Das könnte Ihnen auch gefallen

- Econ101B NotesDokument97 SeitenEcon101B NotesYilena HsueNoch keine Bewertungen

- Aggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserDokument18 SeitenAggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserIndivineNoch keine Bewertungen

- Gyaan Kosh: Global EconomicsDokument19 SeitenGyaan Kosh: Global EconomicsU KUNALNoch keine Bewertungen

- Eco120DE - Saturday Session 1 0640Dokument67 SeitenEco120DE - Saturday Session 1 0640Izzat AmirNoch keine Bewertungen

- Chapter 2 EconomicsDokument26 SeitenChapter 2 EconomicssthesibisiNoch keine Bewertungen

- ME Cycle 8 Session 7Dokument96 SeitenME Cycle 8 Session 7OttilieNoch keine Bewertungen

- Indirect Taxes: Ian Crawford (Surrey / IFS) Michael Keen (IMF) Stephen Smith (UCL)Dokument16 SeitenIndirect Taxes: Ian Crawford (Surrey / IFS) Michael Keen (IMF) Stephen Smith (UCL)vivekgupta4444Noch keine Bewertungen

- EC 102 Revisions Lectures - Macro 2013Dokument56 SeitenEC 102 Revisions Lectures - Macro 2013TylerTangTengYangNoch keine Bewertungen

- ECON3102 Lec9Dokument22 SeitenECON3102 Lec9ag268Noch keine Bewertungen

- Economics For Business: Introduction To The MacroeconomyDokument25 SeitenEconomics For Business: Introduction To The MacroeconomyUsman ZebNoch keine Bewertungen

- Lectures 8-14Dokument47 SeitenLectures 8-14SHIVAM SHARMANoch keine Bewertungen

- Why Do We Study The National Income Accounts?Dokument36 SeitenWhy Do We Study The National Income Accounts?SiddharthNoch keine Bewertungen

- Mankiw10e Lecture Slides Ch06Dokument58 SeitenMankiw10e Lecture Slides Ch06Anggi YudhaNoch keine Bewertungen

- Chapter 1 - Introduction To MacroeconomicsDokument25 SeitenChapter 1 - Introduction To MacroeconomicsDaNetNoch keine Bewertungen

- Session 3 & 4 Aggregate Demand and Multiplier ModelDokument64 SeitenSession 3 & 4 Aggregate Demand and Multiplier ModelPrateek BabbewalaNoch keine Bewertungen

- Macroeconomics: Lecture 3: Real and Nominal Interest RatesDokument10 SeitenMacroeconomics: Lecture 3: Real and Nominal Interest RatesАдамNoch keine Bewertungen

- C1234 Updated Đã Chuyển ĐổiDokument176 SeitenC1234 Updated Đã Chuyển ĐổiBảo ChâuNoch keine Bewertungen

- Lecture 3 - UpdatedDokument46 SeitenLecture 3 - UpdatedMinal AggarwalNoch keine Bewertungen

- EC 102 Revisions Lectures - Macro - 2015Dokument54 SeitenEC 102 Revisions Lectures - Macro - 2015TylerTangTengYangNoch keine Bewertungen

- Macroeconomics FinalDokument57 SeitenMacroeconomics Finaljatin khannaNoch keine Bewertungen

- Chapter 1.4 - GDP ComponentsDokument26 SeitenChapter 1.4 - GDP Componentsgon.ugarrizaNoch keine Bewertungen

- Macroeconomics IIDokument35 SeitenMacroeconomics IIEmre BüyükbayraktarNoch keine Bewertungen

- Study NotesDokument65 SeitenStudy NoteskhmaponyaNoch keine Bewertungen

- MacroEconomics - MultiplierDokument38 SeitenMacroEconomics - MultiplierPranay KarthikNoch keine Bewertungen

- ECON5002 Macroeconomic Theory Week 2: "The Goods Market": Nadine Yamout University of SydneyDokument30 SeitenECON5002 Macroeconomic Theory Week 2: "The Goods Market": Nadine Yamout University of Sydneyxin yiNoch keine Bewertungen

- Introduction To Macroeconomics and National Income AccountingDokument7 SeitenIntroduction To Macroeconomics and National Income AccountingjomardansNoch keine Bewertungen

- Topic 2 National Accounting, The Keynesian Income-Expenditure Model and Fiscal PolicyDokument62 SeitenTopic 2 National Accounting, The Keynesian Income-Expenditure Model and Fiscal PolicyjoeybaggieNoch keine Bewertungen

- Aggregate Expenditure and Equilibrium OutputDokument69 SeitenAggregate Expenditure and Equilibrium OutputhongphakdeyNoch keine Bewertungen

- Lecture 3 (Chapter 19)Dokument28 SeitenLecture 3 (Chapter 19)raymondNoch keine Bewertungen

- Is-Lm CurveDokument7 SeitenIs-Lm Curvejmatsanura1Noch keine Bewertungen

- Saving InvestmentDokument58 SeitenSaving InvestmentTumbal GrowtopiaNoch keine Bewertungen

- Mail To Reg Stud 72232 610769 20230904 062954 670Dokument39 SeitenMail To Reg Stud 72232 610769 20230904 062954 670UshaNoch keine Bewertungen

- ECON102 - Intro To Macro Data by Veronica GuerrieriDokument51 SeitenECON102 - Intro To Macro Data by Veronica GuerrieriWalijaNoch keine Bewertungen

- Learning Unit 7 Keynesian Model Including The Government and The Foreign SectorDokument23 SeitenLearning Unit 7 Keynesian Model Including The Government and The Foreign SectorVinny Hungwe100% (1)

- 5,6. SessionDokument15 Seiten5,6. SessionAman SinghNoch keine Bewertungen

- National Income: Concepts and MeasurementDokument34 SeitenNational Income: Concepts and MeasurementQammer ShahzadNoch keine Bewertungen

- Econ1102 Week 4Dokument41 SeitenEcon1102 Week 4AAA820Noch keine Bewertungen

- Macroeconomics For Business: - MicroeconomicsDokument79 SeitenMacroeconomics For Business: - MicroeconomicshatanoloveNoch keine Bewertungen

- Chapter 3 (A) : GDP Determination With Govt. and Open EconomyDokument26 SeitenChapter 3 (A) : GDP Determination With Govt. and Open EconomyNishantNoch keine Bewertungen

- Economics-II: Ashita AllamrajuDokument47 SeitenEconomics-II: Ashita AllamrajuutkarshNoch keine Bewertungen

- (TOPIC 5) IS-LM-FX Model and Floating ERsDokument96 Seiten(TOPIC 5) IS-LM-FX Model and Floating ERsjjho4832Noch keine Bewertungen

- Sessions 2, 3, 4, 5 - Inflation - National IncomeDokument110 SeitenSessions 2, 3, 4, 5 - Inflation - National IncomeAbhay SahuNoch keine Bewertungen

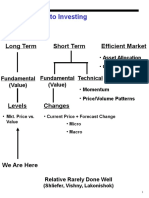

- Approaches To Investing: Long Term Short Term Efficient MarketDokument71 SeitenApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNoch keine Bewertungen

- L2 - PartA - The Keynesian System - The Role of ADDokument19 SeitenL2 - PartA - The Keynesian System - The Role of ADJia Yun YapNoch keine Bewertungen

- Introduction To Macroeconomics 2Dokument40 SeitenIntroduction To Macroeconomics 2Shivangi GuptaNoch keine Bewertungen

- CSNW - zUSS1SJ8P81EptUnw - Macroeconomics Background Notes - Module 1 c2 - v2Dokument22 SeitenCSNW - zUSS1SJ8P81EptUnw - Macroeconomics Background Notes - Module 1 c2 - v2farinNoch keine Bewertungen

- The National Income AccountingDokument38 SeitenThe National Income AccountingTin RobisoNoch keine Bewertungen

- Macro Classes 1-3Dokument35 SeitenMacro Classes 1-3Shajidur RashidNoch keine Bewertungen

- Lecture #7 - Theory of Income DeterminationDokument53 SeitenLecture #7 - Theory of Income DeterminationMike Viet Hoa NguyenNoch keine Bewertungen

- Data and Questions of MacroeconomicsDokument35 SeitenData and Questions of MacroeconomicsSudip DhakalNoch keine Bewertungen

- The Simple Keynesian Model: Conditions For Equilibrium OutputDokument9 SeitenThe Simple Keynesian Model: Conditions For Equilibrium OutputBadal PramanikNoch keine Bewertungen

- Measuring Macro Performance: The Price Level Savings & WealthDokument38 SeitenMeasuring Macro Performance: The Price Level Savings & WealthPaully Fireberry NguyenNoch keine Bewertungen

- Review Notes - Introduction To MacroeconomicsDokument2 SeitenReview Notes - Introduction To MacroeconomicsLote MarcellanoNoch keine Bewertungen

- EinfMakro 2023 - Vorlesung 1Dokument24 SeitenEinfMakro 2023 - Vorlesung 1Miloje RamadaniNoch keine Bewertungen

- Lecture 3-4 Current Account Imbalances and FXDokument81 SeitenLecture 3-4 Current Account Imbalances and FXTrần Đức TàiNoch keine Bewertungen

- Principles of Macroeconomics Econ 109 - Output DeterminationDokument11 SeitenPrinciples of Macroeconomics Econ 109 - Output Determinationannelinemupunga60Noch keine Bewertungen

- Economics 212 Principles of Macroeconomics Study GuideDokument12 SeitenEconomics 212 Principles of Macroeconomics Study GuideDuc PhamNoch keine Bewertungen

- Econ 2003 - Open EconomyDokument6 SeitenEcon 2003 - Open Economycracker drawingsNoch keine Bewertungen

- Pratt 2013 International Studies QuarterlyDokument12 SeitenPratt 2013 International Studies QuarterlyJudith UmesiNoch keine Bewertungen

- INRL 10010 SyllabusDokument9 SeitenINRL 10010 SyllabusJudith UmesiNoch keine Bewertungen

- Homer and HerodotusDokument4 SeitenHomer and HerodotusJudith UmesiNoch keine Bewertungen

- Similes in The IliadDokument18 SeitenSimiles in The IliadJudith UmesiNoch keine Bewertungen

- The Globalization of World Politics. Introduction To International Relations TheoryDokument212 SeitenThe Globalization of World Politics. Introduction To International Relations TheoryBrunno A. Araujo20% (5)

- Study On The Port of RotterdamDokument292 SeitenStudy On The Port of RotterdamJulio César AlcarazNoch keine Bewertungen

- 3Dokument10 Seiten3JaeDukAndrewSeoNoch keine Bewertungen

- Account Closure Form Citi BankDokument1 SeiteAccount Closure Form Citi BankSarfaraz AhmedNoch keine Bewertungen

- DDA (Management and Disposal of Housing Estates) Regulations 1968Dokument17 SeitenDDA (Management and Disposal of Housing Estates) Regulations 1968SameerVermaNoch keine Bewertungen

- Collecting Coins of AustraliaDokument7 SeitenCollecting Coins of Australiazonlives100% (1)

- Price Expansion PathsDokument4 SeitenPrice Expansion Pathsvinayvasant2020Noch keine Bewertungen

- Gyetvai Attila CVDokument2 SeitenGyetvai Attila CVmyregistratNoch keine Bewertungen

- Jehle SolutionsDokument5 SeitenJehle SolutionsTamás Szabó50% (2)

- Politeknik MicroeconomicsDokument6 SeitenPoliteknik MicroeconomicsSno Xthree100% (2)

- Chapter 11 - AnswerDokument31 SeitenChapter 11 - AnsweragnesNoch keine Bewertungen

- Engineering Economics Cheat SheetDokument4 SeitenEngineering Economics Cheat SheetNasser SANoch keine Bewertungen

- 11 35Dokument8 Seiten11 35Wildan IrfansyahNoch keine Bewertungen

- Compound InterestDokument10 SeitenCompound InterestgetphotojobNoch keine Bewertungen

- 40units of Goods + 10units of Goods 50units of GoodsDokument4 Seiten40units of Goods + 10units of Goods 50units of GoodsseraphevileyesNoch keine Bewertungen

- Costos de Transporte m3-Km y Ton-KmDokument68 SeitenCostos de Transporte m3-Km y Ton-KmROBERT50% (2)

- 2 Simple Regression Model Estimation and PropertiesDokument48 Seiten2 Simple Regression Model Estimation and PropertiesMuhammad Chaudhry100% (1)

- Stat Seasonal Adjustment enDokument163 SeitenStat Seasonal Adjustment engialutNoch keine Bewertungen

- The Economic PerspectiveDokument69 SeitenThe Economic PerspectiveDr Rushen SinghNoch keine Bewertungen

- Abbington Youth Center CaseDokument6 SeitenAbbington Youth Center CaseP3 Powers100% (2)

- MicroeconomicsDokument82 SeitenMicroeconomicsPriyaSharmaNoch keine Bewertungen

- 31754Dokument7 Seiten31754moustafamahmoud2010100% (1)

- Silent RiskDokument389 SeitenSilent Riskmicha424100% (1)

- Single Index ModelDokument4 SeitenSingle Index ModelNikita Mehta DesaiNoch keine Bewertungen

- Microeconomics Practice QuestionsDokument5 SeitenMicroeconomics Practice Questionstoms446Noch keine Bewertungen

- Chart PatternsDokument5 SeitenChart PatternsKevin Rune Nyheim100% (2)

- PerTrac Investment Statistics A Reference Guide September 2012Dokument65 SeitenPerTrac Investment Statistics A Reference Guide September 2012Murray PriestleyNoch keine Bewertungen

- Microeconomic Theory and Computation Mith Maxima (Michael R. Hammock, J. Wilson Mixon)Dokument393 SeitenMicroeconomic Theory and Computation Mith Maxima (Michael R. Hammock, J. Wilson Mixon)zeque85Noch keine Bewertungen

- Break Even AnalysisDokument33 SeitenBreak Even AnalysisArunraj ArumugamNoch keine Bewertungen

- Cost Management PMP Questions-AnswersDokument10 SeitenCost Management PMP Questions-Answerspratikdas2670100% (1)

- SupplyDokument19 SeitenSupplykimcy19Noch keine Bewertungen