Das könnte Ihnen auch gefallen

- Real Estate Valuation)Dokument40 SeitenReal Estate Valuation)shivpreetsandhuNoch keine Bewertungen

- ISMSDokument23 SeitenISMSshivpreetsandhu100% (1)

- NOC and SOCDokument19 SeitenNOC and SOCshivpreetsandhuNoch keine Bewertungen

- Information Technology InfrastructureDokument29 SeitenInformation Technology InfrastructureshivpreetsandhuNoch keine Bewertungen

- Slum Rehablitiaion ReportDokument65 SeitenSlum Rehablitiaion Reportshivpreetsandhu100% (2)

- Legal Tech and Digital Transformation: Competitive Positioning and Business Models of Law FirmsVon EverandLegal Tech and Digital Transformation: Competitive Positioning and Business Models of Law FirmsNoch keine Bewertungen

- Strategic Outsourcing at Bharti Airtel LimitedDokument6 SeitenStrategic Outsourcing at Bharti Airtel LimitedAnna Marie Mccurdy FitzgeraldNoch keine Bewertungen

- Sustaining Contractual Business: an Exploration of the New Revised International Commercial Terms: Incoterms®2010Von EverandSustaining Contractual Business: an Exploration of the New Revised International Commercial Terms: Incoterms®2010Noch keine Bewertungen

- Slum Rehabilitation Schemes: 33.10 SchemeDokument5 SeitenSlum Rehabilitation Schemes: 33.10 Schemeshivpreetsandhu100% (1)

- Comparative Analysis of Marketing Strategies of VODAFONE and AIRTELDokument62 SeitenComparative Analysis of Marketing Strategies of VODAFONE and AIRTELAbhay JainNoch keine Bewertungen

- Marketing Strategies Comparison of Vodafone and AirtelDokument78 SeitenMarketing Strategies Comparison of Vodafone and AirtelSami ZamaNoch keine Bewertungen

- Consumer Behaviour of Airtel NewDokument72 SeitenConsumer Behaviour of Airtel NewArpit BaggaNoch keine Bewertungen

- Airtel ChangedDokument107 SeitenAirtel ChangedRahulNaiyyarNoch keine Bewertungen

- Bharti Airtel AND MTN - The Unsuccessful Deal By: Beerkaran YaminiDokument23 SeitenBharti Airtel AND MTN - The Unsuccessful Deal By: Beerkaran YaminiBk SidhuNoch keine Bewertungen

- Mergers and Acquisitions in Indian Telecom SectorDokument15 SeitenMergers and Acquisitions in Indian Telecom SectorVinal PatilNoch keine Bewertungen

- Project AirtelDokument79 SeitenProject AirtelshashankNoch keine Bewertungen

- A Term Project On GSCMDokument33 SeitenA Term Project On GSCMIndrajit Indrani BanerjeeNoch keine Bewertungen

- Impact of AGR Ruling on Telecom SectorDokument4 SeitenImpact of AGR Ruling on Telecom SectorRamreejhan ChaudharyNoch keine Bewertungen

- Technology, Media & TelecommunicationsDokument4 SeitenTechnology, Media & TelecommunicationsAaryan LakhaniNoch keine Bewertungen

- Bharti 2airtel 1227851581611151 8Dokument48 SeitenBharti 2airtel 1227851581611151 8Venkat NatarajanNoch keine Bewertungen

- CP Osp 29032019Dokument56 SeitenCP Osp 29032019PratikNoch keine Bewertungen

- Telecom Industry Woes and SolutionsDokument4 SeitenTelecom Industry Woes and SolutionsMohd AnasNoch keine Bewertungen

- PTCL - Market Structure and Regression AnalysisDokument21 SeitenPTCL - Market Structure and Regression AnalysisSanya Tiwana100% (1)

- ME - Telecom Industry CostDokument9 SeitenME - Telecom Industry Costsharad_bajajNoch keine Bewertungen

- Airtel Project PDFDokument50 SeitenAirtel Project PDFhika50% (2)

- Customer Relationship Management and Service Quality at Idea CellularDokument89 SeitenCustomer Relationship Management and Service Quality at Idea CellularShekhar_Kapoor_11210% (1)

- AT&T GNSI Counter Comments TRAI M2M ConsultationDokument12 SeitenAT&T GNSI Counter Comments TRAI M2M ConsultationSushil BabooNoch keine Bewertungen

- C.I Retail Management 111Dokument25 SeitenC.I Retail Management 111JeyaprakanthNoch keine Bewertungen

- Telecom in IndiaDokument59 SeitenTelecom in IndiaAnkur Singh NegiNoch keine Bewertungen

- Project On Voda and AirtelDokument81 SeitenProject On Voda and AirtelNitu SainiNoch keine Bewertungen

- Report 4Dokument13 SeitenReport 4Pushkar AgarwalNoch keine Bewertungen

- Bandwidth Pricing and Its EconomicsDokument20 SeitenBandwidth Pricing and Its EconomicsGarvit SharmaNoch keine Bewertungen

- CAN THE TELECOM INDUSTRY WELCOME THE NEW ENTRANTSDokument8 SeitenCAN THE TELECOM INDUSTRY WELCOME THE NEW ENTRANTSPijush Kanti DolaiNoch keine Bewertungen

- I C ' A S T: R. SrinivasanDokument26 SeitenI C ' A S T: R. SrinivasanvirenNoch keine Bewertungen

- M&A Group AssignmentDokument25 SeitenM&A Group AssignmentPratik MalviyaNoch keine Bewertungen

- Blue Diamond Group 10Dokument33 SeitenBlue Diamond Group 10guptak09Noch keine Bewertungen

- Project Report: "Consumer Behaviour of Airtel"Dokument95 SeitenProject Report: "Consumer Behaviour of Airtel"Sudhakar KarkeraNoch keine Bewertungen

- Economics - Telecom Industry - Government PoliciesDokument3 SeitenEconomics - Telecom Industry - Government PoliciesPraveenNoch keine Bewertungen

- Telecom Industry in IndiaDokument21 SeitenTelecom Industry in IndiaVaibhav PatelNoch keine Bewertungen

- Indias Telecom SectorDokument14 SeitenIndias Telecom Sectoramitdce0178Noch keine Bewertungen

- Airtel Consumer Behavior ReportDokument87 SeitenAirtel Consumer Behavior ReportShubham VermaNoch keine Bewertungen

- Bharti LTDDokument16 SeitenBharti LTDkpooran389Noch keine Bewertungen

- Project On Bharti Airtel LTDDokument24 SeitenProject On Bharti Airtel LTDMahendra ChoubeyNoch keine Bewertungen

- A Project Report On: Master of Business AdministrationDokument45 SeitenA Project Report On: Master of Business AdministrationMd IntekhabNoch keine Bewertungen

- Jio Case Study PDFDokument4 SeitenJio Case Study PDFmanindersingh949100% (1)

- Bharti Zain Ppt-FinalDokument17 SeitenBharti Zain Ppt-FinalMehul J Sudra50% (2)

- Bav Assignment TelecomDokument36 SeitenBav Assignment Telecomudit singhNoch keine Bewertungen

- India: M&A Landscape: Featuring Vineet AnejaDokument20 SeitenIndia: M&A Landscape: Featuring Vineet Anejajayth123Noch keine Bewertungen

- 2G Anatomy of The Scam: Triumphant Institute of Management Education P LTDDokument56 Seiten2G Anatomy of The Scam: Triumphant Institute of Management Education P LTDAbhay YadavNoch keine Bewertungen

- Reforms in The Indian Telecom Industry ReportDokument13 SeitenReforms in The Indian Telecom Industry ReportAnakha RadhakrishnanNoch keine Bewertungen

- Telecom Tower Provider: Group - 8Dokument16 SeitenTelecom Tower Provider: Group - 8Megha AgrawalNoch keine Bewertungen

- Airtel - C.I For RetailDokument25 SeitenAirtel - C.I For RetailJeyaprakanthNoch keine Bewertungen

- Telecom Sector in IndiaDokument15 SeitenTelecom Sector in IndiapawanchetanaNoch keine Bewertungen

- Telecom Sector in IndiaDokument15 SeitenTelecom Sector in IndiajuzarboxwalaNoch keine Bewertungen

- Telecom Sector in IndiaDokument15 SeitenTelecom Sector in IndiaLakshmanRao NimmagaddaNoch keine Bewertungen

- A Brief Analysis of Bharti-Zain Deal: C C C C C C C C C CDokument20 SeitenA Brief Analysis of Bharti-Zain Deal: C C C C C C C C C Crana_nidhi4Noch keine Bewertungen

- Analysis of Vodafone Essar IndiaDokument34 SeitenAnalysis of Vodafone Essar IndiaSantosh SamNoch keine Bewertungen

- TRAI Cloud Services Industry Body ConcernsDokument4 SeitenTRAI Cloud Services Industry Body ConcernsSubramanian RNoch keine Bewertungen

- Bharti 2airtel 1227851581611151 8Dokument49 SeitenBharti 2airtel 1227851581611151 8Kartik. SolankiNoch keine Bewertungen

- Marketing Strategy of Airtel and Its Promotional Strategy.Dokument48 SeitenMarketing Strategy of Airtel and Its Promotional Strategy.mbogadhiNoch keine Bewertungen

- Synopsis: Telecom Sector in IndiaDokument50 SeitenSynopsis: Telecom Sector in Indiarabi_kungleNoch keine Bewertungen

- INDIA TELECOMDokument49 SeitenINDIA TELECOMrabi_kungleNoch keine Bewertungen

- Papers on the field: Telecommunication Economic, Business, Regulation & PolicyVon EverandPapers on the field: Telecommunication Economic, Business, Regulation & PolicyNoch keine Bewertungen

- The Comprehensive Guide for Minority Tech Startups Securing Lucrative Government Contracts, Harnessing Business Opportunities, and Achieving Long-Term SuccessVon EverandThe Comprehensive Guide for Minority Tech Startups Securing Lucrative Government Contracts, Harnessing Business Opportunities, and Achieving Long-Term SuccessNoch keine Bewertungen

- The Time Value of MoneyDokument26 SeitenThe Time Value of MoneyshivpreetsandhuNoch keine Bewertungen

- Sale Leaseback & MortgageDokument30 SeitenSale Leaseback & MortgageshivpreetsandhuNoch keine Bewertungen

- Re 4Dokument10 SeitenRe 4shivpreetsandhuNoch keine Bewertungen

- Real EstateDokument25 SeitenReal Estateshivpreetsandhu100% (1)

- Re 1Dokument6 SeitenRe 1shivpreetsandhuNoch keine Bewertungen

- Exploring Real Estate InvestmentsDokument18 SeitenExploring Real Estate InvestmentssengtohNoch keine Bewertungen

- Real Estate Cycles What Is A Business Cycle?Dokument5 SeitenReal Estate Cycles What Is A Business Cycle?shivpreetsandhuNoch keine Bewertungen

- ICT DevelopmentDokument44 SeitenICT DevelopmentshivpreetsandhuNoch keine Bewertungen

- Housing For The Poor in IndiaDokument16 SeitenHousing For The Poor in IndiashivpreetsandhuNoch keine Bewertungen

- FAR PresentationDokument29 SeitenFAR PresentationshivpreetsandhuNoch keine Bewertungen

- Tower Infra2003Dokument30 SeitenTower Infra2003shivpreetsandhuNoch keine Bewertungen

- Is It Better To Deploy 3GDokument9 SeitenIs It Better To Deploy 3GshivpreetsandhuNoch keine Bewertungen

- Remote Infrastructure Monitoring & MGTDokument29 SeitenRemote Infrastructure Monitoring & MGTshivpreetsandhuNoch keine Bewertungen

- NGN Û Next Generation Network - Shivpreet, AbhijeevDokument29 SeitenNGN Û Next Generation Network - Shivpreet, AbhijeevshivpreetsandhuNoch keine Bewertungen

- ICTDokument21 SeitenICTshivpreetsandhuNoch keine Bewertungen

- Market Trends QualityDokument21 SeitenMarket Trends QualityshivpreetsandhuNoch keine Bewertungen

- LTEDokument36 SeitenLTEshivpreetsandhuNoch keine Bewertungen

- Guidelines Related To enDokument28 SeitenGuidelines Related To enshivpreetsandhuNoch keine Bewertungen

- In DOMAIN Registration DerDokument20 SeitenIn DOMAIN Registration DershivpreetsandhuNoch keine Bewertungen

- Indian TelecomDokument38 SeitenIndian TelecomshivpreetsandhuNoch keine Bewertungen

- ICT DevelopmentDokument49 SeitenICT DevelopmentshivpreetsandhuNoch keine Bewertungen

- GSM CDMA Network & Broadband Û India RoadmapDokument17 SeitenGSM CDMA Network & Broadband Û India RoadmapshivpreetsandhuNoch keine Bewertungen

- ICITM Relation To Service SupportDokument25 SeitenICITM Relation To Service SupportshivpreetsandhuNoch keine Bewertungen

- Sale of Goods Act ExplainedDokument147 SeitenSale of Goods Act ExplainedKhairun Nasuha Binti Mohamad Tahir A20B2134Noch keine Bewertungen

- Renewable Energy Snapshot: SloveniaDokument4 SeitenRenewable Energy Snapshot: SloveniaUNDP in Europe and Central AsiaNoch keine Bewertungen

- 978 93 5199 818 1 New - Rangoli TM 08Dokument132 Seiten978 93 5199 818 1 New - Rangoli TM 08Chaitanya AralkarNoch keine Bewertungen

- 209 Analysis and Comparison of The Contract Law For Small Medium and Large Enterprises in IndiaDokument6 Seiten209 Analysis and Comparison of The Contract Law For Small Medium and Large Enterprises in Indiatanishkasingh.ballbNoch keine Bewertungen

- Headquarters ITC Green Centre 10 Institutional Area, Sector 32Dokument1 SeiteHeadquarters ITC Green Centre 10 Institutional Area, Sector 32najakatNoch keine Bewertungen

- JCGL Project Balance of Works Completion Progress UpdateDokument12 SeitenJCGL Project Balance of Works Completion Progress UpdateSteve UkohaNoch keine Bewertungen

- Risk Mitigation and Vulnerability Assessment of Nam Dok Mai Mango (Mangifera Indica L.cv. Nam Dok Mai) Supply Chain Using Rapid Agricultural Supply Chain Risk Assessment (RapAgRisk)Dokument8 SeitenRisk Mitigation and Vulnerability Assessment of Nam Dok Mai Mango (Mangifera Indica L.cv. Nam Dok Mai) Supply Chain Using Rapid Agricultural Supply Chain Risk Assessment (RapAgRisk)Dhiyaa Ulhaq RikavianiNoch keine Bewertungen

- Pollution Adjudication BoardDokument10 SeitenPollution Adjudication Boardmaanyag6685Noch keine Bewertungen

- Comprehensive Analysis of Agriculture Business - JK Agri Genetics LTDDokument15 SeitenComprehensive Analysis of Agriculture Business - JK Agri Genetics LTDAkilesh KumarNoch keine Bewertungen

- Service Network - 20211007Dokument14 SeitenService Network - 20211007Antonis IsidorouNoch keine Bewertungen

- Housing loan details and documentsDokument2 SeitenHousing loan details and documentsArun PrasadNoch keine Bewertungen

- PLC & BCG matrix analysis of AsianPaintsDokument11 SeitenPLC & BCG matrix analysis of AsianPaintsNeeraj PrajapatNoch keine Bewertungen

- People Pattern and Process - Completo PDFDokument174 SeitenPeople Pattern and Process - Completo PDFCanul Koyok Andres AngelNoch keine Bewertungen

- Aditya Birla Group PPT PDF FreeDokument21 SeitenAditya Birla Group PPT PDF FreeShailesh KumarNoch keine Bewertungen

- A Business Plan On Bora Cereal ProductioDokument21 SeitenA Business Plan On Bora Cereal ProductioSimiyu K NelsonNoch keine Bewertungen

- Esurvey HisarDokument191 SeitenEsurvey HisarRahul DhawanNoch keine Bewertungen

- Quality Wireless (A) ... KEL153Dokument6 SeitenQuality Wireless (A) ... KEL153Amit Admune0% (1)

- 2021 03 28 17 59Dokument100 Seiten2021 03 28 17 59HASIBA MithunNoch keine Bewertungen

- Official Gazette Regulations on Insurance IntermediariesDokument142 SeitenOfficial Gazette Regulations on Insurance Intermediariespacs0% (1)

- Analytical Exposition TextDokument17 SeitenAnalytical Exposition TextraisyaaanadhifaaaNoch keine Bewertungen

- Realme Narzo 20 Pro (Black Ninja, 64 GB) : Grand Total 7678.00Dokument2 SeitenRealme Narzo 20 Pro (Black Ninja, 64 GB) : Grand Total 7678.00kishan mauryaNoch keine Bewertungen

- 1-BMCG2323 Introduction To ManufacturingDokument56 Seiten1-BMCG2323 Introduction To Manufacturinghemarubini96100% (1)

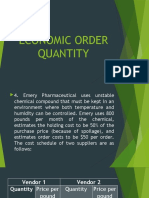

- EOQ Calculation for Chemical SupplierDokument11 SeitenEOQ Calculation for Chemical SupplierShaneen Angelique MoralesNoch keine Bewertungen

- JWR TariffDokument5 SeitenJWR TariffphilmikantNoch keine Bewertungen

- Protect Ashok Leyland from Counterfeit PartsDokument2 SeitenProtect Ashok Leyland from Counterfeit PartsAshwini Kumar JoshiNoch keine Bewertungen

- Indian Textile Industry: Opportunities, Challenges and SuggestionsDokument5 SeitenIndian Textile Industry: Opportunities, Challenges and Suggestionsgizex2013Noch keine Bewertungen

- Petra Capital Research Note Peer Next Door Valued 8x MoreDokument5 SeitenPetra Capital Research Note Peer Next Door Valued 8x MoretgitoenebNoch keine Bewertungen

- The House of Tata: Acquiring A Global FootprintDokument16 SeitenThe House of Tata: Acquiring A Global FootprintPunit PatelNoch keine Bewertungen

- Toyota's Five Forces AnalysisDokument5 SeitenToyota's Five Forces AnalysisOnalenna Tracy MaikanoNoch keine Bewertungen

- Bret Polfuss - Resume 2021Dokument2 SeitenBret Polfuss - Resume 2021api-533858450Noch keine Bewertungen