Das könnte Ihnen auch gefallen

- Arthur Andersen CaseDokument10 SeitenArthur Andersen CaseHarsha ShivannaNoch keine Bewertungen

- Arthur Andersen, LLPDokument6 SeitenArthur Andersen, LLPJohnny Bi Z⃝⃤Noch keine Bewertungen

- Arthur Andersen: An Accounting Confidence Crisis: Center For Ethical Organizational Cultures Auburn UniversityDokument12 SeitenArthur Andersen: An Accounting Confidence Crisis: Center For Ethical Organizational Cultures Auburn UniversityDendy TryandaNoch keine Bewertungen

- Arthur AndersenDokument9 SeitenArthur AndersenSheraz HasanNoch keine Bewertungen

- ACCA 100 YearsDokument100 SeitenACCA 100 YearsShouravpedia™Noch keine Bewertungen

- A Study On Quality of Earnings in Petrochemical IndustryDokument9 SeitenA Study On Quality of Earnings in Petrochemical IndustrySudheer KumarNoch keine Bewertungen

- Final Thesis IntanDokument77 SeitenFinal Thesis IntanKarina RusmanNoch keine Bewertungen

- An Analysis of Fraud Triangle and Responsibilities of AuditorsDokument8 SeitenAn Analysis of Fraud Triangle and Responsibilities of AuditorsPrihandani AntonNoch keine Bewertungen

- ACC101 Chapter 01 HuyenDTT24Dokument40 SeitenACC101 Chapter 01 HuyenDTT24Doanh PhùngNoch keine Bewertungen

- Enron Case History and Major Issues SummaryDokument6 SeitenEnron Case History and Major Issues Summaryshanker23scribd100% (1)

- Tootsie Roll-Final PaperDokument19 SeitenTootsie Roll-Final Paperapi-240320161Noch keine Bewertungen

- Forensic Audit PDFDokument6 SeitenForensic Audit PDFKoolmind33% (3)

- Worldcom: A Focus On Internal Audit: SynopsisDokument5 SeitenWorldcom: A Focus On Internal Audit: SynopsisCryptic LollNoch keine Bewertungen

- Client Evaluation and Planning The AuditDokument31 SeitenClient Evaluation and Planning The AuditEron Shaikh100% (1)

- Waste Management, Inc.: Manipulating Accounting EstimatesDokument10 SeitenWaste Management, Inc.: Manipulating Accounting EstimatesJimmy NdawaNoch keine Bewertungen

- Chap 5 Accounting For Merchandising OperationDokument71 SeitenChap 5 Accounting For Merchandising OperationtamimNoch keine Bewertungen

- Impact of Lehman Brothers Bankruptcy on Individual WealthDokument25 SeitenImpact of Lehman Brothers Bankruptcy on Individual WealthNishat Siyara100% (1)

- 2021 ACA Syllabus Handbook - AdvancedDokument59 Seiten2021 ACA Syllabus Handbook - AdvancedfatehsalehNoch keine Bewertungen

- Assurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15Dokument41 SeitenAssurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15dhea100% (1)

- IIBA® Business Analysis Foundations Business Process Modeling - Gaurav Kumar WankarDokument1 SeiteIIBA® Business Analysis Foundations Business Process Modeling - Gaurav Kumar WankarGaurav Kumar WankarNoch keine Bewertungen

- Corporate DisclosureDokument46 SeitenCorporate DisclosureSameerLalakiyaNoch keine Bewertungen

- Case #2.3 - Worldcom - Professional Responsibility: I. Technical Audit GuidanceDokument8 SeitenCase #2.3 - Worldcom - Professional Responsibility: I. Technical Audit GuidanceDaniel HunksNoch keine Bewertungen

- AFT 1043 Basic Accounting: Group AssignmentDokument4 SeitenAFT 1043 Basic Accounting: Group AssignmentWenXin ChiongNoch keine Bewertungen

- Corporate Valuation - Chapter 2Dokument4 SeitenCorporate Valuation - Chapter 2Shreya s shettyNoch keine Bewertungen

- Gutierrez Construction Company journal entriesDokument3 SeitenGutierrez Construction Company journal entriesAj GuanzonNoch keine Bewertungen

- The Fall of Enron: Group 1Dokument20 SeitenThe Fall of Enron: Group 1Thiện NhânNoch keine Bewertungen

- Auditing Sols To Homework Tute Qs - S2 2016 (WK 4 CH 8)Dokument6 SeitenAuditing Sols To Homework Tute Qs - S2 2016 (WK 4 CH 8)sonima aroraNoch keine Bewertungen

- HealthSouth Case StudyDokument41 SeitenHealthSouth Case StudyAlex D. Padilla100% (1)

- Forecasting Debt and InterestDokument16 SeitenForecasting Debt and InterestRnaidoo1972Noch keine Bewertungen

- Complete Revision Notes Auditing 1Dokument90 SeitenComplete Revision Notes Auditing 1Marwin AceNoch keine Bewertungen

- Memo 5A Ocean Manuf.Dokument2 SeitenMemo 5A Ocean Manuf.Morgan GreeneNoch keine Bewertungen

- Forensic Accounting Education, Institutions, and SpecialtiesDokument25 SeitenForensic Accounting Education, Institutions, and SpecialtiesAlysha Harvey EA100% (1)

- Tugas FM-High Rock IndustryDokument5 SeitenTugas FM-High Rock IndustryAnggit Tut PinilihNoch keine Bewertungen

- Accounting For ManagersDokument286 SeitenAccounting For ManagersSatyam Rastogi100% (1)

- AEB14 SM CH17 v2Dokument31 SeitenAEB14 SM CH17 v2RonLiu350% (1)

- Introduction To Accounting 1st SemDokument15 SeitenIntroduction To Accounting 1st SemANJALI KUMARI100% (1)

- Beams - 12ge - LN04 - Consolidation TechniqueDokument48 SeitenBeams - 12ge - LN04 - Consolidation TechniqueArisBachtiarNoch keine Bewertungen

- Ecopak Case Notes Chapter 4 5Dokument3 SeitenEcopak Case Notes Chapter 4 5Gajan SelvaNoch keine Bewertungen

- Auditing: The Art and Science of Assurance Engagements: Fifteenth Canadian EditionDokument21 SeitenAuditing: The Art and Science of Assurance Engagements: Fifteenth Canadian EditionSaawan PatelNoch keine Bewertungen

- Research Paper OnDokument15 SeitenResearch Paper OnKusum BhandariNoch keine Bewertungen

- Evolution of AccountingDokument5 SeitenEvolution of AccountingCHRISTINE ELAINE TOLENTINONoch keine Bewertungen

- Barringer Chapter 1 PowerpointDokument38 SeitenBarringer Chapter 1 PowerpointCiara Caldwell75% (4)

- 2022 - 05 - Bad and Doubtful DebtsDokument39 Seiten2022 - 05 - Bad and Doubtful DebtsSafi UllahNoch keine Bewertungen

- TMP 15004 Solutions Manual For The Lakeside Company Case Studies in Auditing 12e 1360219079Dokument4 SeitenTMP 15004 Solutions Manual For The Lakeside Company Case Studies in Auditing 12e 1360219079Mark Vendolf KongNoch keine Bewertungen

- AF301 Fair V Alue Accounting - Lecture - HandoutDokument8 SeitenAF301 Fair V Alue Accounting - Lecture - HandoutAmiteshNoch keine Bewertungen

- Comparative Study Auditing Between Profit & Nonprofit OrganizationsDokument52 SeitenComparative Study Auditing Between Profit & Nonprofit OrganizationsNael Loay Arandas100% (7)

- Case 2.3 HanauerDokument10 SeitenCase 2.3 HanauerAlexa RodriguezNoch keine Bewertungen

- Accounting history postwar period modern trendsDokument5 SeitenAccounting history postwar period modern trendstiyas100% (1)

- Sitaram Gokul MilkDokument20 SeitenSitaram Gokul Milkpramodth71% (14)

- Financial StatementDokument5 SeitenFinancial StatementJubelle Tacusalme PunzalanNoch keine Bewertungen

- IPSAS Explained: A Summary of International Public Sector Accounting StandardsVon EverandIPSAS Explained: A Summary of International Public Sector Accounting StandardsNoch keine Bewertungen

- Determinants of Level of Sustainability ReportVon EverandDeterminants of Level of Sustainability ReportNoch keine Bewertungen

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionVon EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionNoch keine Bewertungen

- Risk Based Internal Audit A Complete Guide - 2020 EditionVon EverandRisk Based Internal Audit A Complete Guide - 2020 EditionNoch keine Bewertungen

- Arthur Andersen CollapseDokument21 SeitenArthur Andersen CollapseRagil RamadhaniNoch keine Bewertungen

- Producers Bank case study: Enhancing reporting & analyticsDokument3 SeitenProducers Bank case study: Enhancing reporting & analyticsvictorious xtremeNoch keine Bewertungen

- 2159 2009Dokument9 Seiten2159 2009wolf10070% (2)

- Revised Rules of Procedure for PNP Disciplinary CasesDokument44 SeitenRevised Rules of Procedure for PNP Disciplinary CasesApril Elenor Juco100% (1)

- Revision 2 - Investment AppraisalDokument27 SeitenRevision 2 - Investment AppraisalVishal PrasadNoch keine Bewertungen

- 3.4 Gov LabDokument4 Seiten3.4 Gov LabSlothChain EmpireNoch keine Bewertungen

- Crandall Reexam RequestDokument119 SeitenCrandall Reexam RequestJennifer M GallagherNoch keine Bewertungen

- English f4 (MC Plus)Dokument7 SeitenEnglish f4 (MC Plus)kyraNoch keine Bewertungen

- Anjali Kapoor vs. Rajiv Baijal946Dokument5 SeitenAnjali Kapoor vs. Rajiv Baijal946samiaNoch keine Bewertungen

- Ufc Ingles1 P S 1999-2000Dokument4 SeitenUfc Ingles1 P S 1999-2000Orlando Firmeza0% (1)

- GstnoidaDokument3 SeitenGstnoidaRohit SandhuNoch keine Bewertungen

- Common Cavities & Tooling: 2-Way 3-Way / 3-Way Short 4-WayDokument6 SeitenCommon Cavities & Tooling: 2-Way 3-Way / 3-Way Short 4-WaytecnicomanelNoch keine Bewertungen

- Write Your Handwritten Answers in A Bond or Line Paper and Submit The SameDokument4 SeitenWrite Your Handwritten Answers in A Bond or Line Paper and Submit The SameIan Ray PaglinawanNoch keine Bewertungen

- HMWSSBDokument11 SeitenHMWSSBSoori GanipineniNoch keine Bewertungen

- Criminalization of Politics in India: A Project StudyDokument24 SeitenCriminalization of Politics in India: A Project Studysanchitsingh75% (12)

- KP Form 28 TransmittalDokument39 SeitenKP Form 28 TransmittalBarangay Magsaysay ParangNoch keine Bewertungen

- Free - Dinosaur Alphabet Clip CardsDokument8 SeitenFree - Dinosaur Alphabet Clip CardsMariana74Noch keine Bewertungen

- Korean Grape Sales ContractDokument2 SeitenKorean Grape Sales ContractNhư QuỳnhNoch keine Bewertungen

- FAQs - Infosys Online TestDokument3 SeitenFAQs - Infosys Online TestNilprabha ZarekarNoch keine Bewertungen

- BreadTalk Group Limited Annual Report 2017Dokument172 SeitenBreadTalk Group Limited Annual Report 2017jacechanNoch keine Bewertungen

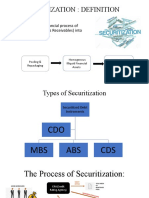

- SECURITIZATIONDokument5 SeitenSECURITIZATIONASHISH KUMARNoch keine Bewertungen

- Complaint Francisco RamirezDokument7 SeitenComplaint Francisco RamirezGoMNNoch keine Bewertungen

- RSA Archer Policy Management: Build Your Governance, Risk and Compliance Program On A Firm FoundationDokument2 SeitenRSA Archer Policy Management: Build Your Governance, Risk and Compliance Program On A Firm Foundationnmukherjee20Noch keine Bewertungen

- Operational Support Client Forum PDFDokument129 SeitenOperational Support Client Forum PDFASDFGHTNoch keine Bewertungen

- Income Tax ClassificationDokument3 SeitenIncome Tax ClassificationALMA MORENANoch keine Bewertungen

- 2016 Canary Yelloweye ID FlyerDokument2 Seiten2016 Canary Yelloweye ID FlyeraninnaNoch keine Bewertungen

- A History of The System of Education in The PhilippinesDokument6 SeitenA History of The System of Education in The PhilippinesjenNoch keine Bewertungen

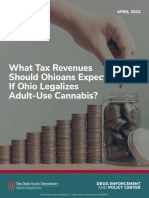

- What Tax Revenues Should Ohioans Expect If Ohio Legalizes Adult-Use Cannabis?Dokument9 SeitenWhat Tax Revenues Should Ohioans Expect If Ohio Legalizes Adult-Use Cannabis?Sarah McRitchieNoch keine Bewertungen

- Callable Bonds ExplainedDokument33 SeitenCallable Bonds ExplainedtwinklenoorNoch keine Bewertungen

- Terakhir P4-1Dokument1 SeiteTerakhir P4-1Arnalistan EkaNoch keine Bewertungen

- PO Correction and Return Process in Oracle EBSDokument11 SeitenPO Correction and Return Process in Oracle EBSADISH C ANoch keine Bewertungen