Das könnte Ihnen auch gefallen

- Vivos Based On Pure Act of Liberality Without Any or Less Than Adequate Consideration and Without AnyDokument5 SeitenVivos Based On Pure Act of Liberality Without Any or Less Than Adequate Consideration and Without AnyJunivenReyUmadhayNoch keine Bewertungen

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Von EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Noch keine Bewertungen

- Donor's Tax A) Basic Principles, Concept and DefinitionDokument4 SeitenDonor's Tax A) Basic Principles, Concept and DefinitionAnonymous YNTVcDNoch keine Bewertungen

- 1040 Exam Prep: Module II - Basic Tax ConceptsVon Everand1040 Exam Prep: Module II - Basic Tax ConceptsBewertung: 1.5 von 5 Sternen1.5/5 (2)

- 24 Pirovano v. CIR (14 SCRA 232)Dokument8 Seiten24 Pirovano v. CIR (14 SCRA 232)Perry YapNoch keine Bewertungen

- Donor's TaxDokument5 SeitenDonor's TaxKeithNoch keine Bewertungen

- CHAPTER II-Donorrs TaxDokument5 SeitenCHAPTER II-Donorrs TaxShiela May Agustin MacarayanNoch keine Bewertungen

- Donor's TaxDokument25 SeitenDonor's TaxMark Erick Acojido RetonelNoch keine Bewertungen

- BA 128 2 Donor's TaxDokument5 SeitenBA 128 2 Donor's TaxEyriel CoNoch keine Bewertungen

- Donor's TaxDokument19 SeitenDonor's TaxMark CanoNoch keine Bewertungen

- Basic Concept of Donation and Donor's TaxDokument20 SeitenBasic Concept of Donation and Donor's TaxKarl BasaNoch keine Bewertungen

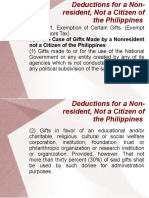

- B) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesDokument23 SeitenB) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesNissi JonnaNoch keine Bewertungen

- Taxation I Assignment: Chapter 2 (C To F) DefinitionsDokument4 SeitenTaxation I Assignment: Chapter 2 (C To F) DefinitionsMarvin H. Taleon IINoch keine Bewertungen

- Module 1 Lesson 4Dokument4 SeitenModule 1 Lesson 4Rich Ann Redondo VillanuevaNoch keine Bewertungen

- A Requirement On Management, Tax and Consultancy: Cyrra Q. Balignasay BSA-5Dokument14 SeitenA Requirement On Management, Tax and Consultancy: Cyrra Q. Balignasay BSA-5Cyrra BalignasayNoch keine Bewertungen

- Donor's TaxDokument15 SeitenDonor's TaxMary Fatima LiganNoch keine Bewertungen

- Module 1 - Lesson 1 - Administrative Provisions and Fundamental Concepts of Donor's TaxationDokument4 SeitenModule 1 - Lesson 1 - Administrative Provisions and Fundamental Concepts of Donor's Taxationohmyme sungjaeNoch keine Bewertungen

- Govern The Imposition of The Donor's TaxDokument5 SeitenGovern The Imposition of The Donor's TaxjuliNoch keine Bewertungen

- TAX BSA Group 9 Page 348 362Dokument3 SeitenTAX BSA Group 9 Page 348 362JerricaRamaNoch keine Bewertungen

- Reviewer On Intro To TaxDokument7 SeitenReviewer On Intro To Taxjulius art maputiNoch keine Bewertungen

- Frequently Asked QuestionsDokument4 SeitenFrequently Asked QuestionsMV FadsNoch keine Bewertungen

- Transfer Taxes: Atty. Kim M. Aranas Faculty, USC-SOLGDokument61 SeitenTransfer Taxes: Atty. Kim M. Aranas Faculty, USC-SOLGethel hyugaNoch keine Bewertungen

- Module 4. Donors Tax-Gross Gifts, Examptions and Tax RatesDokument5 SeitenModule 4. Donors Tax-Gross Gifts, Examptions and Tax RatesYolly DiazNoch keine Bewertungen

- Taxation Reviewer Taxation:: Estate TaxDokument7 SeitenTaxation Reviewer Taxation:: Estate TaxKit OsillosNoch keine Bewertungen

- Bir Donors Tax QueriesDokument2 SeitenBir Donors Tax QueriesdteroseNoch keine Bewertungen

- Transfer Taxes: Donor'S TaxDokument8 SeitenTransfer Taxes: Donor'S TaxracrabeNoch keine Bewertungen

- Estate and Donor's TaxDokument6 SeitenEstate and Donor's TaxKimberly SendinNoch keine Bewertungen

- SEC. 98. Imposition of TaxDokument15 SeitenSEC. 98. Imposition of TaxAybern BawtistaNoch keine Bewertungen

- Donor's TaxDokument8 SeitenDonor's TaxRenalyn GardeNoch keine Bewertungen

- Donor's Tax - BirDokument7 SeitenDonor's Tax - BirHannah Brynne UrreraNoch keine Bewertungen

- DONOR's TaxDokument4 SeitenDONOR's TaxAnne Elamparo50% (4)

- Questions and Answers On Philippine Donor's TaxDokument4 SeitenQuestions and Answers On Philippine Donor's TaxBlesilda OracoyNoch keine Bewertungen

- Estate TaxDokument26 SeitenEstate Taxkitayroselyn4Noch keine Bewertungen

- Business Taxation Part 1Dokument5 SeitenBusiness Taxation Part 1Rich Ann Redondo VillanuevaNoch keine Bewertungen

- Notes To Transfer Taxes Under TRAIN LawDokument7 SeitenNotes To Transfer Taxes Under TRAIN LawDustin PascuaNoch keine Bewertungen

- Donors TaxDokument19 SeitenDonors TaxIo AyaNoch keine Bewertungen

- CARL ANDREW Assignment Tax 102Dokument7 SeitenCARL ANDREW Assignment Tax 102Carl Andrew Aborquez Arcinal0% (1)

- Tax FinalsDokument30 SeitenTax FinalsJennie KimNoch keine Bewertungen

- Transfer Taxation: Estate Taxation: CDD In-House CPA Review Rex B. Banggawan, CPA, MBA TaxationDokument14 SeitenTransfer Taxation: Estate Taxation: CDD In-House CPA Review Rex B. Banggawan, CPA, MBA TaxationAnonymous l13WpzNoch keine Bewertungen

- Donors TaxDokument8 SeitenDonors Taxmaxine claire cutingNoch keine Bewertungen

- Donor's TaxDokument29 SeitenDonor's TaxPETERWILLE CHUANoch keine Bewertungen

- Estate TaxDokument13 SeitenEstate TaxJeriane Carissa DigaNoch keine Bewertungen

- Ch08 Donor's TaxDokument8 SeitenCh08 Donor's TaxHazel CruzNoch keine Bewertungen

- 2donor's Tax LectureDokument23 Seiten2donor's Tax LectureJohn Paulo CalubNoch keine Bewertungen

- Jessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstateDokument8 SeitenJessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstatejessaNoch keine Bewertungen

- Estate Tax and Donors TaxDokument19 SeitenEstate Tax and Donors Taxtalla aldover100% (1)

- BIR - DONOR'S TaxDokument5 SeitenBIR - DONOR'S TaxKim EspinaNoch keine Bewertungen

- Tax2 - Estate Donors VAT ReviewerDokument3 SeitenTax2 - Estate Donors VAT ReviewercardeguzmanNoch keine Bewertungen

- Chapter 2 - Donor's Tax (Notes)Dokument8 SeitenChapter 2 - Donor's Tax (Notes)Angela Denisse FranciscoNoch keine Bewertungen

- TAXATIONDokument9 SeitenTAXATIONkekadiegoNoch keine Bewertungen

- Transfer TaxesDokument101 SeitenTransfer TaxesAngelo IvanNoch keine Bewertungen

- CHAPTER 6 - Donor's Tax ReportDokument58 SeitenCHAPTER 6 - Donor's Tax ReportheyheyNoch keine Bewertungen

- Exemptions and Exclusions TaxDokument5 SeitenExemptions and Exclusions TaxJade RogieNoch keine Bewertungen

- Effective January 1, 2018 and Onwards (Republic Act (RA) No. 10963/TRAIN)Dokument3 SeitenEffective January 1, 2018 and Onwards (Republic Act (RA) No. 10963/TRAIN)Deneb DoydoraNoch keine Bewertungen

- Nature of Transfer TaxesDokument2 SeitenNature of Transfer TaxesColleen ArcosNoch keine Bewertungen

- Donor's Tax ReviewerDokument6 SeitenDonor's Tax ReviewerMaria Victoria75% (4)

- Module 3 Donor's Tax (Part 1)Dokument39 SeitenModule 3 Donor's Tax (Part 1)Venice Marie ArroyoNoch keine Bewertungen

- Ch10 Donor's TaxDokument9 SeitenCh10 Donor's TaxRenelyn FiloteoNoch keine Bewertungen

- TX12 - Estate TaxDokument14 SeitenTX12 - Estate TaxPatrick Kyle AgraviadorNoch keine Bewertungen

- Nature of Vat, "In The Course of Trade/Business"Dokument7 SeitenNature of Vat, "In The Course of Trade/Business"Ziad DnetNoch keine Bewertungen

- Del RosarioDokument5 SeitenDel RosarioZiad DnetNoch keine Bewertungen

- Omnibus Election CodeDokument74 SeitenOmnibus Election CodeZiad DnetNoch keine Bewertungen

- Puig v. PenafloridaDokument3 SeitenPuig v. PenafloridaZiad DnetNoch keine Bewertungen

- G.R. No. L-29204 December 29, 1928 RUFINA ZAPANTA, ET AL., Plaintiffs-Appellees, JUAN POSADAS, JR., ET AL., Defendants-AppellantsDokument4 SeitenG.R. No. L-29204 December 29, 1928 RUFINA ZAPANTA, ET AL., Plaintiffs-Appellees, JUAN POSADAS, JR., ET AL., Defendants-AppellantsZiad DnetNoch keine Bewertungen

- Del RosarioDokument5 SeitenDel RosarioZiad DnetNoch keine Bewertungen

- Civil Law Forecast by Atty. Jumrani 2022Dokument5 SeitenCivil Law Forecast by Atty. Jumrani 2022Ziad DnetNoch keine Bewertungen

- Banking Law CasesDokument61 SeitenBanking Law CasesZiad DnetNoch keine Bewertungen

- Digest Case Banking LawsDokument1 SeiteDigest Case Banking LawsZiad DnetNoch keine Bewertungen

- Banking Law CasesDokument20 SeitenBanking Law CasesZiad DnetNoch keine Bewertungen

- Banking Laws QuestionDokument2 SeitenBanking Laws QuestionZiad DnetNoch keine Bewertungen

- Ipl Cases 2Dokument281 SeitenIpl Cases 2Ziad Dnet100% (1)

- BOC 2015 Civil Law Reviewer (Final)Dokument602 SeitenBOC 2015 Civil Law Reviewer (Final)Joshua Laygo Sengco88% (17)

- B 1 Judicial Afffidavit Andy LimDokument8 SeitenB 1 Judicial Afffidavit Andy LimZiad DnetNoch keine Bewertungen

- Chart Template 16x9Dokument5 SeitenChart Template 16x9Ziad DnetNoch keine Bewertungen

- Banking Law CasesDokument39 SeitenBanking Law CasesZiad DnetNoch keine Bewertungen

- Contract of Sale Motor VehicleDokument3 SeitenContract of Sale Motor VehicleZiad Dnet100% (1)

- Agreement On Contract To SaleDokument12 SeitenAgreement On Contract To SaleZiad DnetNoch keine Bewertungen

- Corporation Law Notes Under Atty. Ladia (Revised)Dokument73 SeitenCorporation Law Notes Under Atty. Ladia (Revised)yumiganda91% (11)

- Answers To Bar: Remedial Law Bar Examination Q & A (1997-2006Dokument51 SeitenAnswers To Bar: Remedial Law Bar Examination Q & A (1997-2006Ziad DnetNoch keine Bewertungen

- Contract of Sale Motor VehicleDokument3 SeitenContract of Sale Motor VehicleZiad DnetNoch keine Bewertungen

- Traning Development PPT 2Dokument18 SeitenTraning Development PPT 2Ziad DnetNoch keine Bewertungen

- Contract of Sale Motor VehicleDokument3 SeitenContract of Sale Motor VehicleZiad DnetNoch keine Bewertungen

- The Corporation Code of The Philippines PDFDokument85 SeitenThe Corporation Code of The Philippines PDFDawn BarondaNoch keine Bewertungen

- Land Sale ContractDokument3 SeitenLand Sale ContractZiad DnetNoch keine Bewertungen

- Different Types of CommDokument23 SeitenDifferent Types of CommZiad DnetNoch keine Bewertungen

- Case Digests - Corporation LawDokument134 SeitenCase Digests - Corporation LawLemuel R. Campiseño80% (10)

- TAX REMEDIES by Sababan Reviewer 2008 EdDokument11 SeitenTAX REMEDIES by Sababan Reviewer 2008 Edolaydyosa95% (20)

- Agreement On Contract To SaleDokument12 SeitenAgreement On Contract To SaleZiad DnetNoch keine Bewertungen

- Traning Development PPT 2Dokument18 SeitenTraning Development PPT 2Ziad DnetNoch keine Bewertungen

- Hazard Risk Assessment of Roof of The Mazanine Floor..Dokument15 SeitenHazard Risk Assessment of Roof of The Mazanine Floor..Akhtar BahramNoch keine Bewertungen

- Affidavit: IN WITNESS WHEREOF, I Have Hereunto Affixed MyDokument2 SeitenAffidavit: IN WITNESS WHEREOF, I Have Hereunto Affixed Myceleste LorenzanaNoch keine Bewertungen

- English CV Chis Roberta AndreeaDokument1 SeiteEnglish CV Chis Roberta AndreeaRoby ChisNoch keine Bewertungen

- 06-433rev7 HFC-227ea IVO ManualDokument109 Seiten06-433rev7 HFC-227ea IVO ManualFelix MartinezNoch keine Bewertungen

- MCQDokument5 SeitenMCQJagdishVankar100% (1)

- Comprehensive Soup ProjectDokument98 SeitenComprehensive Soup ProjectSachin Soni63% (8)

- Compositional Changes of Crude Oil SARA Fractions Due To Biodegradation and Adsorption Supported On Colloidal Support Such As Clay Susing IatroscanDokument13 SeitenCompositional Changes of Crude Oil SARA Fractions Due To Biodegradation and Adsorption Supported On Colloidal Support Such As Clay Susing IatroscanNatalia KovalovaNoch keine Bewertungen

- Unit5 TestDokument3 SeitenUnit5 TestAndrea MészárosnéNoch keine Bewertungen

- Clay Analysis - 1Dokument55 SeitenClay Analysis - 1JCSNoch keine Bewertungen

- ComFlor 80 Load Span Tables PDFDokument4 SeitenComFlor 80 Load Span Tables PDFAkhil VNNoch keine Bewertungen

- Medical Gases: NO. Item Brand Name OriginDokument4 SeitenMedical Gases: NO. Item Brand Name OriginMahmoud AnwerNoch keine Bewertungen

- iGCSE Biology Section 1 Lesson 1Dokument44 SeiteniGCSE Biology Section 1 Lesson 1aastha dograNoch keine Bewertungen

- Marine Turtle Survey Along The Sindh CoastDokument106 SeitenMarine Turtle Survey Along The Sindh CoastSyed Najam Khurshid100% (1)

- Pediatric Medication Dosing GuildelinesDokument2 SeitenPediatric Medication Dosing GuildelinesMuhammad ZeeshanNoch keine Bewertungen

- Nitrile Butadiene Rubber (NBR), Synthetic Latex: ApplicationDokument2 SeitenNitrile Butadiene Rubber (NBR), Synthetic Latex: ApplicationbobNoch keine Bewertungen

- Topic 10 - The Schooler and The FamilyDokument18 SeitenTopic 10 - The Schooler and The FamilyReanne Mae AbreraNoch keine Bewertungen

- Corp Given To HemaDokument132 SeitenCorp Given To HemaPaceNoch keine Bewertungen

- Worksheet 2 - TLC - Updated Summer 2021Dokument4 SeitenWorksheet 2 - TLC - Updated Summer 2021Bria PopeNoch keine Bewertungen

- ms1471pt5-99 - Vocabulary Smoke ControlDokument8 Seitenms1471pt5-99 - Vocabulary Smoke ControlBryan Ng Horng HengNoch keine Bewertungen

- (Template) The World in 2050 Will and Wont Reading Comprehension Exercises Writing Creative W 88793Dokument2 Seiten(Template) The World in 2050 Will and Wont Reading Comprehension Exercises Writing Creative W 88793ZulfiyaNoch keine Bewertungen

- Handover Paper Final 22 3 16 BJNDokument13 SeitenHandover Paper Final 22 3 16 BJNsisaraaah12Noch keine Bewertungen

- FPSB 2 (1) 56-62oDokument7 SeitenFPSB 2 (1) 56-62ojaouadi adelNoch keine Bewertungen

- 2006 SM600Dokument2 Seiten2006 SM600Ioryogi KunNoch keine Bewertungen

- The Modern Fire Attack - Phil Jose and Dennis LegearDokument7 SeitenThe Modern Fire Attack - Phil Jose and Dennis LegearTomNoch keine Bewertungen

- 2mw Biomass Gasification Gas Power Plant ProposalDokument9 Seiten2mw Biomass Gasification Gas Power Plant ProposalsabrahimaNoch keine Bewertungen

- TQM Assignment 3Dokument8 SeitenTQM Assignment 3ehte19797177Noch keine Bewertungen

- Indian MaDokument1 SeiteIndian MaAnass LyamaniNoch keine Bewertungen

- Heating Ventilation Air Conditioning Hvac ManualDokument4 SeitenHeating Ventilation Air Conditioning Hvac ManualShabaz KhanNoch keine Bewertungen

- Pre-Feasibility Report: at Plot No. 15/B-3, Jigani Industrial Area Anekal Taluk, Bangalore South District Karnataka byDokument41 SeitenPre-Feasibility Report: at Plot No. 15/B-3, Jigani Industrial Area Anekal Taluk, Bangalore South District Karnataka by12mchc07Noch keine Bewertungen

- Radfet DatasheetDokument6 SeitenRadfet DatasheetNicholas EspinozaNoch keine Bewertungen