Das könnte Ihnen auch gefallen

- Options Theory Guide for Professional TradingDokument134 SeitenOptions Theory Guide for Professional TradingVibhats VibhorNoch keine Bewertungen

- Social Media Marketing ProposalDokument7 SeitenSocial Media Marketing Proposalsaurabh100% (3)

- Delays and Disruption Hudson FormulaDokument2 SeitenDelays and Disruption Hudson FormulaGordan CelarNoch keine Bewertungen

- 03-Cost Concepts and Design Economics CHE40ADokument65 Seiten03-Cost Concepts and Design Economics CHE40AFaye Blair MarkovaNoch keine Bewertungen

- ECH 158A Economic Analysis and Design: Cost Estimation TechniquesDokument60 SeitenECH 158A Economic Analysis and Design: Cost Estimation TechniquesLe Anh QuânNoch keine Bewertungen

- Business Plan 2 - 2020Dokument22 SeitenBusiness Plan 2 - 2020fajarf100% (1)

- Material Ledgers: Actual Costing - SAP BlogsDokument34 SeitenMaterial Ledgers: Actual Costing - SAP Blogsvivaldikid0% (1)

- Financial Problems of StartupsDokument65 SeitenFinancial Problems of StartupsSoham Dalvi100% (2)

- Ec 101 CHP 07Dokument24 SeitenEc 101 CHP 07Hudzaifah ZaidanNoch keine Bewertungen

- Ch07Dokument23 SeitenCh07Aisha AzamNoch keine Bewertungen

- Short-Run Costs and Output Decisions: Prepared By: Fernando Quijano and Yvonn QuijanoDokument25 SeitenShort-Run Costs and Output Decisions: Prepared By: Fernando Quijano and Yvonn QuijanoSari MolisaNoch keine Bewertungen

- Short-Run Costs and Output DecisionsDokument30 SeitenShort-Run Costs and Output DecisionsDevi AryaNoch keine Bewertungen

- Ch-8 - Ist Sem 23-24Dokument82 SeitenCh-8 - Ist Sem 23-24Hrishikesh KasatNoch keine Bewertungen

- Costs and Output Decisions in The Long RunDokument39 SeitenCosts and Output Decisions in The Long Runforensic accNoch keine Bewertungen

- Case Econ08 Ab - Az.ppt 08Dokument31 SeitenCase Econ08 Ab - Az.ppt 08matthews bwalyaNoch keine Bewertungen

- 07-The Production Process:The Behavior of Profit - Maximizing FirmsDokument26 Seiten07-The Production Process:The Behavior of Profit - Maximizing FirmsSHUBHAM SINGHNoch keine Bewertungen

- Long-Run Costs and Output DecisionsDokument38 SeitenLong-Run Costs and Output DecisionsBintang RainNoch keine Bewertungen

- Ch08 - Long Run Costs and Output DecisionsDokument38 SeitenCh08 - Long Run Costs and Output DecisionsPRATAMA ADI SUGANDA UINJKTNoch keine Bewertungen

- Ch08Dokument38 SeitenCh08Aisha AzamNoch keine Bewertungen

- Long-Run Costs and Output DecisionsDokument38 SeitenLong-Run Costs and Output DecisionsSer MacikoiNoch keine Bewertungen

- Case & Fair: Chapter 8: Short-Run Costs and Output DecisionsDokument31 SeitenCase & Fair: Chapter 8: Short-Run Costs and Output DecisionsManepalli YashwinNoch keine Bewertungen

- Short-Run Costs and Output Decisions: Fernando & Yvonn QuijanoDokument31 SeitenShort-Run Costs and Output Decisions: Fernando & Yvonn QuijanoCharles Reginald K. HwangNoch keine Bewertungen

- CFO POE12 PPT 08Dokument41 SeitenCFO POE12 PPT 08Batuhan GyulerNoch keine Bewertungen

- Fundamental Cost Concepts: (Part 2)Dokument30 SeitenFundamental Cost Concepts: (Part 2)amirulNoch keine Bewertungen

- Ch06Dokument23 SeitenCh06Aisha AzamNoch keine Bewertungen

- 02 CVP HandoutDokument23 Seiten02 CVP HandoutRishika RathiNoch keine Bewertungen

- Chapter 4 - Costs of Production - AllDokument29 SeitenChapter 4 - Costs of Production - AllNetsanet MeleseNoch keine Bewertungen

- Introduction to Economics: Short and Long Run Costs (Econ. 101Dokument31 SeitenIntroduction to Economics: Short and Long Run Costs (Econ. 101Nahom MasreshaNoch keine Bewertungen

- HL TOF 1 Costs Revenues and ProfitsDokument127 SeitenHL TOF 1 Costs Revenues and ProfitsDamir JovicNoch keine Bewertungen

- Chapter 4 - Costs of Production-1Dokument42 SeitenChapter 4 - Costs of Production-1idolhevevNoch keine Bewertungen

- Chapter Four: Supply I: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong UniversityDokument27 SeitenChapter Four: Supply I: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong Universitymaria rafiqNoch keine Bewertungen

- Chapter 5 Costs and ProductionDokument27 SeitenChapter 5 Costs and ProductionChen Yee KhooNoch keine Bewertungen

- Reviewer in Man Eco Finals 1ST SemDokument11 SeitenReviewer in Man Eco Finals 1ST SemZoomkada BhieNoch keine Bewertungen

- Theory of Cost: Slides by Pamela L. Hall Western Washington UniversityDokument28 SeitenTheory of Cost: Slides by Pamela L. Hall Western Washington UniversityKristyl CernaNoch keine Bewertungen

- Principles of Microeconomics: Twelfth Edition, Global EditionDokument37 SeitenPrinciples of Microeconomics: Twelfth Edition, Global EditionmmNoch keine Bewertungen

- Inventory Control Models: EPL ModelDokument25 SeitenInventory Control Models: EPL ModeldarmianaNoch keine Bewertungen

- C5 MicroEcoDokument11 SeitenC5 MicroEcoShashwat JhaNoch keine Bewertungen

- ECO6201 - Chapter 5 - Production and Cost Analysis in The Short Run (Amended)Dokument36 SeitenECO6201 - Chapter 5 - Production and Cost Analysis in The Short Run (Amended)Thomas WuNoch keine Bewertungen

- CH 09 - Input Demand - Labor and LandDokument31 SeitenCH 09 - Input Demand - Labor and LandArjun NeekhraNoch keine Bewertungen

- 2024 - Level 1 - Economics - Slide (1)Dokument42 Seiten2024 - Level 1 - Economics - Slide (1)k60.2113340007Noch keine Bewertungen

- Lesson 4 ProductionDokument49 SeitenLesson 4 ProductionScriptedNoch keine Bewertungen

- MAS 9204 Product Costing Activity-Based Costing (ABC)Dokument19 SeitenMAS 9204 Product Costing Activity-Based Costing (ABC)Mila Casandra CastañedaNoch keine Bewertungen

- ch09 - Cost Theory ApplicationsDokument21 Seitench09 - Cost Theory ApplicationsWilliam DC RiveraNoch keine Bewertungen

- Econ 101 Intro to Short and Long Run Cost CurvesDokument27 SeitenEcon 101 Intro to Short and Long Run Cost CurvesAli HassenNoch keine Bewertungen

- Finance T3 2017 - w9Dokument45 SeitenFinance T3 2017 - w9aabubNoch keine Bewertungen

- Ch09Dokument29 SeitenCh09Aisha AzamNoch keine Bewertungen

- 203 - Engineering Eco 1 - IntroductionDokument21 Seiten203 - Engineering Eco 1 - IntroductionNPCNoch keine Bewertungen

- Econ - Unit - 5 - Cost TheoryDokument39 SeitenEcon - Unit - 5 - Cost TheorySampurnaa DasNoch keine Bewertungen

- ME Session 13 Cost Concepts (1) .PPTMDokument51 SeitenME Session 13 Cost Concepts (1) .PPTMAnushka ChokseNoch keine Bewertungen

- Cost Evaluation StudyDokument29 SeitenCost Evaluation StudyMo ZeroNoch keine Bewertungen

- 012721-Syn4-Ch 7 - The Theory of Estimation of CostDokument21 Seiten012721-Syn4-Ch 7 - The Theory of Estimation of CostYani RahmaNoch keine Bewertungen

- 1 Lecture 6 - Short-Run Costs and Output DecisionsDokument14 Seiten1 Lecture 6 - Short-Run Costs and Output DecisionsyasirNoch keine Bewertungen

- Module 6Dokument25 SeitenModule 6prabodhNoch keine Bewertungen

- D - Absorption and Variable CostingDokument5 SeitenD - Absorption and Variable Costingian dizonNoch keine Bewertungen

- Time Value of Money: Production and Operations Management - R B Khanna © Prentice Hall IndiaDokument130 SeitenTime Value of Money: Production and Operations Management - R B Khanna © Prentice Hall IndiararaNoch keine Bewertungen

- Analysis of Costs: Cost Function Cost FunctionDokument10 SeitenAnalysis of Costs: Cost Function Cost Functionkanv gulatiNoch keine Bewertungen

- Bilaspur University presentation on managerial economics cost theoryDokument22 SeitenBilaspur University presentation on managerial economics cost theoryVi Pin SinghNoch keine Bewertungen

- Principles of Economics: Global EditionDokument43 SeitenPrinciples of Economics: Global EditionErsin TukenmezNoch keine Bewertungen

- Breakeven Analysis: Engineering EconomyDokument10 SeitenBreakeven Analysis: Engineering EconomyChakshu KapoorNoch keine Bewertungen

- CH 4 PPT PresentationDokument22 SeitenCH 4 PPT PresentationNigus AyeleNoch keine Bewertungen

- Topik 5Dokument64 SeitenTopik 5Nur Niesha AthirahNoch keine Bewertungen

- Mas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsDokument3 SeitenMas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsClyde RamosNoch keine Bewertungen

- 4 Productionandcost 121207091754 Phpapp02Dokument23 Seiten4 Productionandcost 121207091754 Phpapp02Daffa HanifNoch keine Bewertungen

- Case Econ08 PPT 09Dokument36 SeitenCase Econ08 PPT 09Kristin Alice PonienteNoch keine Bewertungen

- Finman Session6bDokument71 SeitenFinman Session6bLovely CabardoNoch keine Bewertungen

- CH 03Dokument65 SeitenCH 03ahmadhidrNoch keine Bewertungen

- CH 04Dokument55 SeitenCH 04ahmadhidrNoch keine Bewertungen

- CH 02Dokument46 SeitenCH 02ahmadhidrNoch keine Bewertungen

- CH 05Dokument67 SeitenCH 05EvaNoch keine Bewertungen

- Open Economy Macroeconomics The Balance of Payments and Exchange RatesDokument36 SeitenOpen Economy Macroeconomics The Balance of Payments and Exchange RatesMr.BrewokNoch keine Bewertungen

- CH 28Dokument27 SeitenCH 28forensic accNoch keine Bewertungen

- Open Economy Macroeconomics The Balance of Payments and Exchange RatesDokument36 SeitenOpen Economy Macroeconomics The Balance of Payments and Exchange RatesMr.BrewokNoch keine Bewertungen

- CH 32Dokument34 SeitenCH 32forensic accNoch keine Bewertungen

- Household and Firm Behavior in The Macroeconomy: A Further LookDokument41 SeitenHousehold and Firm Behavior in The Macroeconomy: A Further Lookforensic accNoch keine Bewertungen

- CH 01Dokument61 SeitenCH 01orxan205Noch keine Bewertungen

- Principles of Economics Chapter 18Dokument24 SeitenPrinciples of Economics Chapter 18Louie Guese ManguneNoch keine Bewertungen

- International Trade, Comparative Advantage, and ProtectionismDokument36 SeitenInternational Trade, Comparative Advantage, and Protectionismforensic accNoch keine Bewertungen

- CH 26Dokument36 SeitenCH 26EvaNoch keine Bewertungen

- Money Demand, The Equilibrium Interest Rate, and Monetary PolicyDokument21 SeitenMoney Demand, The Equilibrium Interest Rate, and Monetary PolicyEvaNoch keine Bewertungen

- Aggregate Demand, Aggregate Supply, and InflationDokument34 SeitenAggregate Demand, Aggregate Supply, and Inflationforensic accNoch keine Bewertungen

- CH 23Dokument24 SeitenCH 23forensic accNoch keine Bewertungen

- Externalities, Public Goods, Imperfect Information, and Social ChoiceDokument33 SeitenExternalities, Public Goods, Imperfect Information, and Social ChoiceEvaNoch keine Bewertungen

- The Labor Market, Unemployment, and InflationDokument29 SeitenThe Labor Market, Unemployment, and Inflationforensic accNoch keine Bewertungen

- CH 19Dokument30 SeitenCH 19forensic accNoch keine Bewertungen

- CH 21Dokument35 SeitenCH 21EvaNoch keine Bewertungen

- Money Demand, The Equilibrium Interest Rate, and Monetary PolicyDokument21 SeitenMoney Demand, The Equilibrium Interest Rate, and Monetary PolicyEvaNoch keine Bewertungen

- CH 15Dokument33 SeitenCH 15EvaNoch keine Bewertungen

- Monopolistic Competition and OligopolyDokument38 SeitenMonopolistic Competition and Oligopolymidori_06Noch keine Bewertungen

- The Government and Fiscal PolicyDokument30 SeitenThe Government and Fiscal Policyforensic accNoch keine Bewertungen

- CH 19Dokument30 SeitenCH 19forensic accNoch keine Bewertungen

- CH 05Dokument27 SeitenCH 05msohailtahirNoch keine Bewertungen

- Principles of Economics Chapter 6Dokument38 SeitenPrinciples of Economics Chapter 6Louie Guese ManguneNoch keine Bewertungen

- Monopoly and Antitrust PolicyDokument35 SeitenMonopoly and Antitrust PolicyEvaNoch keine Bewertungen

- Monopolistic Competition and OligopolyDokument38 SeitenMonopolistic Competition and Oligopolymidori_06Noch keine Bewertungen

- Ch11 General Equilibrium and The Efficiency of Perfect CompetitionDokument22 SeitenCh11 General Equilibrium and The Efficiency of Perfect CompetitionfirebirdshockwaveNoch keine Bewertungen

- Auditing and Assurance Services 15th Edition Arens Solutions ManualDokument23 SeitenAuditing and Assurance Services 15th Edition Arens Solutions Manualfidelmaalexandranbj100% (32)

- Erp 2017 Studyguide FinalDokument20 SeitenErp 2017 Studyguide Finalken_ng333Noch keine Bewertungen

- The Product Life CycleDokument8 SeitenThe Product Life CycleMandvi YadavNoch keine Bewertungen

- Practice Final Bus331 Spring2023Dokument2 SeitenPractice Final Bus331 Spring2023Javan OdephNoch keine Bewertungen

- Vertical Integration in Apparel IndustryDokument15 SeitenVertical Integration in Apparel IndustryAyushi ShuklaNoch keine Bewertungen

- Arvind Fashions Limited: Investor RoadshowDokument39 SeitenArvind Fashions Limited: Investor RoadshowdeepurNoch keine Bewertungen

- Presented by Minal Neswankar Jivika Thakur Preeti WaghmodeDokument21 SeitenPresented by Minal Neswankar Jivika Thakur Preeti WaghmodeJivika ThakurNoch keine Bewertungen

- Buyers' Cartels An Empirical Study of Prevalence and Economic CharacteristicsDokument48 SeitenBuyers' Cartels An Empirical Study of Prevalence and Economic CharacteristicsmgNoch keine Bewertungen

- Rectified Business Project PDFDokument8 SeitenRectified Business Project PDFPrem Kumar KarnNoch keine Bewertungen

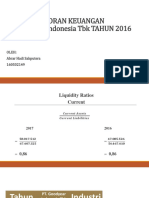

- Analisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Dokument34 SeitenAnalisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Tri AmbarNoch keine Bewertungen

- University of California PE and VC IRR ReturnsDokument5 SeitenUniversity of California PE and VC IRR Returnsdavidsun1988Noch keine Bewertungen

- Chapter 15 - Solution ManualDokument13 SeitenChapter 15 - Solution ManualjuanNoch keine Bewertungen

- PetMeds Analysis 2Dokument10 SeitenPetMeds Analysis 2Марго КоваленкоNoch keine Bewertungen

- Prelims QuestionsDokument2 SeitenPrelims QuestionsPushpendra SinghNoch keine Bewertungen

- Table - 23-7: Schedule 1g: Ending Inventories Budget, First Quarter, 20XXDokument4 SeitenTable - 23-7: Schedule 1g: Ending Inventories Budget, First Quarter, 20XXeahpotNoch keine Bewertungen

- Strategic AllianceDokument12 SeitenStrategic AllianceMadhura GiraseNoch keine Bewertungen

- 23 W Group 8 Final Project CapstoneDokument14 Seiten23 W Group 8 Final Project CapstoneQwertNoch keine Bewertungen

- 5 Replacement StudiesDokument31 Seiten5 Replacement StudiesAngel NaldoNoch keine Bewertungen

- Practice 2Dokument24 SeitenPractice 2Софи БреславецNoch keine Bewertungen

- Property Inventory: Msu-Iit National Multi-Purpose CooperativeDokument4 SeitenProperty Inventory: Msu-Iit National Multi-Purpose CooperativeNestorJepolanCapiña100% (1)

- Chapter 13 - Audit Property, Plant and EquipmentDokument21 SeitenChapter 13 - Audit Property, Plant and EquipmentEarl Lalaine EscolNoch keine Bewertungen

- 3 AccountingDokument39 Seiten3 AccountingSaltanat ShamovaNoch keine Bewertungen

- Motilal Oswal Finance Services IPO Note Aug 07 EDELDokument17 SeitenMotilal Oswal Finance Services IPO Note Aug 07 EDELKunal Maheshwari100% (1)

- Sticker MonitorDokument21 SeitenSticker MonitorRestia SchleiferNoch keine Bewertungen