Das könnte Ihnen auch gefallen

- Hein Technologies Conducted The Following Cash Transactions On JanuaryDokument1 SeiteHein Technologies Conducted The Following Cash Transactions On JanuaryTaimur TechnologistNoch keine Bewertungen

- Conceptual Frame Work QBDokument15 SeitenConceptual Frame Work QBnanthini nanthini100% (1)

- Midterm Exams ReviewDokument5 SeitenMidterm Exams ReviewJeanette LampitocNoch keine Bewertungen

- XH-H 3e PPT Chap05Dokument69 SeitenXH-H 3e PPT Chap05An NhiênNoch keine Bewertungen

- Đề Bài Đáp Án: Which of the following are examples of non-financial performance indicators? Select ALL that may applyDokument11 SeitenĐề Bài Đáp Án: Which of the following are examples of non-financial performance indicators? Select ALL that may applyDANH LÊ VĂNNoch keine Bewertungen

- MANACCDokument3 SeitenMANACCminseok kimNoch keine Bewertungen

- T1 - KMLT 2015 - ThanhDokument35 SeitenT1 - KMLT 2015 - ThanhCavipsotNoch keine Bewertungen

- Chapter 11&12 QuestionsDokument8 SeitenChapter 11&12 QuestionsMya B. Walker100% (1)

- Quizzes - Topic 4 - Xem L I Bài LàmDokument4 SeitenQuizzes - Topic 4 - Xem L I Bài LàmHải YếnNoch keine Bewertungen

- Accounting Policies, Changes in Accounting Estimates and ErrorsDokument48 SeitenAccounting Policies, Changes in Accounting Estimates and ErrorsHồ Đan ThụcNoch keine Bewertungen

- Financial Analysis - HomeworkDokument7 SeitenFinancial Analysis - HomeworkTuan Anh LeeNoch keine Bewertungen

- Introduction To Transaction ProcessingDokument23 SeitenIntroduction To Transaction ProcessingAngel Cauilan100% (1)

- App ADokument92 SeitenApp AMohammadYaqoob100% (1)

- Auditing in Cis Prelim Exam Raquel Alvarez-De Castro, Cpa, Mba/Mpa I.QuestionsDokument3 SeitenAuditing in Cis Prelim Exam Raquel Alvarez-De Castro, Cpa, Mba/Mpa I.QuestionsWenjunNoch keine Bewertungen

- Final Exam, s1, 2019 FINALDokument12 SeitenFinal Exam, s1, 2019 FINALShivneel NaiduNoch keine Bewertungen

- Corporate ReportingDokument24 SeitenCorporate ReportingAnjali RajendranNoch keine Bewertungen

- Workshop F2 May 2011Dokument18 SeitenWorkshop F2 May 2011roukaiya_peerkhanNoch keine Bewertungen

- QuestionsDokument5 SeitenQuestionsYonas100% (1)

- Chapter 13 Share-Based Payments 2Dokument9 SeitenChapter 13 Share-Based Payments 2Thalia Rhine AberteNoch keine Bewertungen

- IAS 20 Accounting For Government Grants and Disclosure of Government AssistanceDokument5 SeitenIAS 20 Accounting For Government Grants and Disclosure of Government Assistancemanvi jainNoch keine Bewertungen

- N. Title Location: List of Examples IFRS 15 Revenue From Contracts With CustomersDokument27 SeitenN. Title Location: List of Examples IFRS 15 Revenue From Contracts With CustomersHồ Đan ThụcNoch keine Bewertungen

- Practice Questions: Global Certified Management AccountantDokument23 SeitenPractice Questions: Global Certified Management AccountantThiha WinNoch keine Bewertungen

- Financial Instruments: Class 6Dokument6 SeitenFinancial Instruments: Class 6KristenNoch keine Bewertungen

- K17405CA Assignment Kim Huong and Nhu ThuanDokument25 SeitenK17405CA Assignment Kim Huong and Nhu Thuanthuylinh voNoch keine Bewertungen

- Answer: B: Cf-Multiple Choice Questions (1) - Thuhien-UehDokument5 SeitenAnswer: B: Cf-Multiple Choice Questions (1) - Thuhien-UehMinh Phạm100% (1)

- luyện tập IFRSDokument6 Seitenluyện tập IFRSÁnh Nguyễn Thị NgọcNoch keine Bewertungen

- Bài kiểm tra trắc nghiệm chủ đề - Công cụ tài chính - - Xem lại bài làmDokument11 SeitenBài kiểm tra trắc nghiệm chủ đề - Công cụ tài chính - - Xem lại bài làmAh TuanNoch keine Bewertungen

- Evaluation of Misstatements Identified During The Audit: Risk Management & Audit-ICMAP 1Dokument18 SeitenEvaluation of Misstatements Identified During The Audit: Risk Management & Audit-ICMAP 1mrizwan84Noch keine Bewertungen

- AIS10Dokument4 SeitenAIS10XiaoMeiMei100% (1)

- Baitap C1 HVDokument8 SeitenBaitap C1 HVThanh ThảoNoch keine Bewertungen

- BT kế toán quốc tếDokument58 SeitenBT kế toán quốc tếUyên Nguyễn Hoàng ThanhNoch keine Bewertungen

- Chuẩn mực KTQTDokument24 SeitenChuẩn mực KTQTChi PhươngNoch keine Bewertungen

- IAS 16 Property Plant EquipmentDokument4 SeitenIAS 16 Property Plant EquipmentMD Hafizul Islam HafizNoch keine Bewertungen

- Ntjca/Edit Ynd6Pnm/Edit: TN KTCB (Eng)Dokument97 SeitenNtjca/Edit Ynd6Pnm/Edit: TN KTCB (Eng)My Nguyễn TràNoch keine Bewertungen

- Job, Batch and Service CostingDokument22 SeitenJob, Batch and Service CostingSanjeev JayaratnaNoch keine Bewertungen

- Advanced Accounting Test Bank Chapter 07 Susan Hamlen PDFDokument60 SeitenAdvanced Accounting Test Bank Chapter 07 Susan Hamlen PDFsamuel debebeNoch keine Bewertungen

- 04 Objective Type Financial Instruments B15Dokument4 Seiten04 Objective Type Financial Instruments B15Huỳnh Minh Gia HàoNoch keine Bewertungen

- E. All of The Above. A. Total Revenue Equals Total CostDokument22 SeitenE. All of The Above. A. Total Revenue Equals Total CostNicole KimNoch keine Bewertungen

- My Proposal ReaserchDokument24 SeitenMy Proposal ReaserchAbdulhamid MustefaNoch keine Bewertungen

- F6 Midterm Test QuestionDokument11 SeitenF6 Midterm Test QuestionChippu AnhNoch keine Bewertungen

- Management Accounting HWDokument5 SeitenManagement Accounting HWHw SolutionNoch keine Bewertungen

- B5: Problem Solving: P.O.Box 10378 Mwanza-TanzaniaDokument9 SeitenB5: Problem Solving: P.O.Box 10378 Mwanza-TanzaniaSHWAIBU SELLANoch keine Bewertungen

- Assignment 1 - Chapter 2Dokument6 SeitenAssignment 1 - Chapter 2Ho Thi Phuong ThaoNoch keine Bewertungen

- Audit of PPE Case StudyDokument1 SeiteAudit of PPE Case Studyvenice cambryNoch keine Bewertungen

- SIA Problem 7Dokument4 SeitenSIA Problem 7Gain GainNoch keine Bewertungen

- Individual Assignment v1Dokument4 SeitenIndividual Assignment v1Vie TrầnNoch keine Bewertungen

- Solutions To Review Exam Papers 1 To 3Dokument171 SeitenSolutions To Review Exam Papers 1 To 3Roi NyanNoch keine Bewertungen

- Standard Unmodified Auditor ReportDokument3 SeitenStandard Unmodified Auditor ReportRiz WanNoch keine Bewertungen

- Tasks Group AccountingDokument11 SeitenTasks Group Accountingduchieu2k32k3100% (1)

- Intangible MCDokument49 SeitenIntangible MCAnonymous zpUO2SNoch keine Bewertungen

- Chapter 13A Review GuideDokument7 SeitenChapter 13A Review GuideNirali PatelNoch keine Bewertungen

- Session 6 - Process Costing: Multiple ChoiceDokument10 SeitenSession 6 - Process Costing: Multiple Choiceatty lesNoch keine Bewertungen

- Econ 3a Midterm 1 WorksheetDokument21 SeitenEcon 3a Midterm 1 WorksheetZyania LizarragaNoch keine Bewertungen

- Quiz 1 AnswersDokument6 SeitenQuiz 1 AnswersAlyssa CasimiroNoch keine Bewertungen

- IAS 02: Inventories: Requirement: SolutionDokument2 SeitenIAS 02: Inventories: Requirement: SolutionMD Hafizul Islam Hafiz100% (1)

- F8 Workbook Questions & Solutions 1.1 PDFDokument188 SeitenF8 Workbook Questions & Solutions 1.1 PDFLinkon PeterNoch keine Bewertungen

- Multiple Choice Questions Accounting PoliciesDokument4 SeitenMultiple Choice Questions Accounting PoliciesUy Uy ChoiceNoch keine Bewertungen

- Lecture Week 4Dokument48 SeitenLecture Week 4朱潇妤Noch keine Bewertungen

- Intangibles: ACC/ACF3100 Advanced Financial AccountingDokument42 SeitenIntangibles: ACC/ACF3100 Advanced Financial Accountingharoon nasirNoch keine Bewertungen

- SBRIAS38 TutorSlidesDokument27 SeitenSBRIAS38 TutorSlidesDipesh MagratiNoch keine Bewertungen

- Btx2000 Week 2 自改1 Tutorial QuestionDokument3 SeitenBtx2000 Week 2 自改1 Tutorial Question朱潇妤Noch keine Bewertungen

- Week 3 Lecture Example (With Solutions)Dokument6 SeitenWeek 3 Lecture Example (With Solutions)朱潇妤Noch keine Bewertungen

- Lecture Week 4Dokument48 SeitenLecture Week 4朱潇妤Noch keine Bewertungen

- Week 11 Lecture Examples 1 and 2Dokument2 SeitenWeek 11 Lecture Examples 1 and 2朱潇妤Noch keine Bewertungen

- Lecture Week 5Dokument56 SeitenLecture Week 5朱潇妤100% (1)

- Week 8 Lecture Example - Quality SolsDokument2 SeitenWeek 8 Lecture Example - Quality Sols朱潇妤Noch keine Bewertungen

- Type of Theories: ACC3100 WEEK 2 Accounting TheoryDokument7 SeitenType of Theories: ACC3100 WEEK 2 Accounting Theory朱潇妤Noch keine Bewertungen

- Chapter 12 - Job-Order-Process and Hybrid Costing SystemsDokument52 SeitenChapter 12 - Job-Order-Process and Hybrid Costing Systems朱潇妤100% (2)

- ACC3200 - ACF3200 - Week 01 Tutorial SolutionDokument4 SeitenACC3200 - ACF3200 - Week 01 Tutorial Solution朱潇妤Noch keine Bewertungen

- DocxDokument18 SeitenDocx朱潇妤Noch keine Bewertungen

- Quiz 7Dokument3 SeitenQuiz 7朱潇妤Noch keine Bewertungen

- B. Ledgers: Accounting TheoryDokument8 SeitenB. Ledgers: Accounting Theory朱潇妤Noch keine Bewertungen

- NPV and IRR, Payback Period, ImportantDokument5 SeitenNPV and IRR, Payback Period, Important朱潇妤Noch keine Bewertungen

- Quiz 9Dokument3 SeitenQuiz 9朱潇妤100% (1)

- Quiz 8Dokument2 SeitenQuiz 8朱潇妤Noch keine Bewertungen

- BFC2140 PV and FV CaluateDokument4 SeitenBFC2140 PV and FV Caluate朱潇妤Noch keine Bewertungen

- Quiz 1Dokument1 SeiteQuiz 1朱潇妤Noch keine Bewertungen

- Quiz 5Dokument4 SeitenQuiz 5朱潇妤Noch keine Bewertungen

- Review Module 10 Engineering Economy Part 1Dokument2 SeitenReview Module 10 Engineering Economy Part 1Althea De LeonNoch keine Bewertungen

- RTP May 2018 New Gr1Dokument122 SeitenRTP May 2018 New Gr1subhanvts7781Noch keine Bewertungen

- Cost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Dokument35 SeitenCost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Yonas BamlakuNoch keine Bewertungen

- AngelDokument46 SeitenAngelTORRES , VENUSNoch keine Bewertungen

- N.jayasankar 773Dokument18 SeitenN.jayasankar 773bhanganrosevcNoch keine Bewertungen

- ACCT 2211 Assignment 1Dokument12 SeitenACCT 2211 Assignment 1Tannaz SNoch keine Bewertungen

- Assignment of Cash ManagementDokument15 SeitenAssignment of Cash ManagementnraghaveNoch keine Bewertungen

- Advanced Accounting Study MaterialDokument974 SeitenAdvanced Accounting Study MaterialPrashant Sagar Gautam100% (2)

- 1913 IRS 1040 FormDokument4 Seiten1913 IRS 1040 Formfredlox100% (4)

- Research Paper On Qualifying ActivitiesDokument48 SeitenResearch Paper On Qualifying ActivitiesResearch and Development Tax Credit Magazine; David Greenberg PhD, MSA, EA, CPA; TGI; 646-705-2910100% (1)

- Analysis of Financial Statement-683Dokument10 SeitenAnalysis of Financial Statement-683MariNoch keine Bewertungen

- Flash MemoryDokument14 SeitenFlash MemoryPranav TatavarthiNoch keine Bewertungen

- Sports Equipment Retail Business Plan (Sunny)Dokument15 SeitenSports Equipment Retail Business Plan (Sunny)mattogillNoch keine Bewertungen

- How One Can Create HufDokument5 SeitenHow One Can Create HufrbspNoch keine Bewertungen

- Trial BalanceDokument11 SeitenTrial Balancejhastine_0712Noch keine Bewertungen

- Formatted Brgy. FormsDokument21 SeitenFormatted Brgy. FormsBarangay CambaroNoch keine Bewertungen

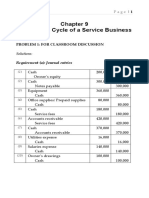

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDokument52 SeitenSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- UOM Students' Union Bilan 2013/14Dokument153 SeitenUOM Students' Union Bilan 2013/14Rishikesh PoorunNoch keine Bewertungen

- Comparative Analysis of Measurement After Recognition of Property Plant and EquipmentDokument14 SeitenComparative Analysis of Measurement After Recognition of Property Plant and EquipmentMstefNoch keine Bewertungen

- Assigment Financial ManagementDokument5 SeitenAssigment Financial ManagementMuhammad A IsmaielNoch keine Bewertungen

- 2 INTRODUCTION WE Have Visited Sabarkantha District Co Operative Milk Producers Union LTD." Sabar DairyDokument87 Seiten2 INTRODUCTION WE Have Visited Sabarkantha District Co Operative Milk Producers Union LTD." Sabar Dairymayur_1990Noch keine Bewertungen

- p3 Acc 110 ReviewerDokument12 Seitenp3 Acc 110 ReviewerRona Amor MundaNoch keine Bewertungen

- Full Download Financial Reporting Financial Statement Analysis and Valuation 7th Edition Whalen Test BankDokument35 SeitenFull Download Financial Reporting Financial Statement Analysis and Valuation 7th Edition Whalen Test Bankjulianwellsueiy100% (19)

- Notes For Income tax-IIDokument10 SeitenNotes For Income tax-IIDr.M.KAMARAJ M.COM., M.Phil.,Ph.D100% (1)

- Casper Investor Presentation 2Q'21 August UpdateDokument20 SeitenCasper Investor Presentation 2Q'21 August UpdatepaoscagNoch keine Bewertungen

- T11F CHP 03 1 Income Sources 2011Dokument140 SeitenT11F CHP 03 1 Income Sources 2011jessie1614Noch keine Bewertungen

- Chapter 3 Accrued Liabilities and Deferred Revenue - ContinuationDokument29 SeitenChapter 3 Accrued Liabilities and Deferred Revenue - ContinuationJouhara San JuanNoch keine Bewertungen

- Assessment and Computation of Working Capital Requirements Numerical QuestionsDokument6 SeitenAssessment and Computation of Working Capital Requirements Numerical QuestionsNazreena MukherjeeNoch keine Bewertungen

- ACC 1701X Mock Exam #1 SolutionDokument13 SeitenACC 1701X Mock Exam #1 SolutionShaunny BravoNoch keine Bewertungen

- ACCT 110 - Assignment - EBR DecDokument17 SeitenACCT 110 - Assignment - EBR DecBen Noah EuroNoch keine Bewertungen