Das könnte Ihnen auch gefallen

- MACR Project ReportDokument9 SeitenMACR Project ReportSrikanth Kumar KonduriNoch keine Bewertungen

- TCS Acquiring CMC: Project Report On MACR Submitted To: Prof. J. S. MatharuDokument22 SeitenTCS Acquiring CMC: Project Report On MACR Submitted To: Prof. J. S. MatharuAdithi VaishNoch keine Bewertungen

- 1 Retail Turnaround VFDokument8 Seiten1 Retail Turnaround VFTakudzwa S MupfurutsaNoch keine Bewertungen

- Turnaround StrategiesDokument2 SeitenTurnaround StrategiesIke Mag-away Gaamil100% (1)

- Valuation AssignmentDokument20 SeitenValuation AssignmentHw SolutionNoch keine Bewertungen

- Takeover & Acquisition: Mergers and Acquisitions and CRDokument11 SeitenTakeover & Acquisition: Mergers and Acquisitions and CROmkar PandeyNoch keine Bewertungen

- Case: IBM Corporation Turnaround: Presented By: Group 8Dokument13 SeitenCase: IBM Corporation Turnaround: Presented By: Group 8Karthik RamaduraiNoch keine Bewertungen

- Iflexppt 03Dokument33 SeitenIflexppt 03Chithra Lekha100% (1)

- Loan SalesDokument17 SeitenLoan SalesWILLY SETIAWANNoch keine Bewertungen

- Talbros Case PDFDokument16 SeitenTalbros Case PDFSoumik MalNoch keine Bewertungen

- Merger and AquisitionsDokument22 SeitenMerger and AquisitionsIshAkhterNoch keine Bewertungen

- Strategic DissonanceDokument29 SeitenStrategic DissonanceDamian Flori AlinaNoch keine Bewertungen

- Radnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Dokument22 SeitenRadnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Luisa FernandaNoch keine Bewertungen

- Attractive M&a Targets PART 1 v2Dokument24 SeitenAttractive M&a Targets PART 1 v2Aman SrivastavaNoch keine Bewertungen

- Private Equity Unchained: Strategy Insights for the Institutional InvestorVon EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNoch keine Bewertungen

- Zip Co Ltd. - Acquisition of QuadPay and Capital Raise (Z1P-AU)Dokument12 SeitenZip Co Ltd. - Acquisition of QuadPay and Capital Raise (Z1P-AU)JacksonNoch keine Bewertungen

- Case Study-Finance AssignmentDokument12 SeitenCase Study-Finance AssignmentMakshud ManikNoch keine Bewertungen

- Bectondickinsonpresentation 090910204604 Phpapp02Dokument23 SeitenBectondickinsonpresentation 090910204604 Phpapp02rohanfernsNoch keine Bewertungen

- Turnaround Strategy: DR Amit RangnekarDokument46 SeitenTurnaround Strategy: DR Amit RangnekarDr Amit RangnekarNoch keine Bewertungen

- Sony and Zee Ink Merger DealDokument2 SeitenSony and Zee Ink Merger DealMr PicaedNoch keine Bewertungen

- Syllabus E - Commerce: B-Com Vi Sem (Hons) Subject - E-CommerceDokument36 SeitenSyllabus E - Commerce: B-Com Vi Sem (Hons) Subject - E-CommerceSpatiha PathmanabanNoch keine Bewertungen

- Capital Structure: Financial DistressDokument22 SeitenCapital Structure: Financial DistressAniket KaushikNoch keine Bewertungen

- Maruti SuzukiDokument18 SeitenMaruti SuzukichandaNoch keine Bewertungen

- Maruti True ValueDokument7 SeitenMaruti True Valuedarshan1793Noch keine Bewertungen

- Wipro LimitedDokument4 SeitenWipro LimitedAnkitnautyNoch keine Bewertungen

- Lecture Notes Topic 6 Final PDFDokument109 SeitenLecture Notes Topic 6 Final PDFAnDy YiMNoch keine Bewertungen

- The Common Determinants of Merger and Acquisition SuccessDokument16 SeitenThe Common Determinants of Merger and Acquisition SuccessSi QinNoch keine Bewertungen

- Case1 - LEK Vs PWCDokument26 SeitenCase1 - LEK Vs PWCmayolgalloNoch keine Bewertungen

- Finanacial Restructuring 2Dokument48 SeitenFinanacial Restructuring 2Jim Mathilakathu100% (2)

- HP Sonos AccvDokument6 SeitenHP Sonos AccvDeepti AgarwalNoch keine Bewertungen

- Tinplate Company of IndiaDokument17 SeitenTinplate Company of IndiaZaheer NâqvîNoch keine Bewertungen

- Morgan Stanley: Ka Him NG Kevin Yu Eric Long Ming ChuDokument116 SeitenMorgan Stanley: Ka Him NG Kevin Yu Eric Long Ming ChuvaibhavNoch keine Bewertungen

- Lecture 5 - Shareholder's Equity AccountingDokument33 SeitenLecture 5 - Shareholder's Equity Accountingpeter kong100% (1)

- IAPM Selected NumericalsDokument18 SeitenIAPM Selected NumericalsPareen DesaiNoch keine Bewertungen

- Credit DerivativesDokument31 SeitenCredit DerivativesahmtyNoch keine Bewertungen

- Sapm - Fifth (5) Sem BBIDokument156 SeitenSapm - Fifth (5) Sem BBIRasesh ShahNoch keine Bewertungen

- Indian Financial SystemDokument163 SeitenIndian Financial SystemrohitravaliyaNoch keine Bewertungen

- Gujarat Ambuja Holcim DealDokument6 SeitenGujarat Ambuja Holcim DealkndhanushNoch keine Bewertungen

- Prachi Navghare, 29 ValuationDokument14 SeitenPrachi Navghare, 29 ValuationPrachi NavghareNoch keine Bewertungen

- Retail MarketingDokument235 SeitenRetail MarketingSaranya RagupathiNoch keine Bewertungen

- Essar Steel-Defaulting On Debt RepaymentDokument9 SeitenEssar Steel-Defaulting On Debt RepaymentSudani Ankit100% (1)

- IBM StrategyDokument17 SeitenIBM StrategydzunghvNoch keine Bewertungen

- Euro Zone Debt Crisis: RGCMS MMS II Year - FinanceDokument33 SeitenEuro Zone Debt Crisis: RGCMS MMS II Year - FinanceRahul Kadam100% (1)

- Hertz QuestionsDokument1 SeiteHertz Questionsianseow0% (1)

- SM Cycle 7 Session 4Dokument76 SeitenSM Cycle 7 Session 4OttilieNoch keine Bewertungen

- Arnab Roy Abhishek Mukherjee Anurag Rai Shauvik Ghosh Soumya C Pulak JainDokument15 SeitenArnab Roy Abhishek Mukherjee Anurag Rai Shauvik Ghosh Soumya C Pulak JainArnab RoyNoch keine Bewertungen

- Group2 F&O PDFDokument4 SeitenGroup2 F&O PDFTarushi BhatiaNoch keine Bewertungen

- Takeover Defenses: Ankit Singhal Ifmr GSBDokument20 SeitenTakeover Defenses: Ankit Singhal Ifmr GSBRavi JangidNoch keine Bewertungen

- BloombergDokument2 SeitenBloombergJosé IgnacioNoch keine Bewertungen

- Due Diligence: Prof Ashutosh Kumar Sinha IIM LucknowDokument10 SeitenDue Diligence: Prof Ashutosh Kumar Sinha IIM LucknowCHINMAY JAINNoch keine Bewertungen

- Financial Distress, Bankruptcy and ReorganizationDokument41 SeitenFinancial Distress, Bankruptcy and ReorganizationYap Shoon EuNoch keine Bewertungen

- Zee-Sony Merger - Zee-Sony Merged Entity To Be Number One Player in Entertainment Space - Ashwin Patil - The Economic TimesDokument2 SeitenZee-Sony Merger - Zee-Sony Merged Entity To Be Number One Player in Entertainment Space - Ashwin Patil - The Economic TimesPratyayNoch keine Bewertungen

- Lecture 4 - ReformattingDokument31 SeitenLecture 4 - ReformattingnopeNoch keine Bewertungen

- Bond Problem - Fixed Income ValuationDokument1 SeiteBond Problem - Fixed Income ValuationAbhishek Garg0% (2)

- IBMDokument15 SeitenIBMAkshay MinhasNoch keine Bewertungen

- UVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentDokument14 SeitenUVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentKumarNoch keine Bewertungen

- Mergers and AcquisitionsDokument10 SeitenMergers and AcquisitionsHarpreet ChawlaNoch keine Bewertungen

- Valuation Final PPT 2015Dokument48 SeitenValuation Final PPT 2015roopesh gowdaNoch keine Bewertungen

- LTCMDokument6 SeitenLTCMAditya MaheshwariNoch keine Bewertungen

- BMA 12e PPT Ch13 16 PDFDokument68 SeitenBMA 12e PPT Ch13 16 PDFLuu ParrondoNoch keine Bewertungen

- 1035 Karnani OLDDokument32 Seiten1035 Karnani OLDdhingaraj20051858Noch keine Bewertungen

- Requirements For CADokument5 SeitenRequirements For CAKunwar Shivpal SinghNoch keine Bewertungen

- GICS (Global Industry Classification Standard) : Effective After Close of Business (US, EST) Wednesday June 30, 2010Dokument13 SeitenGICS (Global Industry Classification Standard) : Effective After Close of Business (US, EST) Wednesday June 30, 2010dhingaraj20051858Noch keine Bewertungen

- Yoga Sutras InterpretiveDokument63 SeitenYoga Sutras InterpretiveAshish Mangalampalli100% (1)

- Yoga Sutras of PatanjaliDokument333 SeitenYoga Sutras of PatanjaliGheorghe Paul100% (5)

- Hatha Yoga Pradipika PDFDokument102 SeitenHatha Yoga Pradipika PDFlovablesagi100% (1)

- Indian Economy AnalysisDokument18 SeitenIndian Economy Analysisdhingaraj20051858Noch keine Bewertungen

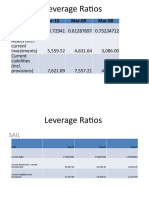

- Leverage Ratios: Year Mar-10 Mar-09 Mar-08Dokument6 SeitenLeverage Ratios: Year Mar-10 Mar-09 Mar-08dhingaraj20051858Noch keine Bewertungen

- Components of A Set of Financial Statements:: 1. Fair Presentation and Compliance With PFRSDokument7 SeitenComponents of A Set of Financial Statements:: 1. Fair Presentation and Compliance With PFRSFiona Mirasol P. BeroyNoch keine Bewertungen

- Worksheet 1.1 Introducing AccountingDokument3 SeitenWorksheet 1.1 Introducing AccountingKenshin HayashiNoch keine Bewertungen

- CFA Level 1 FRADokument17 SeitenCFA Level 1 FRAAkash KaleNoch keine Bewertungen

- 2016 Vol 1 CH 9 AnswersDokument3 Seiten2016 Vol 1 CH 9 Answersma quenaNoch keine Bewertungen

- Ch.1 FrameworkDokument30 SeitenCh.1 FrameworkPritam PaulNoch keine Bewertungen

- Business Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Dokument18 SeitenBusiness Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Dearla Bitoon100% (5)

- Chapter 1: The Accountant'S Role in The Organization: True/FalseDokument9 SeitenChapter 1: The Accountant'S Role in The Organization: True/FalseSittie Ainna A. UnteNoch keine Bewertungen

- KLBFDokument2 SeitenKLBFKhaerudin RangersNoch keine Bewertungen

- Components of An Interim Financial ReportDokument7 SeitenComponents of An Interim Financial ReportBedria Nari50% (2)

- Exercise 4 Shareholders EquityDokument9 SeitenExercise 4 Shareholders EquityNimfa SantiagoNoch keine Bewertungen

- ReceivablesDokument20 SeitenReceivablesGemmalyn FolguerasNoch keine Bewertungen

- 1 - Nvidia Pitch ReportDokument4 Seiten1 - Nvidia Pitch Reportapi-475759227Noch keine Bewertungen

- Breadtalk Group LTD: Singapore Company GuideDokument14 SeitenBreadtalk Group LTD: Singapore Company GuideCleoNoch keine Bewertungen

- Consoliated Group Financial Report - Jane Lazar CHP 12.1Dokument1 SeiteConsoliated Group Financial Report - Jane Lazar CHP 12.1Ng GraceNoch keine Bewertungen

- Abhijit Jadhav MBA 21826 2021-23Dokument66 SeitenAbhijit Jadhav MBA 21826 2021-23gawalianiket59Noch keine Bewertungen

- Quiz - IntangiblesDokument1 SeiteQuiz - IntangiblesAna Mae HernandezNoch keine Bewertungen

- Answers To Activity 1Dokument5 SeitenAnswers To Activity 1jangjangNoch keine Bewertungen

- Financial Statement: Unit-IiiDokument18 SeitenFinancial Statement: Unit-IiiRamesh RengarajanNoch keine Bewertungen

- Taking The Big Leap To Success: Performance Highlights Performance HighlightsDokument3 SeitenTaking The Big Leap To Success: Performance Highlights Performance Highlightspkj009Noch keine Bewertungen

- QUIZ 6 Joint ArrangementDokument2 SeitenQUIZ 6 Joint ArrangementEki SunriseNoch keine Bewertungen

- Formula SheetDokument1 SeiteFormula SheetNikhil TodiNoch keine Bewertungen

- Final Examination in Accounting For Business CombinationDokument9 SeitenFinal Examination in Accounting For Business CombinationJasmin Dela CruzNoch keine Bewertungen

- DipIFR D24-J25 Syllabus and Study Guide - FinalDokument15 SeitenDipIFR D24-J25 Syllabus and Study Guide - FinalFrans R. Calderon MendozaNoch keine Bewertungen

- Cfas MidtermDokument38 SeitenCfas MidtermBruce SolanoNoch keine Bewertungen

- Accounting Cycle Practice Problem - Final ExamDokument2 SeitenAccounting Cycle Practice Problem - Final ExamAMNEERA SHANIA LALANTONoch keine Bewertungen

- Solutions Manual: 1st EditionDokument29 SeitenSolutions Manual: 1st EditionJunior Waqairasari100% (3)

- All Ratio FormulasDokument44 SeitenAll Ratio FormulasNikhilNoch keine Bewertungen

- Borrowing Costs NotesDokument2 SeitenBorrowing Costs NotesMariella Olympia PanuncialesNoch keine Bewertungen

- 3 - Discussion - Joint Products and ByproductsDokument2 Seiten3 - Discussion - Joint Products and ByproductsCharles TuazonNoch keine Bewertungen

- Acc105 RevaluationDokument20 SeitenAcc105 RevaluationMaybelleNoch keine Bewertungen