Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Obtain An Understanding of The Customer's Key Business Processes Define The Client's Organization Structure in SAP Based On Those Business ProcessesDokument60 SeitenObtain An Understanding of The Customer's Key Business Processes Define The Client's Organization Structure in SAP Based On Those Business ProcessesvkpandareNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Topic #1: Forecasting Financial Statements and Free Cash FlowsDokument14 SeitenTopic #1: Forecasting Financial Statements and Free Cash FlowsJo JohnstonNoch keine Bewertungen

- Mba ReportDokument89 SeitenMba ReportRiddhi KakkadNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Getalado, Jericho M.Dokument18 SeitenGetalado, Jericho M.Ruth Getalado0% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- 67-2-1 AccountancyDokument27 Seiten67-2-1 AccountancytejNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- INFY - PL - 29 AugDokument6 SeitenINFY - PL - 29 AuganjugaduNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Overview of Sarfaesi Act, 2002Dokument8 SeitenOverview of Sarfaesi Act, 2002Pragati OjhaNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Financial Statements, Cash Flow, and TaxesDokument8 SeitenFinancial Statements, Cash Flow, and TaxesRaihan Eibna RezaNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Marketing Consulting Business PlanDokument33 SeitenMarketing Consulting Business PlanMohamed Salah El Din100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- W8 TutorialSolutionsDokument12 SeitenW8 TutorialSolutionsCJNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Fundamental Analysis Project.Dokument82 SeitenFundamental Analysis Project.Ajay Rockson100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- (PWC) Up Jpia Asset Audit Case Xyz Retail CompanyDokument7 Seiten(PWC) Up Jpia Asset Audit Case Xyz Retail CompanyJoyce BelenNoch keine Bewertungen

- Finance and AccountingDokument143 SeitenFinance and Accountingrt222250% (2)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- ACC XI SEE QP For RevisionDokument31 SeitenACC XI SEE QP For Revisionvarshitha reddyNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- CA Foundation Accounts Recodring of Transactions StudentsDokument57 SeitenCA Foundation Accounts Recodring of Transactions StudentsRockyNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Sub Accountancy: Class XIDokument3 SeitenSub Accountancy: Class XIJanvi Singh RajputNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- JAIIB AFM Module B Financial Statements and Core Banking SystemsDokument61 SeitenJAIIB AFM Module B Financial Statements and Core Banking SystemsGaurav MishraNoch keine Bewertungen

- Asset Accounting Interview QuestionsDokument12 SeitenAsset Accounting Interview QuestionsvinayNoch keine Bewertungen

- Ind As 103Dokument45 SeitenInd As 103Kshitija JoshiNoch keine Bewertungen

- Multiple Cholce Questions MCQ) ) : Brand ValueDokument14 SeitenMultiple Cholce Questions MCQ) ) : Brand ValueHarmohandeep singh100% (1)

- Solution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 13th Edition by StickneyDokument32 SeitenSolution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 13th Edition by Stickneya540142314Noch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Work Sheet AnalysisDokument7 SeitenWork Sheet AnalysisMUHAMMAD ARIF BASHIRNoch keine Bewertungen

- Annamalai University: Accounting For Managerial DecisionsDokument306 SeitenAnnamalai University: Accounting For Managerial DecisionsMALU_BOBBYNoch keine Bewertungen

- Cash Flow Statement 2016-2020Dokument8 SeitenCash Flow Statement 2016-2020yip manNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Accounting Equation Problems and SolutionDokument7 SeitenAccounting Equation Problems and SolutionNilrose EscartinNoch keine Bewertungen

- Notes-INTERM 2-Module 4-Depletion of Natural ResourcesDokument3 SeitenNotes-INTERM 2-Module 4-Depletion of Natural ResourcesLeonoramarie BernosNoch keine Bewertungen

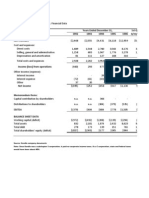

- Exhibit 1 Kendle International Inc. Financial Data Years Ended December 31Dokument12 SeitenExhibit 1 Kendle International Inc. Financial Data Years Ended December 31Kito Minying ChenNoch keine Bewertungen

- Fundamentals of Accountancy, Business, and Management 2Dokument31 SeitenFundamentals of Accountancy, Business, and Management 2Honey ShenNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Training Hand Out - Economic Evaluation and Modeling of Mining ProjectsDokument73 SeitenTraining Hand Out - Economic Evaluation and Modeling of Mining ProjectsAriyanto WibowoNoch keine Bewertungen

- Axis Enam MergerDokument9 SeitenAxis Enam MergernnsriniNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)