Das könnte Ihnen auch gefallen

- Audit Engagement Letter UNAI2022Dokument5 SeitenAudit Engagement Letter UNAI2022Vienzo SiagianNoch keine Bewertungen

- LN02Titman 449327 12 LN02Dokument48 SeitenLN02Titman 449327 12 LN02Nasrudin Insaf Bin Jaafarali100% (1)

- Tardiness Reso of CSCDokument5 SeitenTardiness Reso of CSCxed serNoch keine Bewertungen

- AFS Module 1 Part 1Dokument67 SeitenAFS Module 1 Part 1Helen Grace Benjamin100% (1)

- Pcab Forms 2015Dokument25 SeitenPcab Forms 2015Helen Cinense89% (9)

- PH Budget Circular outlines overtime pay rulesDokument4 SeitenPH Budget Circular outlines overtime pay rulesacir_05Noch keine Bewertungen

- Barangay - Acctg. System - Edited.emrDokument104 SeitenBarangay - Acctg. System - Edited.emrAnnamaAnnama100% (2)

- Module 3 - Assessment CalendarDokument12 SeitenModule 3 - Assessment CalendarElmar Perez Blanco100% (1)

- Accounting For LgusDokument47 SeitenAccounting For LgusPatricia Reyes100% (1)

- Lgsf-Fa To Lgus LBC No. 119Dokument58 SeitenLgsf-Fa To Lgus LBC No. 119ALPINE SUNSHINE A. CHIWERANNoch keine Bewertungen

- Manual DohDokument276 SeitenManual DohdinvNoch keine Bewertungen

- MOOg 45-64Dokument72 SeitenMOOg 45-64Zeniah Arizo100% (1)

- District Presentation - Info Kit - 2016smv1103Dokument58 SeitenDistrict Presentation - Info Kit - 2016smv1103Jonesa Marie100% (1)

- Cawad VS Abad Et Al, GR 207145, Juky 28, 2015Dokument27 SeitenCawad VS Abad Et Al, GR 207145, Juky 28, 2015GmaeNoch keine Bewertungen

- Undergraduate Scholarship RubricDokument1 SeiteUndergraduate Scholarship Rubricapi-243234232Noch keine Bewertungen

- Lbac Form 2021Dokument14 SeitenLbac Form 2021Zyreen Kate CataquisNoch keine Bewertungen

- Updates On Taxation For Cooperative PDFDokument69 SeitenUpdates On Taxation For Cooperative PDFkatrina engoNoch keine Bewertungen

- Independent: Auditor'S ReportDokument3 SeitenIndependent: Auditor'S ReportRene Huyo-aNoch keine Bewertungen

- Journal Entry Voucher: Municipal Government of Lambunao Disbursement VoucherDokument12 SeitenJournal Entry Voucher: Municipal Government of Lambunao Disbursement VoucherFrancisco Lubas Santillana IVNoch keine Bewertungen

- Revised Rules On ReassignmentDokument2 SeitenRevised Rules On ReassignmentAmapola BulusanNoch keine Bewertungen

- COA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsDokument6 SeitenCOA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsJonson PalmaresNoch keine Bewertungen

- Government Auditing and Accounting For NPODokument65 SeitenGovernment Auditing and Accounting For NPOAljon Fabrigas SalacNoch keine Bewertungen

- Capital BudgetingDokument15 SeitenCapital BudgetingJoshua Naragdag ColladoNoch keine Bewertungen

- Bir-Cda Joint Rules and Regulations Back UpDokument60 SeitenBir-Cda Joint Rules and Regulations Back UpGlenn S. GarciaNoch keine Bewertungen

- Bir Cda Joint Rules and RegulationsDokument12 SeitenBir Cda Joint Rules and RegulationsCha Ancheta CabigasNoch keine Bewertungen

- A Guide For City Mayors A Guide For City MayorsDokument56 SeitenA Guide For City Mayors A Guide For City MayorsElaNoch keine Bewertungen

- Personnel ManualDokument65 SeitenPersonnel ManualJessica GalindoNoch keine Bewertungen

- 1-Connecting Plans To The BudgetDokument81 Seiten1-Connecting Plans To The BudgetJamy Vab MontesNoch keine Bewertungen

- Steps in Transfer of TitleDokument2 SeitenSteps in Transfer of TitleApril Joy Ortilano- CajiloNoch keine Bewertungen

- Lending Company Regulation Act of 2007Dokument1 SeiteLending Company Regulation Act of 2007jade123_129Noch keine Bewertungen

- RA 9520 IRR Certain ProvisionsDokument22 SeitenRA 9520 IRR Certain Provisionsroy rubaNoch keine Bewertungen

- JCI Philippines Awards Manual 2014Dokument51 SeitenJCI Philippines Awards Manual 2014mariangpalad69Noch keine Bewertungen

- PPSAS Report For PowerpointDokument6 SeitenPPSAS Report For PowerpointButchoy GemaoNoch keine Bewertungen

- CPDD-ACC-01-A Application Form As Local CPD Provider 2020Dokument2 SeitenCPDD-ACC-01-A Application Form As Local CPD Provider 2020Elie DGNoch keine Bewertungen

- APSEMO A Guide For City MayorsDokument68 SeitenAPSEMO A Guide For City MayorspdccNoch keine Bewertungen

- Affidavit of Non-Operation2Dokument1 SeiteAffidavit of Non-Operation2Mayett Manalo MendozaNoch keine Bewertungen

- CIAP Citizen's Charter outlines services for construction industryDokument254 SeitenCIAP Citizen's Charter outlines services for construction industryAffordable HousingNoch keine Bewertungen

- Features of the Government Accounting ManualDokument30 SeitenFeatures of the Government Accounting ManualMay Joy ManagdagNoch keine Bewertungen

- LOCAL BUDGET PROCESSDokument12 SeitenLOCAL BUDGET PROCESSAigene PinedaNoch keine Bewertungen

- Linking The Plan To The BudgetDokument14 SeitenLinking The Plan To The Budgetrohaida musaNoch keine Bewertungen

- Boa Sworn Statement For AccreditationDokument1 SeiteBoa Sworn Statement For AccreditationBillcounterNoch keine Bewertungen

- Ecology Planning Devt ZoningDokument94 SeitenEcology Planning Devt ZoningNILO PAJARELLANONoch keine Bewertungen

- GROUP 5 HUMAY Multi Purpose CooperativeDokument34 SeitenGROUP 5 HUMAY Multi Purpose CooperativeIcah Mae D. SaloNoch keine Bewertungen

- 04 07 17 - Petron - Annual Report 2016 (SEC Form 17-A) (As Filed With SEC On April 6, 2017) .Dokument228 Seiten04 07 17 - Petron - Annual Report 2016 (SEC Form 17-A) (As Filed With SEC On April 6, 2017) .Lara Flynne Castro-Gregorio100% (1)

- TRANSFER LAND OWNERSHIPDokument5 SeitenTRANSFER LAND OWNERSHIPCrisanta MarieNoch keine Bewertungen

- The Local Government CodeDokument176 SeitenThe Local Government CodeGracelyn Enriquez BellinganNoch keine Bewertungen

- Engagement LetterDokument2 SeitenEngagement LetterNelnel GarciaNoch keine Bewertungen

- BIR's Tax Ruling Process ExplainedDokument3 SeitenBIR's Tax Ruling Process ExplainedConnieAllanaMacapagaoNoch keine Bewertungen

- BIR Ease of Doing BusinessDokument25 SeitenBIR Ease of Doing BusinessCess MelendezNoch keine Bewertungen

- Tax Agents and PractitionersDokument5 SeitenTax Agents and PractitionerskawaiimiracleNoch keine Bewertungen

- Real Property TaxationDokument39 SeitenReal Property Taxationmarjorie blanco100% (1)

- 0087 - Digital Tax Parcel Mapping - Example 1 - iTAX Mapping in The PhilippinesDokument21 Seiten0087 - Digital Tax Parcel Mapping - Example 1 - iTAX Mapping in The PhilippinesCACNoch keine Bewertungen

- SMR - FSDokument1 SeiteSMR - FSBaldovino VenturesNoch keine Bewertungen

- Invalidating Tax Assessment January 2024 2Dokument68 SeitenInvalidating Tax Assessment January 2024 2arnulfojr hicoNoch keine Bewertungen

- Preparation of Financial Statements 081112 RevisedDokument89 SeitenPreparation of Financial Statements 081112 RevisedNorhian AlmeronNoch keine Bewertungen

- Fleet Management System A Complete Guide - 2021 EditionVon EverandFleet Management System A Complete Guide - 2021 EditionNoch keine Bewertungen

- COA adjudication process guideDokument41 SeitenCOA adjudication process guideJulie Khristine Panganiban-ArevaloNoch keine Bewertungen

- Tax Admin and EnforcementDokument5 SeitenTax Admin and EnforcementPeanutButter 'n JellyNoch keine Bewertungen

- Taxation - 8 Tax Remedies Under NIRCDokument34 SeitenTaxation - 8 Tax Remedies Under NIRCcmv mendoza100% (3)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Von EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Noch keine Bewertungen

- 12b Template - Slides 16-9Dokument8 Seiten12b Template - Slides 16-9Abi Serrano TaguiamNoch keine Bewertungen

- NpoDokument30 SeitenNpoAbi Serrano TaguiamNoch keine Bewertungen

- 12a Template - Slides 4-3Dokument8 Seiten12a Template - Slides 4-3Abi Serrano TaguiamNoch keine Bewertungen

- Style: A Medical Plan For The Young MarketDokument4 SeitenStyle: A Medical Plan For The Young MarketAbi Serrano TaguiamNoch keine Bewertungen

- SLAMCI App Form 2013 v4 - 04.07.14Dokument4 SeitenSLAMCI App Form 2013 v4 - 04.07.14impuissantNoch keine Bewertungen

- LoyaltyCard 2016 May4Dokument14 SeitenLoyaltyCard 2016 May4Abi Serrano TaguiamNoch keine Bewertungen

- BCDokument73 SeitenBCAbi Serrano Taguiam100% (2)

- Select 2015-01 (Jan) LowresDokument6 SeitenSelect 2015-01 (Jan) LowresAbi Serrano TaguiamNoch keine Bewertungen

- NBC548 PDFDokument9 SeitenNBC548 PDFegabadNoch keine Bewertungen

- CPA Review: Code of Ethics for Professional Accountants in the PhilippinesDokument20 SeitenCPA Review: Code of Ethics for Professional Accountants in the PhilippinesJedidiah SmithNoch keine Bewertungen

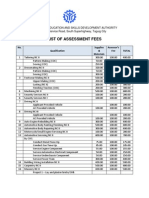

- List of Assessment FeesDokument6 SeitenList of Assessment FeesBenjo FransiscoNoch keine Bewertungen

- NFPDokument53 SeitenNFPYane Purazo - Duque100% (1)

- Revised Withholding Tax TablesDokument1 SeiteRevised Withholding Tax TablesJonasAblangNoch keine Bewertungen

- Premier Brochure 2013-07 (July) P2015!03!4pDokument4 SeitenPremier Brochure 2013-07 (July) P2015!03!4pAbi Serrano TaguiamNoch keine Bewertungen

- Summary IFRS For SMEDokument17 SeitenSummary IFRS For SMEAbi Serrano Taguiam100% (1)

- Summary IFRS For SMEDokument17 SeitenSummary IFRS For SMEAbi Serrano Taguiam100% (1)

- Philippine Bidding Documents for Procurement of GoodsDokument94 SeitenPhilippine Bidding Documents for Procurement of GoodsSittie Farhana BaltNoch keine Bewertungen

- Revised Rules On Administrative Cases in The Civil ServiceDokument43 SeitenRevised Rules On Administrative Cases in The Civil ServiceMerlie Moga100% (29)

- Case Digest 11-20Dokument9 SeitenCase Digest 11-20Abi Serrano TaguiamNoch keine Bewertungen

- The PPSAS and The Revised Chart of AccountsDokument98 SeitenThe PPSAS and The Revised Chart of AccountsDaniel Salmorin87% (15)

- Government Employee ViolationsDokument6 SeitenGovernment Employee ViolationsBernice Purugganan AresNoch keine Bewertungen

- Maestro Vs CADokument4 SeitenMaestro Vs CAAbi Serrano TaguiamNoch keine Bewertungen

- Oria Vs McMickingDokument4 SeitenOria Vs McMickingAbi Serrano TaguiamNoch keine Bewertungen

- Value For Money AuditDokument86 SeitenValue For Money AuditAbi Serrano TaguiamNoch keine Bewertungen

- 1987 ConstitutionDokument67 Seiten1987 ConstitutionAbi Serrano TaguiamNoch keine Bewertungen

- 36 Mortel vs. KASSCO IncDokument4 Seiten36 Mortel vs. KASSCO IncAbi Serrano TaguiamNoch keine Bewertungen

- Maestro Vs CADokument4 SeitenMaestro Vs CAAbi Serrano TaguiamNoch keine Bewertungen

- American Fashion Vs Office of The PresidentDokument8 SeitenAmerican Fashion Vs Office of The PresidentAbi Serrano TaguiamNoch keine Bewertungen

- Law and Logic (Fallacies)Dokument10 SeitenLaw and Logic (Fallacies)Arbie Dela TorreNoch keine Bewertungen

- Rodriguez-Luna vs. Intermediate Appellate CourtDokument7 SeitenRodriguez-Luna vs. Intermediate Appellate Courtvince005Noch keine Bewertungen

- Swatanter Kumar Vs The Indian Express Ltd. & Ors - Delhi High Court OrdersDokument47 SeitenSwatanter Kumar Vs The Indian Express Ltd. & Ors - Delhi High Court Ordersdharma nextNoch keine Bewertungen

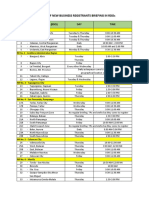

- Schedule of New Business Registrants Briefings by Revenue District OfficeDokument4 SeitenSchedule of New Business Registrants Briefings by Revenue District OfficeNarkSunderNoch keine Bewertungen

- Mark - Non Registrable Industrial DesignDokument13 SeitenMark - Non Registrable Industrial DesignHannah Keziah Dela CernaNoch keine Bewertungen

- Loan AgreementDokument2 SeitenLoan AgreementElizabeth Fernandez-BenologaNoch keine Bewertungen

- Kanun - WikiDokument6 SeitenKanun - WikiPhilip SuitorNoch keine Bewertungen

- SPA TO PROCESS (Loss OR CR)Dokument1 SeiteSPA TO PROCESS (Loss OR CR)majoy75% (4)

- Villahermosa Sr. v. CaracolDokument6 SeitenVillahermosa Sr. v. CaracolVener Angelo MargalloNoch keine Bewertungen

- 2-National Differences in JGKHJ J'L K'pkjkjlpolitical EconomyDokument14 Seiten2-National Differences in JGKHJ J'L K'pkjkjlpolitical EconomyDiana HanyNoch keine Bewertungen

- Project BaschetDokument10 SeitenProject BaschetDobler LilianaNoch keine Bewertungen

- Utulo V PasionDokument1 SeiteUtulo V PasionElaizza ConcepcionNoch keine Bewertungen

- TK8A50D Field Effect Transistor SpecificationsDokument6 SeitenTK8A50D Field Effect Transistor Specifications劉毛毛Noch keine Bewertungen

- E4A Circus - Report Digital OK v2Dokument27 SeitenE4A Circus - Report Digital OK v2gvggbgbgNoch keine Bewertungen

- Memoramdum of AgreementDokument2 SeitenMemoramdum of Agreementvayne bangayanNoch keine Bewertungen

- Esmalin Vs NLRC & Care Phil.Dokument8 SeitenEsmalin Vs NLRC & Care Phil.Monroe P ZosaNoch keine Bewertungen

- License All Reports Brookings InstituteDokument134 SeitenLicense All Reports Brookings InstitutePA Work LicenseNoch keine Bewertungen

- Medical Components v. C.R. BardDokument14 SeitenMedical Components v. C.R. BardPriorSmartNoch keine Bewertungen

- The Right To Privacy in The Philippines: Stakeholder Report Universal Periodic Review 27 Session - PhilippinesDokument11 SeitenThe Right To Privacy in The Philippines: Stakeholder Report Universal Periodic Review 27 Session - PhilippinesJan. ReyNoch keine Bewertungen

- Gajendra Singh Yadav Vs Union of IndiaDokument3 SeitenGajendra Singh Yadav Vs Union of IndiaShreya SinhaNoch keine Bewertungen

- York County Court Schedule For April 17Dokument17 SeitenYork County Court Schedule For April 17York Daily Record/Sunday NewsNoch keine Bewertungen

- PDFDokument9 SeitenPDFCBS12NewsReportsNoch keine Bewertungen

- Record Keeping and Pay Slips PDFDokument6 SeitenRecord Keeping and Pay Slips PDFYi YauNoch keine Bewertungen

- Coercion in Contract LawDokument17 SeitenCoercion in Contract LawBba ANoch keine Bewertungen

- Report of Chapter 3 - Redfern and HunterDokument9 SeitenReport of Chapter 3 - Redfern and HunterLucas Vasconcelos de LimaNoch keine Bewertungen

- Pineda-Ng Vs PeopleDokument1 SeitePineda-Ng Vs PeopleJudy Miraflores DumdumaNoch keine Bewertungen

- Roque Vs LapuzDokument2 SeitenRoque Vs LapuzJames Evan I. ObnamiaNoch keine Bewertungen

- Case Digest: Imbong vs. Ochoa, JR PDFDokument14 SeitenCase Digest: Imbong vs. Ochoa, JR PDFJetJuárezNoch keine Bewertungen

- TdsDokument4 SeitenTdsshanikaNoch keine Bewertungen

- Dwelly Cauley v. United States, 11th Cir. (2010)Dokument5 SeitenDwelly Cauley v. United States, 11th Cir. (2010)Scribd Government DocsNoch keine Bewertungen

- Roy Charles Rundle and Mrs. Evelyn Rundle v. Grubb Motor Lines, Inc., and Dwaine Murel Moser, 300 F.2d 333, 4th Cir. (1962)Dokument9 SeitenRoy Charles Rundle and Mrs. Evelyn Rundle v. Grubb Motor Lines, Inc., and Dwaine Murel Moser, 300 F.2d 333, 4th Cir. (1962)Scribd Government DocsNoch keine Bewertungen