Das könnte Ihnen auch gefallen

- Rothschild Analyst TrainingDokument667 SeitenRothschild Analyst TrainingNina Sng92% (26)

- The Portable MBA in Finance and AccountingVon EverandThe Portable MBA in Finance and AccountingBewertung: 4 von 5 Sternen4/5 (19)

- Fa4e SM Ch01Dokument21 SeitenFa4e SM Ch01michaelkwok1100% (1)

- Federal Reserve Lien Ammended AgainDokument3 SeitenFederal Reserve Lien Ammended AgainCharles Scott0% (1)

- Foundations of Entrepreneurship: Basic Accounting and Financial StatementsDokument89 SeitenFoundations of Entrepreneurship: Basic Accounting and Financial StatementsTejaswi BandlamudiNoch keine Bewertungen

- BAB 7 Cash Flow AnalyisisDokument19 SeitenBAB 7 Cash Flow AnalyisisMaun GovillianNoch keine Bewertungen

- Presentation of Financial Statements: The Auditor's ReviewDokument20 SeitenPresentation of Financial Statements: The Auditor's ReviewzulfiNoch keine Bewertungen

- ACCA P2 (International) : Course OverviewDokument121 SeitenACCA P2 (International) : Course OverviewJoseNoch keine Bewertungen

- The Chartered Institute of Taxation of Nigeria (CITN)Dokument48 SeitenThe Chartered Institute of Taxation of Nigeria (CITN)Fred OnyemenamNoch keine Bewertungen

- Corporate Financial ReportingDokument6 SeitenCorporate Financial ReportingAsadvirkNoch keine Bewertungen

- Presentation of Financial Statements: The Auditor S ReviewDokument20 SeitenPresentation of Financial Statements: The Auditor S ReviewPrem ManoNoch keine Bewertungen

- Chapter 8Dokument31 SeitenChapter 8Shirah CoolNoch keine Bewertungen

- Practical Financial ReportingDokument17 SeitenPractical Financial ReportingkambertusNoch keine Bewertungen

- Oracle Hyperion Financial ManagementDokument45 SeitenOracle Hyperion Financial Managementmalleswar7Noch keine Bewertungen

- Cash Flow - Wikipedia, The Free EncyclopediaDokument4 SeitenCash Flow - Wikipedia, The Free EncyclopediaSachinsuhaNoch keine Bewertungen

- Chapter 1Dokument40 SeitenChapter 1Galata NugusaNoch keine Bewertungen

- Advanced Financial Reporting: RevisionDokument44 SeitenAdvanced Financial Reporting: Revisionmy VinayNoch keine Bewertungen

- Ifrs Indian ContextDokument7 SeitenIfrs Indian ContextKumar Sachin DeoNoch keine Bewertungen

- Accounting Standards (Satyanath Mohapatra)Dokument39 SeitenAccounting Standards (Satyanath Mohapatra)smrutiranjan swain100% (1)

- Cash Flow StatementDokument12 SeitenCash Flow StatementChikwason Sarcozy MwanzaNoch keine Bewertungen

- Accounting Standards IndiaDokument49 SeitenAccounting Standards IndiaDivij KumarNoch keine Bewertungen

- Deshare Explore Search You Slideshare Upload Login Signup Search Submit Search Home Explore Sharelikesave Next SlidesharesDokument6 SeitenDeshare Explore Search You Slideshare Upload Login Signup Search Submit Search Home Explore Sharelikesave Next SlidesharesGrowing BiznizNoch keine Bewertungen

- LMT School of Management, Thapar University Masters of Business AdministrationDokument21 SeitenLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhNoch keine Bewertungen

- Other Measurement and Disclosure Issues: Tenth Canadian EditionDokument53 SeitenOther Measurement and Disclosure Issues: Tenth Canadian EditionEli SaNoch keine Bewertungen

- AAOIFI Vs IFRS: Accounting For Islamic FinanceDokument11 SeitenAAOIFI Vs IFRS: Accounting For Islamic FinanceMuhammad Faisal Kamarul ZamanNoch keine Bewertungen

- Finance, Chapter 5Dokument5 SeitenFinance, Chapter 5myapple1994Noch keine Bewertungen

- CH 17Dokument4 SeitenCH 17lamarbawazeerrNoch keine Bewertungen

- of US Cma Part 1Dokument75 Seitenof US Cma Part 1mohammed100% (1)

- Unit 22 - Financial Statement Analysis Introduction - 2013Dokument13 SeitenUnit 22 - Financial Statement Analysis Introduction - 2013cytishNoch keine Bewertungen

- Chapter 7 - Cash Flow AnalysisDokument18 SeitenChapter 7 - Cash Flow AnalysisulfaNoch keine Bewertungen

- Income Statement and Statement of Cash FlowsDokument29 SeitenIncome Statement and Statement of Cash FlowsNadine Santiago100% (1)

- Chapter 1 Part A - Student SlidesDokument48 SeitenChapter 1 Part A - Student Slidesrebeccahf7Noch keine Bewertungen

- The Income Statement and Statement of Cash Flows: ObjectivesDokument29 SeitenThe Income Statement and Statement of Cash Flows: ObjectivesteshomeNoch keine Bewertungen

- Cash Flow and Financial PlanningDokument64 SeitenCash Flow and Financial PlanningAmjad J AliNoch keine Bewertungen

- FRA - v5Dokument20 SeitenFRA - v5Hamid KhurshidNoch keine Bewertungen

- 8A. Role of AccountingDokument11 Seiten8A. Role of AccountingsymhoutNoch keine Bewertungen

- Financial StatementsDokument6 SeitenFinancial Statementsvenkatch220% (1)

- Basic Financial Accounting PPT 1Dokument26 SeitenBasic Financial Accounting PPT 1anon_254280391100% (1)

- Statement of Changes in Financial Position: Cash Flow StatementDokument25 SeitenStatement of Changes in Financial Position: Cash Flow StatementCharu Arora100% (1)

- Chapter 3 - Cash Flow Analysis - SVDokument26 SeitenChapter 3 - Cash Flow Analysis - SVNguyen LienNoch keine Bewertungen

- Module 8 (Albay)Dokument43 SeitenModule 8 (Albay)randyblanza2014Noch keine Bewertungen

- Oracle Hyperion Financial ManagementDokument45 SeitenOracle Hyperion Financial Managementkonda83Noch keine Bewertungen

- CH - 05 Statement of Cash FlowsDokument26 SeitenCH - 05 Statement of Cash FlowsOwais Zaman100% (1)

- EBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and CoronavirusDokument24 SeitenEBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirusks frNoch keine Bewertungen

- Impact of Accounting Standards and Regulations On Financial ReportingDokument68 SeitenImpact of Accounting Standards and Regulations On Financial ReportingRicha AnandNoch keine Bewertungen

- Forecasting Financial StatementsDokument25 SeitenForecasting Financial Statementstarun slowNoch keine Bewertungen

- Module 11 Financial PlanDokument47 SeitenModule 11 Financial PlanAbdul Razak ChaqNoch keine Bewertungen

- FA - ACCA Lecture NotesDokument115 SeitenFA - ACCA Lecture NotesmosesmuomeliteNoch keine Bewertungen

- Finman ReviewerDokument17 SeitenFinman ReviewerSheila Mae Guerta LaceronaNoch keine Bewertungen

- Introduction To Accounting & Finance FinalDokument25 SeitenIntroduction To Accounting & Finance FinalManeesh Chitturu100% (1)

- Understanding of Financial Statements: What Is An Accounting?Dokument53 SeitenUnderstanding of Financial Statements: What Is An Accounting?Rashmi KhatriNoch keine Bewertungen

- CH 11Dokument13 SeitenCH 11Kashif AmmarNoch keine Bewertungen

- Financial Accts - PG1Dokument47 SeitenFinancial Accts - PG1Abhishek SinghNoch keine Bewertungen

- Gaap - Stephen J BigelowDokument4 SeitenGaap - Stephen J BigelowInnocent MundaNoch keine Bewertungen

- Comm1140 NotesDokument43 SeitenComm1140 Notesa45247788989Noch keine Bewertungen

- Conceptual Frame WorkDokument26 SeitenConceptual Frame WorkaemanNoch keine Bewertungen

- Accounting StandardsDokument26 SeitenAccounting StandardsAbhishek Chaturvedi100% (1)

- International Accounting IssuesDokument16 SeitenInternational Accounting IssueschristiananilaomarananNoch keine Bewertungen

- Lesson 4 Investment ClubDokument26 SeitenLesson 4 Investment ClubVictor VandekerckhoveNoch keine Bewertungen

- IAS 40 Investment Property PresentationDokument29 SeitenIAS 40 Investment Property PresentationNollecy Takudzwa BereNoch keine Bewertungen

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Von Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Noch keine Bewertungen

- Partnership Dissolution: National College of Business and ArtsDokument5 SeitenPartnership Dissolution: National College of Business and ArtsKate Jezel SantoniaNoch keine Bewertungen

- Solved Ballou Corporation Distributes 200 000 in Cash To Its Sharehold PDFDokument1 SeiteSolved Ballou Corporation Distributes 200 000 in Cash To Its Sharehold PDFAnbu jaromiaNoch keine Bewertungen

- TENANCY AGREEMENT Pasar SegarDokument4 SeitenTENANCY AGREEMENT Pasar SegarFade ChannelNoch keine Bewertungen

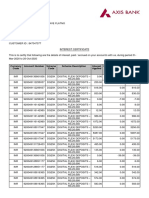

- Interest CertificateDokument2 SeitenInterest CertificatesumitNoch keine Bewertungen

- Ashoka BuildconDokument11 SeitenAshoka Buildconpritish070Noch keine Bewertungen

- Credit Union Performance - L Dean Odle 2Dokument2 SeitenCredit Union Performance - L Dean Odle 2api-413534603Noch keine Bewertungen

- 11th Com DepreciationDokument4 Seiten11th Com DepreciationObaid KhanNoch keine Bewertungen

- EXERCISESDokument25 SeitenEXERCISESGandaNoch keine Bewertungen

- Axis Bank - Final.Dokument55 SeitenAxis Bank - Final.TEJASHVINI PATELNoch keine Bewertungen

- Fundamentals of Auditing and Assurance Services OverviewDokument8 SeitenFundamentals of Auditing and Assurance Services OverviewSkye LeeNoch keine Bewertungen

- International Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Dokument20 SeitenInternational Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Chintakunta PreethiNoch keine Bewertungen

- Ch. 5 Financial AnalysisDokument34 SeitenCh. 5 Financial AnalysisfauziyahNoch keine Bewertungen

- Euro High-Yield Index Factsheet: Index, Portfolio & Risk SolutionsDokument6 SeitenEuro High-Yield Index Factsheet: Index, Portfolio & Risk SolutionsAlejandro PosadaNoch keine Bewertungen

- Rules Governing Acceptance of Fixed Deposit: Kerala Transport Development Finance Corporation LimitedDokument2 SeitenRules Governing Acceptance of Fixed Deposit: Kerala Transport Development Finance Corporation LimitedemilsonusamNoch keine Bewertungen

- Capital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Dokument2 SeitenCapital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Danzo ShahNoch keine Bewertungen

- Bond Basics: Yield, Price and Other Confusion - InvestopediaDokument7 SeitenBond Basics: Yield, Price and Other Confusion - InvestopediaLouis ForestNoch keine Bewertungen

- PGI Sample QuestionDokument4 SeitenPGI Sample QuestionleoneseNoch keine Bewertungen

- Technical Analysis in Forex TradingDokument7 SeitenTechnical Analysis in Forex TradingIFCMarketsNoch keine Bewertungen

- ch15 MCDokument26 Seitench15 MCWed CornelNoch keine Bewertungen

- 4 Hoi and RobinDokument7 Seiten4 Hoi and RobinelizabetaangelovaNoch keine Bewertungen

- Advanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part K)Dokument1 SeiteAdvanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part K)John Carlos DoringoNoch keine Bewertungen

- LAON Recovery-management-Of Andhra BankDokument87 SeitenLAON Recovery-management-Of Andhra Banklakshmikanth100% (1)

- Divine Word College of BanguedDokument3 SeitenDivine Word College of BanguedAeRis Blancaflor BalsitaNoch keine Bewertungen

- Governance, Business Ethics, Risk Management and Internal Control ReportingDokument5 SeitenGovernance, Business Ethics, Risk Management and Internal Control ReportingApril Joy ObedozaNoch keine Bewertungen

- Cement LuckyDokument13 SeitenCement LuckyAnonymous BoaSnZQvpS100% (1)

- City Limits Magazine, November 1979 IssueDokument24 SeitenCity Limits Magazine, November 1979 IssueCity Limits (New York)Noch keine Bewertungen

- Statement of AccountDokument7 SeitenStatement of AccountHamza CollectionNoch keine Bewertungen

- FINRA Series 7 Content Outline - 2015Dokument46 SeitenFINRA Series 7 Content Outline - 2015HappyGhostNoch keine Bewertungen

- Accounting For Managers Course PlanDokument3 SeitenAccounting For Managers Course PlankelifaNoch keine Bewertungen