Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- ListDokument4 SeitenListrobbi ajaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- To Financial Statements: Financial Accounting, Seventh EditionDokument46 SeitenTo Financial Statements: Financial Accounting, Seventh Editionrobbi ajaNoch keine Bewertungen

- Ifrs6 en PDFDokument5 SeitenIfrs6 en PDFrobbi ajaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Management and Financial Accounting in Oil and Gas Upstream IndustryDokument4 SeitenManagement and Financial Accounting in Oil and Gas Upstream Industryrobbi ajaNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Theequitypremiumin150textbooksfullpdf PDFDokument28 SeitenTheequitypremiumin150textbooksfullpdf PDFrobbi ajaNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Us Aers Oil and Gas PDFDokument114 SeitenUs Aers Oil and Gas PDFrobbi ajaNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- FC-100V FC-200V en PDFDokument149 SeitenFC-100V FC-200V en PDFrobbi ajaNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- ThomsonNOW Start Smart Guide For InstructorsDokument160 SeitenThomsonNOW Start Smart Guide For Instructorsrobbi ajaNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Psak Pocket 2016Dokument76 SeitenPsak Pocket 2016Tia VenicaNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Us Aers Oil and Gas PDFDokument114 SeitenUs Aers Oil and Gas PDFrobbi ajaNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Financial Reporting Oil and GasDokument68 SeitenFinancial Reporting Oil and GasNevisa ZhuriNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Quiz KTTCDokument64 SeitenQuiz KTTCChi NguyenNoch keine Bewertungen

- Tutorial (Merchandising With Answers)Dokument16 SeitenTutorial (Merchandising With Answers)Luize Nathaniele Santos0% (1)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- ACCA F8 Chapter 14 ReceivableDokument18 SeitenACCA F8 Chapter 14 ReceivableOmer UddinNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- From 28.11.21 Power Point AccountingDokument191 SeitenFrom 28.11.21 Power Point AccountingAbdul AzizNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Grants Business ProcessDokument18 SeitenGrants Business ProcessPavan polumNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Summary Taxes BrazilDokument29 SeitenSummary Taxes BrazilRegis NemezioNoch keine Bewertungen

- MULTIPLE CHOICE-CPA AdaptedDokument4 SeitenMULTIPLE CHOICE-CPA AdaptedEdiane QuilezaNoch keine Bewertungen

- Week 3 Tutorial SolutionsDokument31 SeitenWeek 3 Tutorial SolutionsalexandraNoch keine Bewertungen

- CPW FormsDokument163 SeitenCPW Formssurendra kumarNoch keine Bewertungen

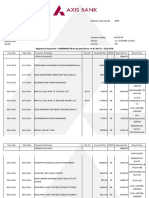

- Axis Jan-Feb-2016 PDFDokument22 SeitenAxis Jan-Feb-2016 PDFAnonymous akFYwVpNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Accounting Chapter 3 NotesDokument3 SeitenAccounting Chapter 3 Notesapi-698495592Noch keine Bewertungen

- Chapter 6 Book-Keeping Balancing Off AccountsDokument12 SeitenChapter 6 Book-Keeping Balancing Off AccountsfileacademyNoch keine Bewertungen

- Lesson 7 - Financial Analysis and Accounting Basics-1Dokument34 SeitenLesson 7 - Financial Analysis and Accounting Basics-1Khatylyn MadroneroNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- BIR - DONOR'S TaxDokument5 SeitenBIR - DONOR'S TaxKim EspinaNoch keine Bewertungen

- Engleski I I II PDFDokument23 SeitenEngleski I I II PDFvejnicNoch keine Bewertungen

- AC Chapter 9Dokument19 SeitenAC Chapter 9Minh AnhNoch keine Bewertungen

- 06C Investment Property & Other InvestmentsDokument8 Seiten06C Investment Property & Other Investmentsrandomlungs121223Noch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- CUET SQP Accountancy PaperDokument12 SeitenCUET SQP Accountancy PaperShreyas BansalNoch keine Bewertungen

- PR P4-5a 29 November 2016Dokument8 SeitenPR P4-5a 29 November 2016Amiratul Ratna Putri50% (2)

- 2 - A. Problems - Property Plant and EquipmentDokument59 Seiten2 - A. Problems - Property Plant and EquipmentsbibandiganNoch keine Bewertungen

- Cash Accrual Single EntryDokument3 SeitenCash Accrual Single EntryJustine GuilingNoch keine Bewertungen

- Exercise 2 AnswersDokument44 SeitenExercise 2 Answers4- Desiree FuaNoch keine Bewertungen

- CHAPTER 5 Accounting Equation and Rules of Double EntryDokument9 SeitenCHAPTER 5 Accounting Equation and Rules of Double Entrynatasha thaiNoch keine Bewertungen

- CH - 05 Statement of Cash FlowsDokument26 SeitenCH - 05 Statement of Cash FlowsOwais Zaman100% (1)

- Chapter 10 Shareholders EquityDokument10 SeitenChapter 10 Shareholders EquityMarine De CocquéauNoch keine Bewertungen

- F.19 - GR - IR RegroupingDokument9 SeitenF.19 - GR - IR RegroupingDiogo Oliveira SilvaNoch keine Bewertungen

- Suggested Answers Intermediate Examinations - Autumn 2011: Financial AccountingDokument6 SeitenSuggested Answers Intermediate Examinations - Autumn 2011: Financial AccountingUssama AbbasNoch keine Bewertungen

- Accounts PayableDokument102 SeitenAccounts PayableAtilaUnorteNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Bank Soal IfrsDokument9 SeitenBank Soal IfrsSabina HadiwardoyoNoch keine Bewertungen

- Bank Reconciliation ReviewerDokument2 SeitenBank Reconciliation Reviewerfred ferrera jrNoch keine Bewertungen