keine Bewertungen

- Cost & Management AccountingDokument9 SeitenCost & Management AccountingUdbhav ShuklaNoch keine Bewertungen

- Pricing Decisions and Cost ManagementDokument22 SeitenPricing Decisions and Cost ManagementDr. Alla Talal YassinNoch keine Bewertungen

- Chapter Two 1Dokument42 SeitenChapter Two 1AN NesNoch keine Bewertungen

- Topic 7Dokument23 SeitenTopic 7AB RomillaNoch keine Bewertungen

- Lec 1Dokument4 SeitenLec 1mbalajimeNoch keine Bewertungen

- Solution Manual For Managerial Accounting 5th Edition by JiambalvoDokument12 SeitenSolution Manual For Managerial Accounting 5th Edition by Jiambalvoa129714627Noch keine Bewertungen

- CVP Analysis - International Finance and AccountingDokument14 SeitenCVP Analysis - International Finance and AccountingJamesNoch keine Bewertungen

- Chapter 5 Cost ProductionDokument8 SeitenChapter 5 Cost ProductionMaria Teresa VillamayorNoch keine Bewertungen

- TERREL DAVIS - Test 3Dokument13 SeitenTERREL DAVIS - Test 3KEVIN GORDONNoch keine Bewertungen

- ICAEW - Valuing A BusinessDokument4 SeitenICAEW - Valuing A BusinessMyrefNoch keine Bewertungen

- Relevant - Costs Bac3 1Dokument17 SeitenRelevant - Costs Bac3 1Fë LïçïäNoch keine Bewertungen

- Pricing To Capture ValueDokument30 SeitenPricing To Capture ValueArshad RS100% (1)

- Princples - Pricing MethodsDokument16 SeitenPrincples - Pricing Methodsmusonza murwiraNoch keine Bewertungen

- Relevant Costs For Decision MakingDokument20 SeitenRelevant Costs For Decision Makingmisharahman100% (2)

- Cost & Management AccountingDokument10 SeitenCost & Management AccountingPoojaNoch keine Bewertungen

- Chapter 4Dokument20 SeitenChapter 4Aydin NajafovNoch keine Bewertungen

- The Key to Higher Profits: Pricing PowerVon EverandThe Key to Higher Profits: Pricing PowerBewertung: 5 von 5 Sternen5/5 (1)

- Pestel: Market Growth or Decline, Business Position, Potential and Direction For OperationsDokument32 SeitenPestel: Market Growth or Decline, Business Position, Potential and Direction For OperationsGuenane ImadNoch keine Bewertungen

- Canada Goose: Out There: Source: Case Studies On WARC, 2016Dokument5 SeitenCanada Goose: Out There: Source: Case Studies On WARC, 2016Guenane ImadNoch keine Bewertungen

- FINAL NPD ToolkitDokument100 SeitenFINAL NPD ToolkitGuenane ImadNoch keine Bewertungen

- Why Do You Study EnglishDokument9 SeitenWhy Do You Study EnglishGuenane ImadNoch keine Bewertungen

- Case6 GreatestFailureDokument7 SeitenCase6 GreatestFailureGuenane ImadNoch keine Bewertungen

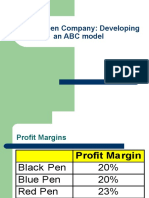

- Classic Pen Company: Developing An ABC ModelDokument22 SeitenClassic Pen Company: Developing An ABC Modeljk kumarNoch keine Bewertungen

- Project Profile On Assembly of Beverage Vending MachineDokument2 SeitenProject Profile On Assembly of Beverage Vending MachineHarshith KolurNoch keine Bewertungen

- Makerere University College of Business and Management Studies Master of Business AdministrationDokument15 SeitenMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidNoch keine Bewertungen

- Chapter03 E7Dokument99 SeitenChapter03 E7conanthegreat0293% (14)

- FEIA Mid-Term Assignment - FNPV: Year T 0 1 2 3 4 5 OutflowsDokument16 SeitenFEIA Mid-Term Assignment - FNPV: Year T 0 1 2 3 4 5 OutflowsMaurice ScholtesNoch keine Bewertungen

- Uniform Format of Accounts For Central Automnomous Bodies PDFDokument46 SeitenUniform Format of Accounts For Central Automnomous Bodies PDFsgirishri4044Noch keine Bewertungen

- Relevant Costing For Managerial DecisionsDokument25 SeitenRelevant Costing For Managerial DecisionsNikoNoch keine Bewertungen

- Bakery Industry Comilla, BangladeshDokument29 SeitenBakery Industry Comilla, BangladeshMd Tarek Rahman100% (1)

- Quick / Rapid Fire Batteries Case StudyDokument15 SeitenQuick / Rapid Fire Batteries Case StudyMd ShahidullahNoch keine Bewertungen

- Ch. 20Dokument8 SeitenCh. 20a_d_r_i_89Noch keine Bewertungen

- Transfer Pricing: Rodelio S. RoqueDokument19 SeitenTransfer Pricing: Rodelio S. Roqueterrence jacob diamaNoch keine Bewertungen

- Results Accountability - PPT NotesDokument72 SeitenResults Accountability - PPT NotesEmma WongNoch keine Bewertungen

- Impact Institute Report True Price of JeansDokument30 SeitenImpact Institute Report True Price of JeansMarco GaspariNoch keine Bewertungen

- Financial Control - 2 - Flexible Budgets and Variances - Webb Company With SolutionDokument5 SeitenFinancial Control - 2 - Flexible Budgets and Variances - Webb Company With SolutionQuang NhựtNoch keine Bewertungen

- CL-9 SAP AuthorizationDokument13 SeitenCL-9 SAP AuthorizationEVANoch keine Bewertungen

- Exterior ReportZone 2exterior ReportDokument2.008 SeitenExterior ReportZone 2exterior ReportwititterleyNoch keine Bewertungen

- Notes in Econ 351Dokument3 SeitenNotes in Econ 351이삐야Noch keine Bewertungen

- S23 MGMT 6139 Module 10 BrightView Plumbing and Heathing - A New Buisness ModelDokument10 SeitenS23 MGMT 6139 Module 10 BrightView Plumbing and Heathing - A New Buisness ModelVino DhanapalNoch keine Bewertungen

- Guidancet3 2 3Dokument40 SeitenGuidancet3 2 3jovanNoch keine Bewertungen

- Chapter 4 SpoilageDokument9 SeitenChapter 4 SpoilageKid bNoch keine Bewertungen

- Ch01 Managerial AccountingDokument7 SeitenCh01 Managerial AccountingIrdo KwanNoch keine Bewertungen

- MS-04 (Absorption & Variable Costing With Pricing Decisions)Dokument6 SeitenMS-04 (Absorption & Variable Costing With Pricing Decisions)yshizamNoch keine Bewertungen

- Managerial Accounting 2nd Edition Balakrishnan Solutions ManualDokument38 SeitenManagerial Accounting 2nd Edition Balakrishnan Solutions Manualnhattranel7k1100% (29)

- MSQ 03 Standard Costs and Variance Analysis BrylDokument13 SeitenMSQ 03 Standard Costs and Variance Analysis BrylDavid DavidNoch keine Bewertungen

- Chapter 3 Job Order CostingDokument20 SeitenChapter 3 Job Order Costingazam_rasheedNoch keine Bewertungen

- Profit, Loss, Alligation & MixturesDokument18 SeitenProfit, Loss, Alligation & MixturesVikasNoch keine Bewertungen

- Cost APProachDokument40 SeitenCost APProachMANNAVAN.T.N100% (1)

- Managerial Accounting PDFDokument350 SeitenManagerial Accounting PDFSalinaNoch keine Bewertungen

- 1st Term Acc9 HandoutDokument55 Seiten1st Term Acc9 HandoutMallet S. GacadNoch keine Bewertungen

- Variance AnalysisDokument51 SeitenVariance AnalysisAnonymous 5F68VLDbNoch keine Bewertungen