Das könnte Ihnen auch gefallen

- MODULE 6A Home Office and Branch AccountingDokument14 SeitenMODULE 6A Home Office and Branch AccountingmcespressoblendNoch keine Bewertungen

- Lesson 15 Home Office, Branch and Agency AccountingDokument11 SeitenLesson 15 Home Office, Branch and Agency AccountingMark TaysonNoch keine Bewertungen

- Home Office and Branch Accounting (HOBA) With Sample Problems, Solutions and ExplanationsDokument16 SeitenHome Office and Branch Accounting (HOBA) With Sample Problems, Solutions and ExplanationsKathleene50% (2)

- Module - Accounting For Business CombinationDokument16 SeitenModule - Accounting For Business CombinationRJ Kristine DaqueNoch keine Bewertungen

- Module 317 - Accounting For Business CombinationDokument48 SeitenModule 317 - Accounting For Business CombinationRJ Kristine DaqueNoch keine Bewertungen

- 1 AccountingforAgencyHomeOfficeandBranchOfficeDokument10 Seiten1 AccountingforAgencyHomeOfficeandBranchOfficenonen3872Noch keine Bewertungen

- ACC5116 - Module 1Dokument6 SeitenACC5116 - Module 1Carl Dhaniel Garcia SalenNoch keine Bewertungen

- p2 - Guerrero Ch7Dokument35 Seitenp2 - Guerrero Ch7JerichoPedragosa66% (38)

- ACC132 - Home Office and Branch Accounting PDFDokument50 SeitenACC132 - Home Office and Branch Accounting PDFRolando G. Cua Jr.92% (12)

- Home Office & Branch AccountingDokument13 SeitenHome Office & Branch AccountingGround ZeroNoch keine Bewertungen

- Advanced Accounting (ACT 410)Dokument58 SeitenAdvanced Accounting (ACT 410)Amr Amr Adel Ahmed MaamounNoch keine Bewertungen

- Home and Branch Accounting General ProceduresDokument30 SeitenHome and Branch Accounting General ProceduresCleah WaskinNoch keine Bewertungen

- 11 Home Office and BranchDokument3 Seiten11 Home Office and BranchabcdefgNoch keine Bewertungen

- Home Office - Branch and Agency AccountingDokument30 SeitenHome Office - Branch and Agency AccountingJenina Diaz82% (11)

- Module 3 - Home Office Brancg Acctg Part 1Dokument13 SeitenModule 3 - Home Office Brancg Acctg Part 1May P. Huit100% (1)

- Uloa. Understand The Entries To Record Agency and Branch TransactionsDokument20 SeitenUloa. Understand The Entries To Record Agency and Branch Transactionsalmira garciaNoch keine Bewertungen

- Advacc Mod1Dokument23 SeitenAdvacc Mod1robNoch keine Bewertungen

- AFAR2 - Sales Agency, H.O., & Branch AccountingDokument18 SeitenAFAR2 - Sales Agency, H.O., & Branch AccountingVon Andrei MedinaNoch keine Bewertungen

- ACP 312 HO 1.1 Accounting For AgenciesDokument3 SeitenACP 312 HO 1.1 Accounting For AgenciesDelsey SerephinaNoch keine Bewertungen

- Home Office & Branch AccountingDokument15 SeitenHome Office & Branch AccountingKenneth NinalgaNoch keine Bewertungen

- AFAR2 - Sales Agency, H.O., & Branch AccountingDokument12 SeitenAFAR2 - Sales Agency, H.O., & Branch AccountingjajajaredredNoch keine Bewertungen

- Lesson 4 Accounting For Home OfficeDokument8 SeitenLesson 4 Accounting For Home OfficeheyheyNoch keine Bewertungen

- Home Office, Branches and AgenciesDokument5 SeitenHome Office, Branches and AgenciesBryan ReyesNoch keine Bewertungen

- Advanced FA All Chapters Teaching MaterialDokument58 SeitenAdvanced FA All Chapters Teaching MaterialKirub WerqeNoch keine Bewertungen

- Home Office and Branch Accounting Special ProblemsDokument27 SeitenHome Office and Branch Accounting Special ProblemsAnna Marie Alferez80% (5)

- Advanced FA I - Chapter 02, BranchesDokument137 SeitenAdvanced FA I - Chapter 02, BranchesUtban AshabNoch keine Bewertungen

- Chapter 4 Branch Accounting@editedDokument18 SeitenChapter 4 Branch Accounting@editedsamuel debebeNoch keine Bewertungen

- Home Office, Agency and Branch AccountingDokument17 SeitenHome Office, Agency and Branch AccountingPaupauNoch keine Bewertungen

- Branches Latest ChapterDokument138 SeitenBranches Latest ChapterMenber MulatNoch keine Bewertungen

- HOBA - General Procedures-DLSAUDokument25 SeitenHOBA - General Procedures-DLSAUJasmine LimNoch keine Bewertungen

- HOBA - SeatworkDokument2 SeitenHOBA - Seatworkahyenn cabelloNoch keine Bewertungen

- Ibro Answer 1Dokument4 SeitenIbro Answer 1Abdi Mucee TubeNoch keine Bewertungen

- Chapter 4 Branch AccountingDokument31 SeitenChapter 4 Branch AccountingAkkamaNoch keine Bewertungen

- Chapter 4 Branch AccountingDokument17 SeitenChapter 4 Branch Accountingkefyalew TNoch keine Bewertungen

- 4 Home Office Agency Handout SolutionDokument15 Seiten4 Home Office Agency Handout SolutionRyan CornistaNoch keine Bewertungen

- Lesson 1 Home Office and Branch AccountingDokument4 SeitenLesson 1 Home Office and Branch AccountingAndy Lalu100% (3)

- Accounting for Agency & BranchDokument16 SeitenAccounting for Agency & BranchDawit AmahaNoch keine Bewertungen

- Home Office and Branch AccountingDokument2 SeitenHome Office and Branch AccountingMae TndnNoch keine Bewertungen

- APrE04 01E Home-Office and BranchDokument6 SeitenAPrE04 01E Home-Office and BranchMendoza Ron NixonNoch keine Bewertungen

- Home Office, Agency and Branch AccountingDokument17 SeitenHome Office, Agency and Branch AccountingRain LerogNoch keine Bewertungen

- M1 - Home Office and Branch Accounting - General ProceduresDokument15 SeitenM1 - Home Office and Branch Accounting - General ProceduresJohn Michael A. PaclibareNoch keine Bewertungen

- Chapter 5Dokument137 SeitenChapter 5Lakachew GetasewNoch keine Bewertungen

- Home Office and Bracnch - Special ProblemsDokument22 SeitenHome Office and Bracnch - Special ProblemsYeshi Soo YahNoch keine Bewertungen

- Consignment & Sales AgencyDokument4 SeitenConsignment & Sales AgencydarlenexjoyceNoch keine Bewertungen

- Accounting For Decentralized Operations: Inventory at Cost of P40,000Dokument6 SeitenAccounting For Decentralized Operations: Inventory at Cost of P40,000Nicole Allyson AguantaNoch keine Bewertungen

- Branch AccountingDokument78 SeitenBranch AccountingleolionaryaNoch keine Bewertungen

- Accounting for Agencies, Branches & Home OfficesDokument30 SeitenAccounting for Agencies, Branches & Home OfficesYalew WondmnewNoch keine Bewertungen

- B326 Accounting For Branches - Summer 2020Dokument14 SeitenB326 Accounting For Branches - Summer 2020Kennedy OnyangoNoch keine Bewertungen

- Materi Lab 1 - HoboDokument4 SeitenMateri Lab 1 - HoboMuhamad Rizki PratamaNoch keine Bewertungen

- Billed price calculations for home office and branch shipmentsDokument4 SeitenBilled price calculations for home office and branch shipmentsJohnmichael Coroza0% (1)

- ECU TOPIC ONE BranchesDokument7 SeitenECU TOPIC ONE BranchesPinky RoseNoch keine Bewertungen

- Branch Accounting - ICMAIDokument51 SeitenBranch Accounting - ICMAIdbNoch keine Bewertungen

- HO, B & A AcctgDokument15 SeitenHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- Home Office & Branch Lecture NotesDokument32 SeitenHome Office & Branch Lecture NotesDrehfcieNoch keine Bewertungen

- Home Office, Branch and Agency AccountingDokument26 SeitenHome Office, Branch and Agency AccountingMarion MalabananNoch keine Bewertungen

- Questions On ALOBIDokument1 SeiteQuestions On ALOBILabLab ChattoNoch keine Bewertungen

- HOB ProblemsDokument2 SeitenHOB ProblemshyosungloverNoch keine Bewertungen

- Home Office, Branch, and Agency AccountingDokument48 SeitenHome Office, Branch, and Agency AccountingCHERYL MORADANoch keine Bewertungen

- Solution Chapter 16Dokument90 SeitenSolution Chapter 16Frances Chariz YbioNoch keine Bewertungen

- Problem 1Dokument1 SeiteProblem 1Frances Chariz Ybio100% (1)

- Ways To Improve Communication SkillsDokument1 SeiteWays To Improve Communication SkillsFrances Chariz YbioNoch keine Bewertungen

- Home Office and Branch Accounting General ProceduresDokument2 SeitenHome Office and Branch Accounting General ProceduresFrances Chariz YbioNoch keine Bewertungen

- Partnerships AccountsDokument133 SeitenPartnerships AccountsNadeem ManzoorNoch keine Bewertungen

- FADM Cheat Sheet ToolsDokument2 SeitenFADM Cheat Sheet Toolsvarun022084Noch keine Bewertungen

- Exercise 2 - Operating Cycle and Cash Conversion Cycle (Not Graded)Dokument9 SeitenExercise 2 - Operating Cycle and Cash Conversion Cycle (Not Graded)Van Errl Nicolai SantosNoch keine Bewertungen

- AR and Sales Audit ProgramDokument10 SeitenAR and Sales Audit ProgramHarold Dan AcebedoNoch keine Bewertungen

- Sowmya FinalDokument48 SeitenSowmya Finalnagarajan sNoch keine Bewertungen

- PT. COOLINDO PURCHASES, SALES AND CASH RECEIPTS JOURNALSDokument29 SeitenPT. COOLINDO PURCHASES, SALES AND CASH RECEIPTS JOURNALSAnisaa Okta100% (5)

- Step 1 - Introduzca información sobre su empresaDokument36 SeitenStep 1 - Introduzca información sobre su empresaSamuel FLoresNoch keine Bewertungen

- For Confirmations After The First Response IsDokument6 SeitenFor Confirmations After The First Response IsRin ZhafiraaNoch keine Bewertungen

- Study Guide-Final Exam-Revised-1Dokument23 SeitenStudy Guide-Final Exam-Revised-1KhayHninsNoch keine Bewertungen

- Horniman Horticulture CaseDokument2 SeitenHorniman Horticulture CaseVinny Tuteja0% (1)

- Question No. 2: Module 6: Discussion 1Dokument4 SeitenQuestion No. 2: Module 6: Discussion 1Camille BonaguaNoch keine Bewertungen

- TB Understanding Financial Statements 11ge Lyn M. FraserDokument85 SeitenTB Understanding Financial Statements 11ge Lyn M. Fraseremanmamdouh596Noch keine Bewertungen

- OLAP in Dynamics AX 4 - Installing and Configuring Analysis ServicesDokument9 SeitenOLAP in Dynamics AX 4 - Installing and Configuring Analysis ServicesCarolina Correa PadolinaNoch keine Bewertungen

- Determine working capital policies ROI and cash conversion cyclesDokument2 SeitenDetermine working capital policies ROI and cash conversion cyclesGreys Maddawat MasulaNoch keine Bewertungen

- 003 ExDokument14 Seiten003 ExanandhuNoch keine Bewertungen

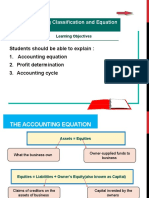

- Accounting Equation and Profit DeterminationDokument19 SeitenAccounting Equation and Profit DeterminationNor LailyNoch keine Bewertungen

- FIN081 P3 Quiz2 Short-Term-Financing AnswerDokument4 SeitenFIN081 P3 Quiz2 Short-Term-Financing AnswerMary Lyn DatuinNoch keine Bewertungen

- PSK Assurance NoteDokument20 SeitenPSK Assurance NoteNTurin1435100% (1)

- JPIA Financial Accounting 1 (Prelims)Dokument20 SeitenJPIA Financial Accounting 1 (Prelims)Pauline Kisha CastroNoch keine Bewertungen

- Chapter 6-Exercise SetDokument23 SeitenChapter 6-Exercise SetNatalie JimenezNoch keine Bewertungen

- CH 23Dokument92 SeitenCH 23Erin Heizyk100% (1)

- University Budgeting and Production PlanningDokument14 SeitenUniversity Budgeting and Production PlanningJenelyn UbananNoch keine Bewertungen

- Managing Current Assets and Liabilities for Business LiquidityDokument26 SeitenManaging Current Assets and Liabilities for Business Liquiditysandsoni2002Noch keine Bewertungen

- Working Capital ManagementDokument7 SeitenWorking Capital ManagementIsmail MarzukiNoch keine Bewertungen

- ACCA F9 Financial Management Notes Summary CDokument76 SeitenACCA F9 Financial Management Notes Summary CAshfaq Ul Haq OniNoch keine Bewertungen

- Gazprom Ifrs 2014 12m enDokument68 SeitenGazprom Ifrs 2014 12m ensimosNoch keine Bewertungen

- GPA Holdings' Board Independence RiskDokument31 SeitenGPA Holdings' Board Independence RiskEileen WongNoch keine Bewertungen

- Chapter 7 (II) - Current Asset ManagementDokument23 SeitenChapter 7 (II) - Current Asset ManagementhendraxyzxyzNoch keine Bewertungen

- Current Liabilities ManagementDokument7 SeitenCurrent Liabilities ManagementJack Herer100% (1)

- Peach Blossom Cologne Company b5Dokument1 SeitePeach Blossom Cologne Company b5lalaNoch keine Bewertungen