Das könnte Ihnen auch gefallen

- Liquidity RiskDokument24 SeitenLiquidity RiskTing YangNoch keine Bewertungen

- Asset Liability Management Banking Book - Tom Haczynski PDFDokument57 SeitenAsset Liability Management Banking Book - Tom Haczynski PDFvinaykansal1Noch keine Bewertungen

- Bank Audit Check List & Procedure (Concurrent Audit) : IndexDokument12 SeitenBank Audit Check List & Procedure (Concurrent Audit) : IndexCA Jay ThakurNoch keine Bewertungen

- Islamic Commercial BankingDokument26 SeitenIslamic Commercial BankingjmfaleelNoch keine Bewertungen

- SynopsisDokument7 SeitenSynopsisAnchalNoch keine Bewertungen

- R56 Fundamentals of Credit AnalysisDokument23 SeitenR56 Fundamentals of Credit AnalysisDiegoNoch keine Bewertungen

- Financial Market & InstrumentDokument73 SeitenFinancial Market & InstrumentSoumya ShettyNoch keine Bewertungen

- Financial Analysis of Britannia and DaburDokument8 SeitenFinancial Analysis of Britannia and DaburBiplab MondalNoch keine Bewertungen

- Sapm Unit 1Dokument49 SeitenSapm Unit 1Alavudeen ShajahanNoch keine Bewertungen

- Startup IndiaDokument3 SeitenStartup IndiaRipgod GamingNoch keine Bewertungen

- Risk Analysis and Protfolio ManagementDokument56 SeitenRisk Analysis and Protfolio ManagementVijetha Eddu100% (1)

- IapmDokument129 SeitenIapmKomal BagrodiaNoch keine Bewertungen

- 17.forecasting of Forex Market Using Technical AnalysisDokument65 Seiten17.forecasting of Forex Market Using Technical Analysisharrydeepak100% (1)

- IFRSDokument12 SeitenIFRSJeneef JoshuaNoch keine Bewertungen

- Fundamental Analysis - : Fundamentals: Quantitative and QualitativeDokument3 SeitenFundamental Analysis - : Fundamentals: Quantitative and QualitativeChandan KokaneNoch keine Bewertungen

- Working Capital Project Introduction On Vijaya DairyDokument8 SeitenWorking Capital Project Introduction On Vijaya DairyAnnapurna VinjamuriNoch keine Bewertungen

- NFO SBI Balanced Advantage Fund PresentationDokument25 SeitenNFO SBI Balanced Advantage Fund PresentationJohnTP100% (1)

- IAPM I IntroductionDokument23 SeitenIAPM I IntroductionSuresh Vadde100% (2)

- Study of Asset Liability Management in Indian BanksDokument14 SeitenStudy of Asset Liability Management in Indian Banksjitu_shinde20010Noch keine Bewertungen

- Mutual Fund AnalysisDokument67 SeitenMutual Fund Analysisakki reddyNoch keine Bewertungen

- Project On Technical AnalysisDokument32 SeitenProject On Technical AnalysisShubham BhatiaNoch keine Bewertungen

- Asset Liability Management QuestionnaireDokument9 SeitenAsset Liability Management QuestionnairePriya MhatreNoch keine Bewertungen

- Stock Investing Mastermind - Zebra Learn-85Dokument2 SeitenStock Investing Mastermind - Zebra Learn-85RGNitinDevaNoch keine Bewertungen

- Credit CreationDokument7 SeitenCredit CreationUmesh PrasadNoch keine Bewertungen

- FOREXDokument129 SeitenFOREXVANDANA GOYALNoch keine Bewertungen

- Fundamental and Technical Analysis of Portfolio Management.Dokument17 SeitenFundamental and Technical Analysis of Portfolio Management.Deven RathodNoch keine Bewertungen

- Study of Financial Derivatives (Futures & Options) : A Project Report On Functional ManagementDokument45 SeitenStudy of Financial Derivatives (Futures & Options) : A Project Report On Functional ManagementmaheshNoch keine Bewertungen

- Merchant Banking SyllabusDokument4 SeitenMerchant Banking SyllabusjeganrajrajNoch keine Bewertungen

- Equity ValuationDokument78 SeitenEquity ValuationReshma UdayNoch keine Bewertungen

- ICRRS Guidelines - BB - Version 2.0Dokument25 SeitenICRRS Guidelines - BB - Version 2.0Optimistic EyeNoch keine Bewertungen

- NBS Bank Limited IPO Prospectus PDFDokument119 SeitenNBS Bank Limited IPO Prospectus PDFKristi DuranNoch keine Bewertungen

- Synopsis Capital MarketDokument25 SeitenSynopsis Capital Marketdibyadrm100% (1)

- Portfolio SelectionDokument6 SeitenPortfolio SelectionAssfaw KebedeNoch keine Bewertungen

- Commodity Presentation (July 10)Dokument33 SeitenCommodity Presentation (July 10)Nitin ShindeNoch keine Bewertungen

- Treasury Management Strategies and Challenges in The Banking IndustryDokument46 SeitenTreasury Management Strategies and Challenges in The Banking IndustryDaniel Obasi100% (1)

- A Study About Investment & Transition in Indian Derivative Markets.Dokument79 SeitenA Study About Investment & Transition in Indian Derivative Markets.SurajKashidNoch keine Bewertungen

- Designing A Global Financing StrategyDokument23 SeitenDesigning A Global Financing StrategyShankar ReddyNoch keine Bewertungen

- Portfolio Management Services - HDFCDokument73 SeitenPortfolio Management Services - HDFCArunKumarNoch keine Bewertungen

- Sharpe Index Model: Portfolio Expected Return E (R) oDokument2 SeitenSharpe Index Model: Portfolio Expected Return E (R) oAlissa BarnesNoch keine Bewertungen

- Treasury Management AssignmentDokument4 SeitenTreasury Management AssignmentJed Bentillo100% (1)

- Indian Debt MarketDokument32 SeitenIndian Debt MarketProfessorAsim Kumar Mishra0% (1)

- A Study On Investors Perception Towards Initial Public Offering in MumbaiDokument13 SeitenA Study On Investors Perception Towards Initial Public Offering in MumbaiRushabh JariwalaNoch keine Bewertungen

- Managing Personal Finance NotesDokument32 SeitenManaging Personal Finance NotesMonashreeNoch keine Bewertungen

- Hand Book For NSDL Depository Operations Module 3Dokument108 SeitenHand Book For NSDL Depository Operations Module 3mhussainNoch keine Bewertungen

- Asg 1 Role of Finance ManagerDokument2 SeitenAsg 1 Role of Finance ManagerRokov N ZhasaNoch keine Bewertungen

- Mcom Economics Project Semi IDokument33 SeitenMcom Economics Project Semi IAbhishek MishraNoch keine Bewertungen

- Financial Performance AnalysisDokument106 SeitenFinancial Performance AnalysisVasu GongadaNoch keine Bewertungen

- Index: Audit of BankDokument63 SeitenIndex: Audit of Bankritesh shrinewarNoch keine Bewertungen

- Central BankDokument9 SeitenCentral BanksakibNoch keine Bewertungen

- Forex MarketDokument33 SeitenForex Marketaniket7gNoch keine Bewertungen

- Blackbook Project On Indian Banking Sector 2Dokument119 SeitenBlackbook Project On Indian Banking Sector 2anilmourya5Noch keine Bewertungen

- Wealth ManagementDokument97 SeitenWealth ManagementShashank100% (1)

- Asset Liability Management in BanksDokument29 SeitenAsset Liability Management in BanksAashima Sharma BhasinNoch keine Bewertungen

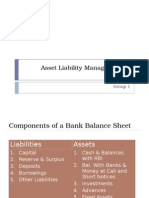

- Asset Liability Management in Banks: Group 1Dokument29 SeitenAsset Liability Management in Banks: Group 1AjDonNoch keine Bewertungen

- Assets Liability ManagementDokument28 SeitenAssets Liability Managementpriyanka choudharyNoch keine Bewertungen

- Asset Liability ManagementDokument18 SeitenAsset Liability Managementmahesh19689Noch keine Bewertungen

- Asset Liability Management: in BanksDokument44 SeitenAsset Liability Management: in Bankssachin21singhNoch keine Bewertungen

- Financial Risk Management: A Simple IntroductionVon EverandFinancial Risk Management: A Simple IntroductionBewertung: 4.5 von 5 Sternen4.5/5 (7)

- MFS - Asset Liability Management MuskanDokument33 SeitenMFS - Asset Liability Management Muskansangambhardwaj64Noch keine Bewertungen

- V JNLJNLJR X H/XV - V: Pit A Ptt7D /TDokument10 SeitenV JNLJNLJR X H/XV - V: Pit A Ptt7D /TAkhil SablokNoch keine Bewertungen

- RBI Guidelines On Currency ManagementDokument16 SeitenRBI Guidelines On Currency Managementeknath2000Noch keine Bewertungen

- Law of Limitation in BankingDokument13 SeitenLaw of Limitation in Bankingeknath2000100% (1)

- Communication Skills For BankersDokument12 SeitenCommunication Skills For Bankerseknath2000Noch keine Bewertungen

- Credit Management - A Conceptual FrameworkDokument30 SeitenCredit Management - A Conceptual Frameworkeknath200050% (2)

- Characteristic of SME IndustryDokument5 SeitenCharacteristic of SME Industryeknath2000100% (1)

- Mergers and AcquisitionsDokument34 SeitenMergers and Acquisitionseknath2000Noch keine Bewertungen

- Various Methods of Payment in International TradeDokument63 SeitenVarious Methods of Payment in International Tradeeknath2000Noch keine Bewertungen

- Preparation Readying For Sales MeetingDokument18 SeitenPreparation Readying For Sales Meetingeknath2000Noch keine Bewertungen

- Legal and Regulatory Aspects of BankingDokument216 SeitenLegal and Regulatory Aspects of Bankingeknath2000Noch keine Bewertungen

- Master Direction On Import of Goods and ServicesDokument31 SeitenMaster Direction On Import of Goods and Serviceseknath2000Noch keine Bewertungen

- Jaiib Module ADokument25 SeitenJaiib Module Aeknath2000Noch keine Bewertungen

- Marketing and Customer ServiceDokument109 SeitenMarketing and Customer Serviceeknath2000Noch keine Bewertungen

- CASA Centric StrategyDokument40 SeitenCASA Centric Strategyeknath2000Noch keine Bewertungen

- Kakada Aarti-Bhajani MalikaDokument48 SeitenKakada Aarti-Bhajani Malikaeknath2000100% (3)

- UCP 600 Effective From 1 July 2007 AnDokument36 SeitenUCP 600 Effective From 1 July 2007 Aneknath2000Noch keine Bewertungen

- Customer Service & Customer Delight: The Bridge To Our CustomersDokument34 SeitenCustomer Service & Customer Delight: The Bridge To Our Customerseknath2000Noch keine Bewertungen

- Treasury and Fund Management in BanksDokument40 SeitenTreasury and Fund Management in Bankseknath2000100% (2)

- Ekadashi Mahatmya-01 - MarathiDokument50 SeitenEkadashi Mahatmya-01 - Marathieknath2000100% (3)

- What Is International TradeDokument2 SeitenWhat Is International Tradeeknath2000Noch keine Bewertungen

- Disclosure in Financial Statements - Notes To AccountsDokument25 SeitenDisclosure in Financial Statements - Notes To Accountseknath2000Noch keine Bewertungen

- Financial ServicesDokument161 SeitenFinancial Serviceseknath2000Noch keine Bewertungen

- Bhajani MalikaDokument288 SeitenBhajani Malikaeknath2000Noch keine Bewertungen

- International Business EnvironmentDokument17 SeitenInternational Business Environmenteknath2000Noch keine Bewertungen

- Preventive VigilanceDokument12 SeitenPreventive Vigilanceeknath2000Noch keine Bewertungen

- Cost of Capital and Capital Budgeting TechniquesDokument23 SeitenCost of Capital and Capital Budgeting TechniquesUmay PelitNoch keine Bewertungen

- Table A Consolidated Income Statement, 2009-2011 (In Thousands of Dollars)Dokument30 SeitenTable A Consolidated Income Statement, 2009-2011 (In Thousands of Dollars)rooptejaNoch keine Bewertungen

- Audit of Sales and Account ReceivablesDokument26 SeitenAudit of Sales and Account ReceivablesnikoNoch keine Bewertungen

- 4 - Ona V CirDokument6 Seiten4 - Ona V CircloudNoch keine Bewertungen

- Analysis On Tiga Pilar SejahteraDokument3 SeitenAnalysis On Tiga Pilar SejahteraridaNoch keine Bewertungen

- Digest (Partnership Dissolution)Dokument4 SeitenDigest (Partnership Dissolution)Steve NapalitNoch keine Bewertungen

- AssignmentDokument5 SeitenAssignmentPrashanthRameshNoch keine Bewertungen

- Assets, Liabilities and Equity of ARA Galleries Pty LTD As at 30 June 2017Dokument4 SeitenAssets, Liabilities and Equity of ARA Galleries Pty LTD As at 30 June 2017BáchHợpNoch keine Bewertungen

- INSURANCE FINALsDokument4 SeitenINSURANCE FINALsNonoy D VolosoNoch keine Bewertungen

- Order in Respect of Mangalam Agro Products LimitedDokument15 SeitenOrder in Respect of Mangalam Agro Products LimitedShyam SunderNoch keine Bewertungen

- Certificate in Advanced Business Calculations: Series 2 Examination 2008Dokument5 SeitenCertificate in Advanced Business Calculations: Series 2 Examination 2008Apollo YapNoch keine Bewertungen

- EW00467 Annual Report 2018Dokument148 SeitenEW00467 Annual Report 2018rehan7777Noch keine Bewertungen

- Sam Seiden CBOT KeepItSimpleDokument3 SeitenSam Seiden CBOT KeepItSimpleferritape100% (2)

- Credit Case TitleDokument9 SeitenCredit Case TitlePatrick James TanNoch keine Bewertungen

- Auditing 2Dokument10 SeitenAuditing 2Nan Laron ParrochaNoch keine Bewertungen

- Definition of TermsDokument8 SeitenDefinition of TermsMark Luigi DeTomas RosarioNoch keine Bewertungen

- Financial Management in Sick UnitsDokument22 SeitenFinancial Management in Sick UnitsAnkit SinghNoch keine Bewertungen

- Bonds and Their Valuation ExerciseDokument42 SeitenBonds and Their Valuation ExerciseLee Wong100% (1)

- ACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneDokument33 SeitenACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneGabriel L. CaringalNoch keine Bewertungen

- Project Profile-HDPE Bottles & ContainersDokument7 SeitenProject Profile-HDPE Bottles & ContainersHetal Patel0% (2)

- International Business Level Strategies PPT 03Dokument7 SeitenInternational Business Level Strategies PPT 03acidangelsterNoch keine Bewertungen

- Risk and Return Trade OffDokument14 SeitenRisk and Return Trade OffDebabrata SutarNoch keine Bewertungen

- Laporan Keuangan Ace Hardware 2014-Q1 PDFDokument44 SeitenLaporan Keuangan Ace Hardware 2014-Q1 PDFBang BegsNoch keine Bewertungen

- Lecture 3 Ratio AnalysisDokument59 SeitenLecture 3 Ratio AnalysisJiun Herng LeeNoch keine Bewertungen

- Critical Evaluation of Financial Reporting Act 2015: An Assignment OnDokument4 SeitenCritical Evaluation of Financial Reporting Act 2015: An Assignment OnTanvir SazzadNoch keine Bewertungen

- Globe TelecomDokument8 SeitenGlobe TelecomLesterAntoniDeGuzmanNoch keine Bewertungen

- Cross Border Transactions HandbookDokument232 SeitenCross Border Transactions Handbookralphhvillanueva100% (2)

- Kohinoor ChemicalDokument21 SeitenKohinoor ChemicalFaisal AhmedNoch keine Bewertungen

- Introduction To Financial Mathematics OpDokument23 SeitenIntroduction To Financial Mathematics OpLuca PilottiNoch keine Bewertungen

- Andhra Pradesh EconomyDokument95 SeitenAndhra Pradesh EconomyKrishna PrasadNoch keine Bewertungen