Das könnte Ihnen auch gefallen

- Pre-Session Seal 1 (2022-2023) Student E-BookDokument6 SeitenPre-Session Seal 1 (2022-2023) Student E-BookMicah Danielle S. TORMONNoch keine Bewertungen

- The Role of Financial InstitutionsDokument8 SeitenThe Role of Financial InstitutionsΚωνσταντίνος ΑμπατζήςNoch keine Bewertungen

- Book Review On Fides Et RatioDokument3 SeitenBook Review On Fides Et RatioLuca InfantinoNoch keine Bewertungen

- Mileage Reimbursement PolicyDokument3 SeitenMileage Reimbursement PolicyF. Nathan RufferNoch keine Bewertungen

- Fides Et RatioDokument19 SeitenFides Et Ratiosuiter944Noch keine Bewertungen

- Importance of Personal Physical AppearanceDokument5 SeitenImportance of Personal Physical Appearancerajnarayanrock100% (1)

- Faith and ReasonDokument64 SeitenFaith and ReasonCopila AlexandraNoch keine Bewertungen

- Think Outside The BoxDokument25 SeitenThink Outside The BoxNoor ZafarNoch keine Bewertungen

- Introduction To Engineering EconomyDokument15 SeitenIntroduction To Engineering EconomyKetut PujaNoch keine Bewertungen

- PADD Loan Calculator Tool: Payment Amount (Annually) : $ 556,927.71Dokument1 SeitePADD Loan Calculator Tool: Payment Amount (Annually) : $ 556,927.71sureshstipl sureshNoch keine Bewertungen

- Sample Financial PlanDokument12 SeitenSample Financial PlanSneha KhuranaNoch keine Bewertungen

- CHAP - 03 - Managing and Pricing Deposit ServicesDokument60 SeitenCHAP - 03 - Managing and Pricing Deposit ServicesTran Thanh NganNoch keine Bewertungen

- TTF Engecon ch4Dokument9 SeitenTTF Engecon ch4Tewelde WorkuNoch keine Bewertungen

- Board of Directors Jim Walter Interbay Unit May 13, 2010: AgendaDokument7 SeitenBoard of Directors Jim Walter Interbay Unit May 13, 2010: AgendaBrendaBrowningNoch keine Bewertungen

- Motorcycle LoanDokument10 SeitenMotorcycle Loanrowilson reyNoch keine Bewertungen

- Board of Directors Steinbrenner Family West Tampa Boys & Girls Club May 12, 2011Dokument5 SeitenBoard of Directors Steinbrenner Family West Tampa Boys & Girls Club May 12, 2011BrendaBrowningNoch keine Bewertungen

- Lesson Guide 2.2 Beware of Banking FeesDokument4 SeitenLesson Guide 2.2 Beware of Banking FeesKent TiclavilcaNoch keine Bewertungen

- Impact, Hope & OpportunityDokument6 SeitenImpact, Hope & OpportunityBrendaBrowningNoch keine Bewertungen

- Financial Literacy: Knowing What You Need To Know To Achieve Your Financial GoalsDokument24 SeitenFinancial Literacy: Knowing What You Need To Know To Achieve Your Financial GoalsSean BoesNoch keine Bewertungen

- APR CalculatorDokument1 SeiteAPR Calculatorcalebrussell.cmNoch keine Bewertungen

- Impact, Hope & OpportunityDokument6 SeitenImpact, Hope & OpportunityBrendaBrowningNoch keine Bewertungen

- Bonds Payable and Investments in Bonds: Financial and Managerial Accounting 8th Edition Warren Reeve FessDokument49 SeitenBonds Payable and Investments in Bonds: Financial and Managerial Accounting 8th Edition Warren Reeve FessCOURAGEOUSNoch keine Bewertungen

- GE1202 Managing Your Personal Finance: Consumer Credits and LoansDokument39 SeitenGE1202 Managing Your Personal Finance: Consumer Credits and LoansAiden LANNoch keine Bewertungen

- 03-M2 Personal Finance SpreadsheetDokument20 Seiten03-M2 Personal Finance SpreadsheetAtlass StoreNoch keine Bewertungen

- Credit and CollectionDokument17 SeitenCredit and CollectionDia Cessianne VillarolaNoch keine Bewertungen

- Your Reverse Mortgage Summary: You Could GetDokument11 SeitenYour Reverse Mortgage Summary: You Could GetPete Santilli100% (1)

- Ten Principles of Personal Financial LiteracyDokument20 SeitenTen Principles of Personal Financial LiteracyARCHEL ORASANoch keine Bewertungen

- December 10th AttachmentsDokument6 SeitenDecember 10th AttachmentsbgctampaNoch keine Bewertungen

- CFS 7 Intro FPW PPT 1220E1R1Dokument26 SeitenCFS 7 Intro FPW PPT 1220E1R1KEHKASHAN NIZAMNoch keine Bewertungen

- Personal Finance For Canadians 9th Edition Currie Solutions ManualDokument9 SeitenPersonal Finance For Canadians 9th Edition Currie Solutions ManualLesterBriggssNoch keine Bewertungen

- Project 6Dokument10 SeitenProject 6api-489150270Noch keine Bewertungen

- Payment Information Account Summary: March 9 20Dokument3 SeitenPayment Information Account Summary: March 9 20Mark Williams100% (2)

- Financial Management Assignment 1Dokument3 SeitenFinancial Management Assignment 12K22DMBA67 kushankNoch keine Bewertungen

- Cash and Liquidity ManagementDokument27 SeitenCash and Liquidity ManagementgagafikNoch keine Bewertungen

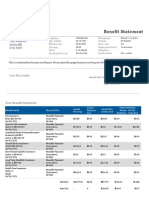

- Benefit Statement: Test Retro 62 Test Address Noida, MB D1D 4S25Dokument3 SeitenBenefit Statement: Test Retro 62 Test Address Noida, MB D1D 4S25007shivangNoch keine Bewertungen

- Stephen Antonioni's Net Worth TableDokument15 SeitenStephen Antonioni's Net Worth TableAbdelrahman ElkadyNoch keine Bewertungen

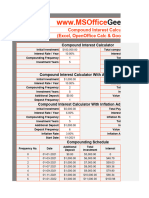

- Compound Interest CalculatorDokument14 SeitenCompound Interest CalculatorSiyabongaNoch keine Bewertungen

- Currency Risk ManagementDokument52 SeitenCurrency Risk ManagementWatan YarNoch keine Bewertungen

- Dang Thuy Huong - 1704040049 - HW Tut 6Dokument19 SeitenDang Thuy Huong - 1704040049 - HW Tut 6Đặng Thuỳ HươngNoch keine Bewertungen

- What Is Leveraged Buyout Model Aka LBO Model?Dokument5 SeitenWhat Is Leveraged Buyout Model Aka LBO Model?bhumiklalka999Noch keine Bewertungen

- HouseDokument14 SeitenHouseapi-435614969Noch keine Bewertungen

- ExportDokument3 SeitenExportToby100% (1)

- Financial Plan: 7.1 Break-Even AnalysisDokument41 SeitenFinancial Plan: 7.1 Break-Even AnalysisnahidasumbalsundasNoch keine Bewertungen

- Summary of Accounts: Contacting UsDokument3 SeitenSummary of Accounts: Contacting Uskogip44817Noch keine Bewertungen

- Mortgage Calculator: Karl Jeacle'sDokument1 SeiteMortgage Calculator: Karl Jeacle'sScott SweeneyNoch keine Bewertungen

- Cash ManagementDokument48 SeitenCash ManagementThabo.GombaNoch keine Bewertungen

- Relationship Summary:: MR John Doe 2 Post Alley, SEATTLE, WA 98101Dokument6 SeitenRelationship Summary:: MR John Doe 2 Post Alley, SEATTLE, WA 98101Zheng YangNoch keine Bewertungen

- Final Financial Plan Kelsey HarrisonDokument7 SeitenFinal Financial Plan Kelsey Harrisonapi-316949889Noch keine Bewertungen

- Homepo NTDokument1 SeiteHomepo NTMissa RoseNoch keine Bewertungen

- Topic 7 Cash Management & ControlDokument25 SeitenTopic 7 Cash Management & ControlMd Jahid HossainNoch keine Bewertungen

- Case Spreadsheet NewDokument6 SeitenCase Spreadsheet NewUsman Ch0% (2)

- Financial Literacy-Middle School 13-PresenationDokument31 SeitenFinancial Literacy-Middle School 13-PresenationRodel floresNoch keine Bewertungen

- Project 6Dokument16 SeitenProject 6api-461500596Noch keine Bewertungen

- Project 6 - Future and Present ValueDokument5 SeitenProject 6 - Future and Present Valueapi-666269710Noch keine Bewertungen

- Module 3B - ACCCOB2 - Receivables - PPT FHVDokument46 SeitenModule 3B - ACCCOB2 - Receivables - PPT FHVCale Robert RascoNoch keine Bewertungen

- ClassSession 20 - Bonds - HandoutsDokument22 SeitenClassSession 20 - Bonds - Handoutsdrey baxterNoch keine Bewertungen

- Lesson 3. TVM 2020Dokument25 SeitenLesson 3. TVM 2020Vĩ NguyễnNoch keine Bewertungen

- WellsFargoDokument5 SeitenWellsFargoUsm amNoch keine Bewertungen

- LM02 Fixed-Income Cash Flows and Types IFT NotesDokument13 SeitenLM02 Fixed-Income Cash Flows and Types IFT NotesClaptrapjackNoch keine Bewertungen

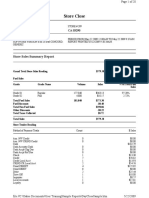

- Store Close: Store Sales Summary ReportDokument20 SeitenStore Close: Store Sales Summary ReportJimmyNoch keine Bewertungen

- In-Wash Scent Boosters A Game Changer For Laundry CareDokument59 SeitenIn-Wash Scent Boosters A Game Changer For Laundry CareSwati JainNoch keine Bewertungen

- Abraham's Strategy: Split StealDokument6 SeitenAbraham's Strategy: Split StealSwati JainNoch keine Bewertungen

- Mergers and Acquisitions: Case: Cooper Industries. Inc. 1Dokument12 SeitenMergers and Acquisitions: Case: Cooper Industries. Inc. 1Swati JainNoch keine Bewertungen

- Mergers and Acquisitions: Case: Cooper Industries. Inc. 1Dokument12 SeitenMergers and Acquisitions: Case: Cooper Industries. Inc. 1Swati JainNoch keine Bewertungen

- Sangam Registration FormDokument1 SeiteSangam Registration FormSwati JainNoch keine Bewertungen

- Mahindra Launches The Xylo D2 With Mdi Crde EngineDokument4 SeitenMahindra Launches The Xylo D2 With Mdi Crde EngineSwati JainNoch keine Bewertungen

- Etf Gold VS E-GoldDokument22 SeitenEtf Gold VS E-GoldRia ShayNoch keine Bewertungen

- Chapter 03Dokument13 SeitenChapter 03ClaraNoch keine Bewertungen

- Payroll Summary For The Month of AugustDokument46 SeitenPayroll Summary For The Month of AugustAida MohammedNoch keine Bewertungen

- Vinati OrganicsDokument6 SeitenVinati OrganicsNeha NehaNoch keine Bewertungen

- A Company Is An Artificial Person Created by LawDokument5 SeitenA Company Is An Artificial Person Created by LawNeelabhNoch keine Bewertungen

- Universiti Teknologi Mara Common Test 1: Confidential 1 TEST1/NOV2017/FAR210Dokument4 SeitenUniversiti Teknologi Mara Common Test 1: Confidential 1 TEST1/NOV2017/FAR210shahrinNoch keine Bewertungen

- FICA Configuration Step by Step - SAP Expertise Consulting PDFDokument35 SeitenFICA Configuration Step by Step - SAP Expertise Consulting PDFsrinivaspanchakarla50% (6)

- Nike CaseDokument10 SeitenNike CaseDanielle Saavedra0% (1)

- Accounting STDDokument168 SeitenAccounting STDChandra ShekharNoch keine Bewertungen

- Free Credit Score and Report - Free Monthly Credit CheckDokument3 SeitenFree Credit Score and Report - Free Monthly Credit CheckSagar Chandra KhatuaNoch keine Bewertungen

- Commerce Class 12 Semester2Dokument31 SeitenCommerce Class 12 Semester2Tesmon MathewNoch keine Bewertungen

- TCDN Clc63d - Peony Coffee-V1Dokument4 SeitenTCDN Clc63d - Peony Coffee-V111219775Noch keine Bewertungen

- H HJ KJHKJDokument15 SeitenH HJ KJHKJEmmanuel BatinganNoch keine Bewertungen

- Summary Account Payable Statement: JiopayDokument2 SeitenSummary Account Payable Statement: Jiopaykamalkant.jaipurNoch keine Bewertungen

- U.S. Individual Income Tax Return: Filing StatusDokument14 SeitenU.S. Individual Income Tax Return: Filing StatusDavid Dautel100% (1)

- Role of Financial Market and Securities Market in Economic GrowthDokument2 SeitenRole of Financial Market and Securities Market in Economic GrowthAparna Rajasekharan100% (1)

- How To Secure BIR Importer Clearance CertificateDokument6 SeitenHow To Secure BIR Importer Clearance CertificateEmely SolonNoch keine Bewertungen

- Assignment On Analysis of Annual Report ofDokument9 SeitenAssignment On Analysis of Annual Report oflalagopgapangamdas100% (1)

- Presentation On Business Icon: by Ankita Sthapak Roll No.57Dokument9 SeitenPresentation On Business Icon: by Ankita Sthapak Roll No.57Ankita SthapakNoch keine Bewertungen

- Accounting Grade 9: Balance SheetDokument2 SeitenAccounting Grade 9: Balance SheetSimthandile NosihleNoch keine Bewertungen

- Trust Accounts Full NotesDokument8 SeitenTrust Accounts Full NotesRuth Nyawira100% (1)

- CFAS Quiz Questions AddedDokument2 SeitenCFAS Quiz Questions AddedSaeym SegoviaNoch keine Bewertungen

- Executive Assistant Office Manager in Washington DC Resume Jane GiordanoDokument2 SeitenExecutive Assistant Office Manager in Washington DC Resume Jane GiordanoJaneGiordanoNoch keine Bewertungen

- SamCERA PE Perf Report Q1 20 SolovisDokument1 SeiteSamCERA PE Perf Report Q1 20 SolovisdavidtollNoch keine Bewertungen

- MBA Syllabus 21-08-2020 FinalDokument160 SeitenMBA Syllabus 21-08-2020 Finalgundarapu deepika0% (1)

- The Mystery of Zero-Leverage Firms: - An Empirical Study On Chinese Public FirmsDokument33 SeitenThe Mystery of Zero-Leverage Firms: - An Empirical Study On Chinese Public FirmsKunal MeenaNoch keine Bewertungen

- 3 - 01 - 10 - Appendix L - Letter of RepresentationDokument4 Seiten3 - 01 - 10 - Appendix L - Letter of RepresentationHariprasad B RNoch keine Bewertungen

- Ch.2 Accounting For Bonus and Right IssueDokument12 SeitenCh.2 Accounting For Bonus and Right IssueAmrit SarkarNoch keine Bewertungen

- M4 Ra 10365Dokument8 SeitenM4 Ra 10365julia4razoNoch keine Bewertungen

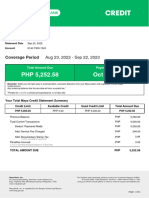

- MayaCredit SoA 2023SEPDokument3 SeitenMayaCredit SoA 2023SEPjepoy palaruanNoch keine Bewertungen