Das könnte Ihnen auch gefallen

- Key Features and Valuation of BondsDokument40 SeitenKey Features and Valuation of BondsNeneng WulandariNoch keine Bewertungen

- Make $50 A Day Autopilot MethodDokument4 SeitenMake $50 A Day Autopilot MethodJadon BoytonNoch keine Bewertungen

- Budgetary Planning: Learning ObjectivesDokument75 SeitenBudgetary Planning: Learning ObjectivesRomuell Banares100% (1)

- Linde E18P-02Dokument306 SeitenLinde E18P-02ludecar hyster100% (4)

- Hansen AISE IM Ch08Dokument54 SeitenHansen AISE IM Ch08indah100% (1)

- Financial Analysis Chapter 2: Review of Key Financial StatementsDokument102 SeitenFinancial Analysis Chapter 2: Review of Key Financial StatementsJose MartinezNoch keine Bewertungen

- Financial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersVon EverandFinancial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersNoch keine Bewertungen

- Habawel V Court of Tax AppealsDokument1 SeiteHabawel V Court of Tax AppealsPerry RubioNoch keine Bewertungen

- University of San Jose Strategic Business Analysis Budgeting OverviewDokument16 SeitenUniversity of San Jose Strategic Business Analysis Budgeting OverviewLayla MainNoch keine Bewertungen

- Topic 2 Financial Statements AnalysisDokument84 SeitenTopic 2 Financial Statements AnalysisTommyYapNoch keine Bewertungen

- Willie Chee Keong Tan - Research Methods (2018, World Scientific Publishing Company) - Libgen - Li PDFDokument236 SeitenWillie Chee Keong Tan - Research Methods (2018, World Scientific Publishing Company) - Libgen - Li PDFakshar pandavNoch keine Bewertungen

- Budgeting guide with tips and templatesDokument3 SeitenBudgeting guide with tips and templatesMarielle CastañedaNoch keine Bewertungen

- Finesse Service ManualDokument34 SeitenFinesse Service ManualLuis Sivira100% (1)

- Should Always: Exercise 1-1. True or FalseDokument7 SeitenShould Always: Exercise 1-1. True or FalseDeanmark RondinaNoch keine Bewertungen

- Lecture 4 - Profit PlanningDokument81 SeitenLecture 4 - Profit PlanningDaphne PerezNoch keine Bewertungen

- Management Accounting: Student EditionDokument28 SeitenManagement Accounting: Student EditionJackson Ubulele DadeNoch keine Bewertungen

- Management Accounting: Budgeting For Planning & ControlDokument42 SeitenManagement Accounting: Budgeting For Planning & ControlNurvia Dwi RahmawatiNoch keine Bewertungen

- Management Accounting: Budgeting For Planning & ControlDokument50 SeitenManagement Accounting: Budgeting For Planning & ControlFariz AlfariziNoch keine Bewertungen

- Hansen AISE IM Ch08Dokument54 SeitenHansen AISE IM Ch08AimanNoch keine Bewertungen

- MAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingDokument6 SeitenMAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingLOUISE ELIJAH GACUANNoch keine Bewertungen

- Budgetary Planning and Control: 7.1 Nature and Purposes of BudgetsDokument18 SeitenBudgetary Planning and Control: 7.1 Nature and Purposes of Budgetsserge folegweNoch keine Bewertungen

- Profit Planning BudgetsDokument67 SeitenProfit Planning BudgetsAparna GoliNoch keine Bewertungen

- Budgetary Planning EssentialsDokument50 SeitenBudgetary Planning EssentialsVahrul DavidNoch keine Bewertungen

- Cost PPT PrelimsDokument148 SeitenCost PPT PrelimsNochook SatelliteNoch keine Bewertungen

- AKMEN Pertm 4, 5Dokument127 SeitenAKMEN Pertm 4, 5UJI TESTNoch keine Bewertungen

- Financial Ratios: Liquidity: Lesson 2.2Dokument73 SeitenFinancial Ratios: Liquidity: Lesson 2.2Friendlyn AzulNoch keine Bewertungen

- Profit Planning: Asic Framework of Budgeting AccountingDokument5 SeitenProfit Planning: Asic Framework of Budgeting AccountingMichaela CruzNoch keine Bewertungen

- The Financial Plan: Learning ObjectivesDokument22 SeitenThe Financial Plan: Learning ObjectivesJAYANT MAHAJANNoch keine Bewertungen

- 18-10-2022-Activity Based BudgetingDokument32 Seiten18-10-2022-Activity Based Budgeting020Abhisek KhadangaNoch keine Bewertungen

- Finance II Materials McNeil 2020Dokument43 SeitenFinance II Materials McNeil 2020Atharva ManjrekarNoch keine Bewertungen

- Budgeting 101: By: Limheya Lester Glenn National University-ManilaDokument42 SeitenBudgeting 101: By: Limheya Lester Glenn National University-ManilaXXXXXXXXXXXXXXXXXXNoch keine Bewertungen

- CH - 2 For TeacherDokument11 SeitenCH - 2 For TeacherEbsa AdemeNoch keine Bewertungen

- BPC-Business Plan-Budget PlanDokument2 SeitenBPC-Business Plan-Budget PlanJacklyn LadeslaNoch keine Bewertungen

- Ch. 8 - Master Budgeting Flashcards - QuizletDokument11 SeitenCh. 8 - Master Budgeting Flashcards - QuizletBisag AsaNoch keine Bewertungen

- IPPTChap013 000Dokument39 SeitenIPPTChap013 000Merly JusayanNoch keine Bewertungen

- Chapter 8 Master Budgeting Flashcards - QuizletDokument4 SeitenChapter 8 Master Budgeting Flashcards - QuizletBisag AsaNoch keine Bewertungen

- UNIT-5 QB-20FTO04 - Process Economics and Industrial ManagementDokument16 SeitenUNIT-5 QB-20FTO04 - Process Economics and Industrial Managementjawaharkumar MBANoch keine Bewertungen

- Budgets: Trefor Mcelroy September/October 2017Dokument35 SeitenBudgets: Trefor Mcelroy September/October 2017Nguyễn Hạnh LinhNoch keine Bewertungen

- Finance Business Analyst JD J MandaDokument6 SeitenFinance Business Analyst JD J MandaBenard ChimhondoNoch keine Bewertungen

- Lecture 7 - The Master BudgetDokument11 SeitenLecture 7 - The Master BudgetSherlyn SempleNoch keine Bewertungen

- Budget Matterial For The Students NewDokument10 SeitenBudget Matterial For The Students NewheysemNoch keine Bewertungen

- T1 Budget For Planning S2-1718Dokument11 SeitenT1 Budget For Planning S2-1718Faizah MKNoch keine Bewertungen

- Mepl CostingDokument303 SeitenMepl CostingVinay KumarNoch keine Bewertungen

- 4 Financial Forecasting, Planning, and BudgetingDokument20 Seiten4 Financial Forecasting, Planning, and BudgetingMarlon LadesmaNoch keine Bewertungen

- Master Budgeting Unit 6Dokument20 SeitenMaster Budgeting Unit 6Maiah Ysabel KaamiñoNoch keine Bewertungen

- Topic 3 - Budgeting and Budgetary ControlDokument42 SeitenTopic 3 - Budgeting and Budgetary ControlSYAZANA HUDA MOHD AZLINoch keine Bewertungen

- Chap002 Without Key AnswersDokument69 SeitenChap002 Without Key AnswersVan TranNoch keine Bewertungen

- Published AccountsDokument31 SeitenPublished AccountsGraceii Mecayer CuizonNoch keine Bewertungen

- FMA Chapter 02ADokument34 SeitenFMA Chapter 02Ameaza mollaNoch keine Bewertungen

- Budgeting ChapterDokument17 SeitenBudgeting ChapteraasNoch keine Bewertungen

- 16Dokument21 Seiten16meryroselicaros525Noch keine Bewertungen

- Ch9 - Budgetary PlanningDokument24 SeitenCh9 - Budgetary PlanningTú NguyênNoch keine Bewertungen

- BUDGET in Health by Dr. Md. Nazmul Hassan RefatDokument7 SeitenBUDGET in Health by Dr. Md. Nazmul Hassan RefatEti BaruaNoch keine Bewertungen

- Budgeting for Planning and ControlDokument25 SeitenBudgeting for Planning and ControlCiara Angily Abad GinetaNoch keine Bewertungen

- Master Budgeting Master Budgeting: The Basic Framework of BudgetingDokument18 SeitenMaster Budgeting Master Budgeting: The Basic Framework of Budgetingalberto.roberto90Noch keine Bewertungen

- Budgetary Control Lesson GuideDokument11 SeitenBudgetary Control Lesson GuiderscjatNoch keine Bewertungen

- Group Iii. Business FinanceDokument11 SeitenGroup Iii. Business FinanceChristian PhilipNoch keine Bewertungen

- Topic 4: Trial Balance: Learning ObjectivesDokument5 SeitenTopic 4: Trial Balance: Learning ObjectivesAzim OthmanNoch keine Bewertungen

- MOD 05 Planning & Budgeting (2023)Dokument53 SeitenMOD 05 Planning & Budgeting (2023)georgiana.ioannouNoch keine Bewertungen

- Fundamentals of Accountancy, Business and Management 2: Lesson 5 - 6: Financial Statement AnalysisDokument2 SeitenFundamentals of Accountancy, Business and Management 2: Lesson 5 - 6: Financial Statement AnalysisJerico MarcelinoNoch keine Bewertungen

- CH 01Dokument20 SeitenCH 01saif khanNoch keine Bewertungen

- CH 01Dokument20 SeitenCH 01tahira awanNoch keine Bewertungen

- 5 Profit PlanningDokument17 Seiten5 Profit PlanningFebbie Novem LavariasNoch keine Bewertungen

- Financial PlanningDokument7 SeitenFinancial Planningp.dashaelaineNoch keine Bewertungen

- 03 Financial PlanningDokument34 Seiten03 Financial PlanningReza MuhammadNoch keine Bewertungen

- Lesson Plan in Business FinanceDokument9 SeitenLesson Plan in Business FinanceEmelen VeranoNoch keine Bewertungen

- Responsibility CenterDokument32 SeitenResponsibility CenterNeneng WulandariNoch keine Bewertungen

- Chapter 1 Lecture - WulanDokument16 SeitenChapter 1 Lecture - WulanNeneng WulandariNoch keine Bewertungen

- Stocks and Their Valuation: Taufikur@ugm - Ac.idDokument43 SeitenStocks and Their Valuation: Taufikur@ugm - Ac.idNeneng Wulandari100% (1)

- AML Sesi 6Dokument3 SeitenAML Sesi 6Neneng WulandariNoch keine Bewertungen

- Mergers and Acquisitions: Rights Reserved. Mcgraw-Hill/IrwinDokument23 SeitenMergers and Acquisitions: Rights Reserved. Mcgraw-Hill/Irwinkkn35Noch keine Bewertungen

- ch30 M&ADokument32 Seitench30 M&ANeneng WulandariNoch keine Bewertungen

- Options and Corporate Finance: Basic ConceptsDokument68 SeitenOptions and Corporate Finance: Basic ConceptsNeneng WulandariNoch keine Bewertungen

- Strengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsDokument16 SeitenStrengthening A Company'S Competitive Position: Strategic Moves, Timing, and Scope of OperationsNeneng WulandariNoch keine Bewertungen

- The Cost of Capital: Taufikur@ugm - Ac.idDokument31 SeitenThe Cost of Capital: Taufikur@ugm - Ac.idNeneng WulandariNoch keine Bewertungen

- Strategies For Competing in International Markets: Student VersionDokument15 SeitenStrategies For Competing in International Markets: Student VersionNeneng WulandariNoch keine Bewertungen

- Determining and Forecasting Exchange Rates: Factors, Systems, and FX Market PlayersDokument4 SeitenDetermining and Forecasting Exchange Rates: Factors, Systems, and FX Market PlayersNeneng WulandariNoch keine Bewertungen

- Types of Forex Exposure and Transaction Risk ManagementDokument13 SeitenTypes of Forex Exposure and Transaction Risk ManagementNeneng WulandariNoch keine Bewertungen

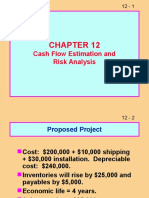

- CH 12 Cash Flow Estimatision and Risk AnalysisDokument39 SeitenCH 12 Cash Flow Estimatision and Risk AnalysisNeneng WulandariNoch keine Bewertungen

- Audit PrinciplesDokument34 SeitenAudit PrinciplesJhayanti Nithyananda KalyaniNoch keine Bewertungen

- Types of Forex Exposure and Transaction Risk ManagementDokument13 SeitenTypes of Forex Exposure and Transaction Risk ManagementNeneng WulandariNoch keine Bewertungen

- 1 Effect of Governance On Credit DecitionsDokument21 Seiten1 Effect of Governance On Credit DecitionsANISANoch keine Bewertungen

- Book 1 BelajarDokument1 SeiteBook 1 BelajarNeneng WulandariNoch keine Bewertungen

- MAHM8e Chapter03.Ab - AzDokument27 SeitenMAHM8e Chapter03.Ab - AzDinda OktavianiNoch keine Bewertungen

- Management Accounting: Student EditionDokument27 SeitenManagement Accounting: Student EditionNeneng WulandariNoch keine Bewertungen

- Management Accounting: Student EditionDokument24 SeitenManagement Accounting: Student EditionNeneng WulandariNoch keine Bewertungen

- HTTP Tugas EnronDokument1 SeiteHTTP Tugas EnronNeneng WulandariNoch keine Bewertungen

- Responsibility Centers: Types, Performance Measurement and Transfer PricingDokument32 SeitenResponsibility Centers: Types, Performance Measurement and Transfer PricingNeneng WulandariNoch keine Bewertungen

- Managerial Accounting: Student EditionDokument21 SeitenManagerial Accounting: Student EditionNeneng WulandariNoch keine Bewertungen

- 231025+ +JBS+3Q23+Earnings+Preview VFDokument3 Seiten231025+ +JBS+3Q23+Earnings+Preview VFgicokobayashiNoch keine Bewertungen

- Relationship Between Effective Pain Management and Patient RecoveryDokument4 SeitenRelationship Between Effective Pain Management and Patient RecoveryAkinyiNoch keine Bewertungen

- Carbon Trust Certification OverviewDokument2 SeitenCarbon Trust Certification OverviewMatt MaceNoch keine Bewertungen

- University of Texas at Arlington Fall 2011 Diagnostic Exam Text and Topic Reference Guide For Electrical Engineering DepartmentDokument3 SeitenUniversity of Texas at Arlington Fall 2011 Diagnostic Exam Text and Topic Reference Guide For Electrical Engineering Departmentnuzhat_mansurNoch keine Bewertungen

- Deped Tacloban City 05202020 PDFDokument2 SeitenDeped Tacloban City 05202020 PDFDon MarkNoch keine Bewertungen

- Accor vs Airbnb: Business Models in Digital EconomyDokument4 SeitenAccor vs Airbnb: Business Models in Digital EconomyAkash PayunNoch keine Bewertungen

- StarletDokument16 SeitenStarletMohsen SirajNoch keine Bewertungen

- Offer Letter - Kunal Saxena (Gurgaon)Dokument5 SeitenOffer Letter - Kunal Saxena (Gurgaon)Neelesh PandeyNoch keine Bewertungen

- Analytic Solver Platform For Education: Setting Up The Course CodeDokument2 SeitenAnalytic Solver Platform For Education: Setting Up The Course CodeTrevor feignarddNoch keine Bewertungen

- Restore a Disk Image with ClonezillaDokument16 SeitenRestore a Disk Image with ClonezillaVictor SantosNoch keine Bewertungen

- COKE MidtermDokument46 SeitenCOKE MidtermKomal SharmaNoch keine Bewertungen

- CRM Chapter 3 Builds Customer RelationshipsDokument45 SeitenCRM Chapter 3 Builds Customer RelationshipsPriya Datta100% (1)

- 2014 Chevrolet Cruze maintenance schedule guideDokument2 Seiten2014 Chevrolet Cruze maintenance schedule guidericardo rodriguezNoch keine Bewertungen

- Desarmado y Armado de Transmision 950BDokument26 SeitenDesarmado y Armado de Transmision 950Bedilberto chableNoch keine Bewertungen

- Dani RodrikDokument12 SeitenDani Rodrikprogramas4242Noch keine Bewertungen

- Kj1010-6804-Man604-Man205 - Chapter 7Dokument16 SeitenKj1010-6804-Man604-Man205 - Chapter 7ghalibNoch keine Bewertungen

- 60 Years of Cannes Lions Infographics: The 50sDokument9 Seiten60 Years of Cannes Lions Infographics: The 50sSapientNitroNoch keine Bewertungen

- Kinds of ObligationDokument50 SeitenKinds of ObligationKIM GABRIEL PAMITTANNoch keine Bewertungen

- Webpage citation guideDokument4 SeitenWebpage citation guiderogelyn samilinNoch keine Bewertungen

- BSC in EEE Full Syllabus (Credit+sylabus)Dokument50 SeitenBSC in EEE Full Syllabus (Credit+sylabus)Sydur RahmanNoch keine Bewertungen

- Maximum Yield USA 2013 December PDFDokument190 SeitenMaximum Yield USA 2013 December PDFmushroomman88Noch keine Bewertungen

- JEdwards PaperDokument94 SeitenJEdwards PaperHassan Hitch Adamu LafiaNoch keine Bewertungen

- GFRDDokument9 SeitenGFRDLalit NagarNoch keine Bewertungen

- DMT80600L104 21WTR Datasheet DATASHEETDokument3 SeitenDMT80600L104 21WTR Datasheet DATASHEETtnenNoch keine Bewertungen