Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Fundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualDokument25 SeitenFundamentals of Futures and Options Markets 8th Edition Hull Solutions ManualBeckySmithnxro98% (62)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- ERP Part 2 Final Exam 2019 PDFDokument91 SeitenERP Part 2 Final Exam 2019 PDFMrugesh100% (3)

- Merton Electronics Corp: - by Alexzander Downs - Ferdinand Hilton - Kevin Grant - Takshal BhansaliDokument18 SeitenMerton Electronics Corp: - by Alexzander Downs - Ferdinand Hilton - Kevin Grant - Takshal BhansalihopetofindmyownwayNoch keine Bewertungen

- Week 4 Tutorial Questions and Solutions: U D U DDokument4 SeitenWeek 4 Tutorial Questions and Solutions: U D U Dmuller1234Noch keine Bewertungen

- Hull: Options, Futures, and Other Derivatives, Ninth Edition Chapter 11: Properties of Stock Options Multiple Choice Test Bank: QuestionsDokument4 SeitenHull: Options, Futures, and Other Derivatives, Ninth Edition Chapter 11: Properties of Stock Options Multiple Choice Test Bank: QuestionsNgân Hà NguyễnNoch keine Bewertungen

- FIN 413 - Midterm #2 SolutionsDokument6 SeitenFIN 413 - Midterm #2 SolutionsWesley CheungNoch keine Bewertungen

- OIS Discounting PiterbargDokument6 SeitenOIS Discounting PiterbargharsjusNoch keine Bewertungen

- How To Be A Successful Option Scalper Using OI PulseDokument223 SeitenHow To Be A Successful Option Scalper Using OI PulseVarun Parihari100% (1)

- A Simple Options Trading Strategy Based On Technical IndicatorsDokument4 SeitenA Simple Options Trading Strategy Based On Technical IndicatorsMnvd prasadNoch keine Bewertungen

- Call & Put OptionDokument4 SeitenCall & Put OptionvvpvarunNoch keine Bewertungen

- Equity Derivatives CheatsheetDokument1 SeiteEquity Derivatives CheatsheetMarco Avello IbarraNoch keine Bewertungen

- Management of Transaction ExposureDokument10 SeitenManagement of Transaction ExposuredediismeNoch keine Bewertungen

- Revision For Exams NBDokument15 SeitenRevision For Exams NBDan Saul KnightNoch keine Bewertungen

- (JP Morgan) Just What You Need To Know About Variance SwapsDokument30 Seiten(JP Morgan) Just What You Need To Know About Variance Swapsmarco_aita100% (1)

- Currency Derivatives - WorkbookDokument95 SeitenCurrency Derivatives - Workbookapi-19974928100% (1)

- NISM Mock 4 PDFDokument41 SeitenNISM Mock 4 PDFnewbie194767% (3)

- Conventions Single Name Credit Default Swaps OpenGamma PDFDokument12 SeitenConventions Single Name Credit Default Swaps OpenGamma PDFRajesh NeppalliNoch keine Bewertungen

- Samples and InstructionsDokument479 SeitenSamples and InstructionsWunmi OlaNoch keine Bewertungen

- Options vs. Futures: What's The Difference?: Investopedia StaffDokument3 SeitenOptions vs. Futures: What's The Difference?: Investopedia StaffJonhmark AniñonNoch keine Bewertungen

- Eagle Builders Inc Initiated A Stock Option Plan For ItsDokument1 SeiteEagle Builders Inc Initiated A Stock Option Plan For ItsTaimour HassanNoch keine Bewertungen

- Solution PDFDokument5 SeitenSolution PDFVicky MajumdarNoch keine Bewertungen

- FRM Unit-3Dokument29 SeitenFRM Unit-3prasanthi CNoch keine Bewertungen

- International Economics, 7e (Husted/Melvin) Chapter 13 The Foreign Exchange MarketDokument19 SeitenInternational Economics, 7e (Husted/Melvin) Chapter 13 The Foreign Exchange MarketAli AlshehhiNoch keine Bewertungen

- T11 Treasury Operations IIDokument5 SeitenT11 Treasury Operations IIkhongst-wb22Noch keine Bewertungen

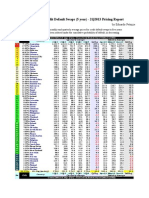

- Sovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportDokument1 SeiteSovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportEduardo PetazzeNoch keine Bewertungen

- Preface: National Institute of Financial Market (NIFMDokument65 SeitenPreface: National Institute of Financial Market (NIFMSankitNoch keine Bewertungen

- Hedge Accounting PresentationDokument29 SeitenHedge Accounting PresentationAshwini Amit ShenoyNoch keine Bewertungen

- R58 Basics of Derivative Pricing and Valuation - Q BankDokument17 SeitenR58 Basics of Derivative Pricing and Valuation - Q BankAdnan AshrafNoch keine Bewertungen