Das könnte Ihnen auch gefallen

- CH 06Dokument65 SeitenCH 06Chang Chan Chong0% (1)

- Accounting For InventoriesDokument12 SeitenAccounting For InventoriesNoor AlSabbaghNoch keine Bewertungen

- Ch06. TranslationDokument56 SeitenCh06. TranslationNaviaNoch keine Bewertungen

- PPAcct II InventoryDokument9 SeitenPPAcct II InventoryNigussie BerhanuNoch keine Bewertungen

- Taller Cinco Acco 111Dokument41 SeitenTaller Cinco Acco 111api-274120622Noch keine Bewertungen

- Chapter 06 - InventoriesDokument57 SeitenChapter 06 - InventoriesDrake AdamNoch keine Bewertungen

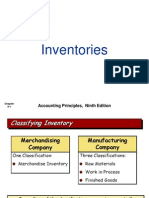

- Inventories: Accounting Principles, Ninth EditionDokument48 SeitenInventories: Accounting Principles, Ninth Editionpiash246Noch keine Bewertungen

- Determining The Monetary Amount of Inventory at Any Given Point in TimeDokument44 SeitenDetermining The Monetary Amount of Inventory at Any Given Point in TimeParth R. ShahNoch keine Bewertungen

- Welcome Back: Accounting For Business Decisions ADokument65 SeitenWelcome Back: Accounting For Business Decisions ALeah StonesNoch keine Bewertungen

- Inventory Valuation GuideDokument43 SeitenInventory Valuation GuideQuyen Thanh NguyenNoch keine Bewertungen

- Chapter - 1 Inventories Definition: - Inventory Is Used To DesignateDokument14 SeitenChapter - 1 Inventories Definition: - Inventory Is Used To DesignateMulugeta TsegaNoch keine Bewertungen

- IMPACT OF INVENTORY VALUATIONDokument10 SeitenIMPACT OF INVENTORY VALUATIONneten_dkjNoch keine Bewertungen

- Act512 - Assignment Chapter - 06Dokument9 SeitenAct512 - Assignment Chapter - 06Rafin MahmudNoch keine Bewertungen

- 2010-06-23 203304 Financialaccounting 2Dokument6 Seiten2010-06-23 203304 Financialaccounting 2pi!Noch keine Bewertungen

- Accounting Principles 7Th Canadian Edition Volume 1 by Jerry J. Weygandt, Test BankDokument95 SeitenAccounting Principles 7Th Canadian Edition Volume 1 by Jerry J. Weygandt, Test BankakasagillNoch keine Bewertungen

- Libby Financial Accounting Chapter7Dokument10 SeitenLibby Financial Accounting Chapter7Jie Bo Ti0% (2)

- CHAPTER Four NewDokument16 SeitenCHAPTER Four NewHace AdisNoch keine Bewertungen

- Chapter 1 Accounting For InventoryDokument12 SeitenChapter 1 Accounting For InventoryLee HailuNoch keine Bewertungen

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDokument66 SeitenPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegenaeemakhtaracmaNoch keine Bewertungen

- Final Chapter 6Dokument8 SeitenFinal Chapter 6Đặng Ngọc Thu HiềnNoch keine Bewertungen

- Text5-Accounting For Materials-Student ResourceDokument10 SeitenText5-Accounting For Materials-Student Resourcekinai williamNoch keine Bewertungen

- Inventory and Cost of Goods SoldDokument39 SeitenInventory and Cost of Goods SoldIsabell Camillo75% (4)

- Taller Seis Acco 111Dokument44 SeitenTaller Seis Acco 111api-274120622Noch keine Bewertungen

- Financial Accounting Practice and Review InventoryDokument3 SeitenFinancial Accounting Practice and Review Inventoryukandi rukmanaNoch keine Bewertungen

- Tutoring Session 3Dokument2 SeitenTutoring Session 3Murtaza HussainNoch keine Bewertungen

- POA1-Assignment - Chapter 6 - Q SentDokument6 SeitenPOA1-Assignment - Chapter 6 - Q SentYusniagita EkadityaNoch keine Bewertungen

- InventoryDokument12 SeitenInventoryMesele AdemeNoch keine Bewertungen

- intermidet ch4Dokument90 Seitenintermidet ch4kqk07829Noch keine Bewertungen

- Methods InventoryDokument12 SeitenMethods InventoryJocelyn LimaNoch keine Bewertungen

- What Is Asset V-WPS OfficeDokument15 SeitenWhat Is Asset V-WPS OfficeGift EdigbeNoch keine Bewertungen

- P2 - New Ch2Dokument10 SeitenP2 - New Ch2mulugetaNoch keine Bewertungen

- Inventories: Purchaser SellerDokument23 SeitenInventories: Purchaser SellerBrylle TamanoNoch keine Bewertungen

- HWChap 006Dokument67 SeitenHWChap 006hellooceanNoch keine Bewertungen

- Libby 4ce Solutions Manual - Ch08Dokument66 SeitenLibby 4ce Solutions Manual - Ch087595522Noch keine Bewertungen

- INVENTORY VALUATIONDokument13 SeitenINVENTORY VALUATIONSumit SahuNoch keine Bewertungen

- ACCT 201: Reporting and Analyzing InventoryDokument22 SeitenACCT 201: Reporting and Analyzing InventoryDuygu YılmazNoch keine Bewertungen

- Kelompok 6 Chapter 6Dokument11 SeitenKelompok 6 Chapter 6leoni pannaNoch keine Bewertungen

- Track Merchandise Inventory CostsDokument18 SeitenTrack Merchandise Inventory CostsawlachewNoch keine Bewertungen

- Inventory: Key Topics To KnowDokument9 SeitenInventory: Key Topics To KnowYaregal YeshiwasNoch keine Bewertungen

- Chapter 6 PowerpointDokument34 SeitenChapter 6 Powerpointapi-248607804Noch keine Bewertungen

- Unit 1 InvetoryDokument53 SeitenUnit 1 InvetoryHirut GetachewNoch keine Bewertungen

- FINANCIAL ACCOUNTING 2020-2021 - MODULE 4 - RevisedDokument26 SeitenFINANCIAL ACCOUNTING 2020-2021 - MODULE 4 - RevisedAnn CalabdanNoch keine Bewertungen

- Fundamentals of Accounting II, Chapter 1Dokument51 SeitenFundamentals of Accounting II, Chapter 1negussie birieNoch keine Bewertungen

- Chapter 1, InventoriesDokument18 SeitenChapter 1, InventoriesAmsaluNoch keine Bewertungen

- ACC 103 CH 5 Lecture Part1Dokument11 SeitenACC 103 CH 5 Lecture Part1Muhammad Farhan AliNoch keine Bewertungen

- Chap 008Dokument69 SeitenChap 008dbjnNoch keine Bewertungen

- Fundamentals of Financial Accounting Canadian 5th Edition Phillips Solutions ManualDokument38 SeitenFundamentals of Financial Accounting Canadian 5th Edition Phillips Solutions Manualjeanbarnettxv9v100% (16)

- 06 InventoriesDokument3 Seiten06 InventoriesCy MiolataNoch keine Bewertungen

- Module 4 Inventory and Biological AssetsDokument19 SeitenModule 4 Inventory and Biological AssetsAndrea Miles VasquezNoch keine Bewertungen

- Chapter 7 Supply ChainDokument15 SeitenChapter 7 Supply Chainrahulg2710Noch keine Bewertungen

- Accounting for Inventory CostsDokument16 SeitenAccounting for Inventory CostsLemma Deme ResearcherNoch keine Bewertungen

- Transcript For Lecture Video 1Dokument5 SeitenTranscript For Lecture Video 1StaygoldNoch keine Bewertungen

- Fifo MethodDokument36 SeitenFifo Methodabhisheksachan10Noch keine Bewertungen

- Maintain Inventory RecordsDokument16 SeitenMaintain Inventory Recordsjoy xoNoch keine Bewertungen

- 08 Inventory Cost MeasurementDokument34 Seiten08 Inventory Cost MeasurementLeonilaEnriquezNoch keine Bewertungen

- Accounting for Goodwill and Other Intangible AssetsVon EverandAccounting for Goodwill and Other Intangible AssetsBewertung: 4 von 5 Sternen4/5 (1)

- Understanding Financial Statements (Review and Analysis of Straub's Book)Von EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Bewertung: 5 von 5 Sternen5/5 (5)

- Accounting All-in-One For Dummies, with Online PracticeVon EverandAccounting All-in-One For Dummies, with Online PracticeBewertung: 3 von 5 Sternen3/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsVon EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsBewertung: 5 von 5 Sternen5/5 (1)

- 4-6-2016 - Nike, SociDokument20 Seiten4-6-2016 - Nike, SociSet LuNoch keine Bewertungen

- Usd Macro Problem Set 1Dokument7 SeitenUsd Macro Problem Set 1Set Lu100% (2)

- ECON 216 - Statistics For Business and Economics: Andrew NarwoldDokument12 SeitenECON 216 - Statistics For Business and Economics: Andrew NarwoldSet LuNoch keine Bewertungen

- Bible CharactersDokument3 SeitenBible CharactersSet LuNoch keine Bewertungen

- Referral PolicyDokument2 SeitenReferral PolicyDipikaNoch keine Bewertungen

- SEDA (Application Form) Manual 425kWp Up To 1MW - 140514Dokument13 SeitenSEDA (Application Form) Manual 425kWp Up To 1MW - 140514raghuram86Noch keine Bewertungen

- Taxation Law I 2020Dokument148 SeitenTaxation Law I 2020Japoy Regodon EsquilloNoch keine Bewertungen

- Risk and Rates of Return: Multiple Choice: ConceptualDokument79 SeitenRisk and Rates of Return: Multiple Choice: ConceptualKatherine Cabading InocandoNoch keine Bewertungen

- Spouses Aggabao V. Parulan, Jr. and Parulan G.R. No. 165803, (September 1, 2010) Doctrine (S)Dokument9 SeitenSpouses Aggabao V. Parulan, Jr. and Parulan G.R. No. 165803, (September 1, 2010) Doctrine (S)RJNoch keine Bewertungen

- Earnings Management in India: Managers' Fixation On Operating ProfitsDokument27 SeitenEarnings Management in India: Managers' Fixation On Operating ProfitsVaibhav KaushikNoch keine Bewertungen

- BonanzaDokument2 SeitenBonanzaMaster HusainNoch keine Bewertungen

- Truth in Lending Act Requires Disclosure of Finance ChargesDokument3 SeitenTruth in Lending Act Requires Disclosure of Finance Chargesjeffprox69Noch keine Bewertungen

- NMIMS MUMBAI NAVI MUMBAI Student Activity Sponsorship and Exp - POLICYDokument5 SeitenNMIMS MUMBAI NAVI MUMBAI Student Activity Sponsorship and Exp - POLICYRushil ShahNoch keine Bewertungen

- 07R911036CDokument899 Seiten07R911036Cbreanna4teen9949Noch keine Bewertungen

- Teaching Market Making with a Game SimulationDokument4 SeitenTeaching Market Making with a Game SimulationRamkrishna LanjewarNoch keine Bewertungen

- Certificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Dokument32 SeitenCertificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Sakura AvhrynNoch keine Bewertungen

- Vajiram & Ravi Civil Services Exam Details for Sept 2022-23Dokument3 SeitenVajiram & Ravi Civil Services Exam Details for Sept 2022-23Appu MansaNoch keine Bewertungen

- FS FactoringDokument17 SeitenFS FactoringJai DeepNoch keine Bewertungen

- GPPB Reso 27-2012Dokument3 SeitenGPPB Reso 27-2012Ax Scribd100% (1)

- 41 and 42 Tolentino Vs Secretary of FinanceDokument2 Seiten41 and 42 Tolentino Vs Secretary of FinanceYvon Baguio100% (1)

- Joint Venture in Insurance Company in IndiaDokument37 SeitenJoint Venture in Insurance Company in IndiaSEMNoch keine Bewertungen

- A122 Exercises QDokument30 SeitenA122 Exercises QBryan Jackson100% (1)

- Statement of Comprehensive Income Worksheet 1 SampleDokument6 SeitenStatement of Comprehensive Income Worksheet 1 SampleKim Shyen BontuyanNoch keine Bewertungen

- Sebi Grade A Exam: Paper 2 Questions With SolutionsDokument34 SeitenSebi Grade A Exam: Paper 2 Questions With SolutionsnitinNoch keine Bewertungen

- Corporate Finance Problem Set 5Dokument2 SeitenCorporate Finance Problem Set 5MANoch keine Bewertungen

- Notes To FS - Part 1Dokument24 SeitenNotes To FS - Part 1Precious Jireh100% (1)

- Securitization of Financial AssetsDokument7 SeitenSecuritization of Financial Assetsnaglaa alyNoch keine Bewertungen

- Total For Reimbursements: Transportation Reimbursements Date Transpo To BITSI March 23 To May 5, 2022Dokument4 SeitenTotal For Reimbursements: Transportation Reimbursements Date Transpo To BITSI March 23 To May 5, 2022IANNoch keine Bewertungen

- Brief of DETAILS of Direct Selling and Plan PDFDokument7 SeitenBrief of DETAILS of Direct Selling and Plan PDFRoNu Rohini ChauhanNoch keine Bewertungen

- Saral Gyan Stocks Past Performance 050113Dokument13 SeitenSaral Gyan Stocks Past Performance 050113saptarshidas21Noch keine Bewertungen

- Scotia Aria Progressive Defend Portfolio - Premium Series: Global Equity BalancedDokument2 SeitenScotia Aria Progressive Defend Portfolio - Premium Series: Global Equity BalancedChrisNoch keine Bewertungen

- Non-current Liabilities - Bonds Payable Classification and MeasurementDokument4 SeitenNon-current Liabilities - Bonds Payable Classification and MeasurementhIgh QuaLIty SVTNoch keine Bewertungen

- 1st PB-TADokument12 Seiten1st PB-TAGlenn Patrick de LeonNoch keine Bewertungen