Das könnte Ihnen auch gefallen

- ISP98 FormsDokument56 SeitenISP98 Formsvkrm14Noch keine Bewertungen

- Letter of CreditDokument49 SeitenLetter of CreditPratheepThankarajNoch keine Bewertungen

- Fco (Full Corporate Offer) For Type B Thermal Coal Fob ModalityDokument3 SeitenFco (Full Corporate Offer) For Type B Thermal Coal Fob ModalityJuliana Iru100% (1)

- Investment ContractDokument2 SeitenInvestment ContractchanNoch keine Bewertungen

- Unit 3 Audit Risk & Internal Control PDFDokument10 SeitenUnit 3 Audit Risk & Internal Control PDFRomi BaaNoch keine Bewertungen

- History of BankingDokument5 SeitenHistory of BankingFiker Yetagesal100% (1)

- Approaches To Resolving The International Documentary Letters of Credit Fraud Issue PDFDokument286 SeitenApproaches To Resolving The International Documentary Letters of Credit Fraud Issue PDFBình Minh Tô100% (1)

- Documentary Letter of Credit in Apparel IndustryDokument3 SeitenDocumentary Letter of Credit in Apparel Industrysuman_ishaNoch keine Bewertungen

- Idelfonso Crisologo v. PeopleDokument1 SeiteIdelfonso Crisologo v. PeopleJohney Doe100% (1)

- Budget Offer PASS M0S 245 KVDokument14 SeitenBudget Offer PASS M0S 245 KVPradip Naik0% (1)

- Aluminum Ingot SCODokument3 SeitenAluminum Ingot SCOTrindra Paul100% (1)

- 2015 Bar Q - MERCANTILE LAWDokument16 Seiten2015 Bar Q - MERCANTILE LAWLimVianesseNoch keine Bewertungen

- Chapter 3 Commercial Banking New - 1535523282Dokument13 SeitenChapter 3 Commercial Banking New - 1535523282Samuel DebebeNoch keine Bewertungen

- Zekarias MekonnenDokument68 SeitenZekarias MekonnenSamuel TekalignNoch keine Bewertungen

- Chapter Four Financial Markets in The Financial SystemDokument66 SeitenChapter Four Financial Markets in The Financial SystemMikias DegwaleNoch keine Bewertungen

- Chapter Six Financial Markets and Institutions in EthiopiaDokument44 SeitenChapter Six Financial Markets and Institutions in EthiopiaAbdiNoch keine Bewertungen

- History of Ethiopia FinalDokument42 SeitenHistory of Ethiopia FinalAnonymous JDYkbONoch keine Bewertungen

- Unit 6Dokument41 SeitenUnit 6EYOB AHMEDNoch keine Bewertungen

- 8 - 9 Test Bank For Intermediate Accounting, Fourteenth EditionDokument22 Seiten8 - 9 Test Bank For Intermediate Accounting, Fourteenth Editionsparts23100% (1)

- History of Banking - National BankDokument3 SeitenHistory of Banking - National BankDerib Asmamaw50% (2)

- Chapter Two: Principles of Accounting and Financial Reporting For State and Local Governments (SLGS)Dokument55 SeitenChapter Two: Principles of Accounting and Financial Reporting For State and Local Governments (SLGS)Bilisummaa GeetahuunNoch keine Bewertungen

- Abrahim Research Reseaserch NEWDokument39 SeitenAbrahim Research Reseaserch NEWAbdi Mucee TubeNoch keine Bewertungen

- Contemporary Issues of Financial IntermediariesDokument1 SeiteContemporary Issues of Financial IntermediariesGETAHUN ASSEFA ALEMU100% (2)

- Cash Management ProceduresDokument9 SeitenCash Management ProceduresNigussie BerhanuNoch keine Bewertungen

- Chapter 2Dokument23 SeitenChapter 2Abrha636100% (1)

- Chapter-2: Audit of Cash and Marketable SecuritiesDokument27 SeitenChapter-2: Audit of Cash and Marketable Securitiesbikilahussen100% (1)

- Bank Deposit Types and Fundamental TransactionsDokument17 SeitenBank Deposit Types and Fundamental TransactionsJamaica IndacNoch keine Bewertungen

- Audit Ch4Dokument42 SeitenAudit Ch4Eyuel SintayehuNoch keine Bewertungen

- Chapter Four Financial Market in The Financial SystemsDokument136 SeitenChapter Four Financial Market in The Financial SystemsNatnael Asfaw100% (1)

- Chapter-Four. Stock and Equity Valuation. Stock CharacteristicDokument8 SeitenChapter-Four. Stock and Equity Valuation. Stock CharacteristicOumer ShaffiNoch keine Bewertungen

- Unit 5: Audit EvidenceDokument10 SeitenUnit 5: Audit EvidenceNigussie BerhanuNoch keine Bewertungen

- Risk Assi 1234Dokument19 SeitenRisk Assi 1234Yonatan100% (1)

- Auditing I Chapter 2Dokument63 SeitenAuditing I Chapter 2Yitera Sisay100% (1)

- Banking and Finance Chapter SummaryDokument43 SeitenBanking and Finance Chapter SummaryInFiNiTy100% (1)

- Auditing CH 2 The Auditing Profession1Dokument87 SeitenAuditing CH 2 The Auditing Profession1lije100% (1)

- Receivables From An Audit Perspective?: 3.why Are Returns and Allowances Sensitive Issues in Receivables Audit?Dokument7 SeitenReceivables From An Audit Perspective?: 3.why Are Returns and Allowances Sensitive Issues in Receivables Audit?Bekeri MohammedNoch keine Bewertungen

- Cost 2 Chapter 2Dokument70 SeitenCost 2 Chapter 2Ebsa AbdiNoch keine Bewertungen

- Bank Audit and InspectionDokument2 SeitenBank Audit and InspectionD. BharadwajNoch keine Bewertungen

- ErtalDokument8 SeitenErtalYonatanNoch keine Bewertungen

- Intermediate Accounting 2Dokument2 SeitenIntermediate Accounting 2stephbatac241Noch keine Bewertungen

- Non-Depository Financial Institutions Chapter SummaryDokument30 SeitenNon-Depository Financial Institutions Chapter SummaryMarina KhanNoch keine Bewertungen

- AfPS&CS Ch-01Dokument10 SeitenAfPS&CS Ch-01Amelwork AlchoNoch keine Bewertungen

- Chapter One Accounting For Public SectorDokument10 SeitenChapter One Accounting For Public SectorFasil MillionNoch keine Bewertungen

- Banking Practice & Proc. Course OutlineDokument5 SeitenBanking Practice & Proc. Course OutlineSuresh Vadde50% (2)

- The Revenue Cycle: Sales To Cash Collections: FOSTER School of Business Acctg.320Dokument37 SeitenThe Revenue Cycle: Sales To Cash Collections: FOSTER School of Business Acctg.320Shaina Shanee CuevasNoch keine Bewertungen

- Topic 9 - The Standard Capital Asset Pricing Model Question PDFDokument15 SeitenTopic 9 - The Standard Capital Asset Pricing Model Question PDFSrinivasa Reddy SNoch keine Bewertungen

- 3chapter Three FM ExtDokument19 Seiten3chapter Three FM ExtTIZITAW MASRESHANoch keine Bewertungen

- Auditing Principles and Practice I Unit 1&2Dokument14 SeitenAuditing Principles and Practice I Unit 1&2ALEM LEMMANoch keine Bewertungen

- Insurance Contracts ExplainedDokument32 SeitenInsurance Contracts ExplainedWingFatt KhooNoch keine Bewertungen

- Chapter 2 Overview of Business ProcessDokument116 SeitenChapter 2 Overview of Business Processwog jimNoch keine Bewertungen

- Audit UNIT 6Dokument7 SeitenAudit UNIT 6Nigussie BerhanuNoch keine Bewertungen

- Credit Risk Management at Awash BankDokument67 SeitenCredit Risk Management at Awash BankMelesNoch keine Bewertungen

- Chapter One Accounting Principles and Professional PracticeDokument22 SeitenChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- Bank Interviw QutionDokument17 SeitenBank Interviw QutionAlex KumieNoch keine Bewertungen

- What Should Be The Fate of The Current Provisions Governing Joint Venture in The Forthcoming Revised Commercial Code of Ethiopia? Retention or Exclusion?Dokument18 SeitenWhat Should Be The Fate of The Current Provisions Governing Joint Venture in The Forthcoming Revised Commercial Code of Ethiopia? Retention or Exclusion?melewon2Noch keine Bewertungen

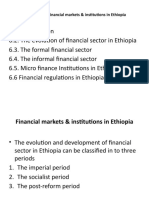

- Financial Markets and Institutions: EthiopianDokument26 SeitenFinancial Markets and Institutions: Ethiopiansemeredin wabeNoch keine Bewertungen

- Central Bank Functions ExplainedDokument7 SeitenCentral Bank Functions ExplainedTilahun MikiasNoch keine Bewertungen

- Risk Management CH 2.Dokument47 SeitenRisk Management CH 2.Aschenaki MebreNoch keine Bewertungen

- Monthly Reports: Figure 1.1: Revenue/Assistance/Loan Report Me/He 21Dokument13 SeitenMonthly Reports: Figure 1.1: Revenue/Assistance/Loan Report Me/He 21GedionNoch keine Bewertungen

- The Regulation of Financial Markets and InstitutionDokument6 SeitenThe Regulation of Financial Markets and InstitutionMany GirmaNoch keine Bewertungen

- Advanced financial accounting intercompany inventory transactionsDokument19 SeitenAdvanced financial accounting intercompany inventory transactionseferem100% (1)

- Auditing I CH 6Dokument9 SeitenAuditing I CH 6Abrha636Noch keine Bewertungen

- Assessment of Credit Risk Management in Micro Finance Institutions: A Case of Adama Town Mfis, EthiopiaDokument13 SeitenAssessment of Credit Risk Management in Micro Finance Institutions: A Case of Adama Town Mfis, EthiopiaHunde gutemaNoch keine Bewertungen

- Chapter 1 Governmental AccountingDokument12 SeitenChapter 1 Governmental AccountingMoh ShiineNoch keine Bewertungen

- Proj Chap 2Dokument10 SeitenProj Chap 2mohdarifshaikh100% (2)

- Values and Ethics From Inception To PracticeDokument29 SeitenValues and Ethics From Inception To PracticeAnonymous fE2l3DzlNoch keine Bewertungen

- Gadise Teshome PPDokument6 SeitenGadise Teshome PPTewodrose Teklehawariat BelayhunNoch keine Bewertungen

- WegagenDokument63 SeitenWegagenYonas100% (1)

- @4 Auditing and Assurance Services - WSUDokument125 Seiten@4 Auditing and Assurance Services - WSUOUSMAN SEIDNoch keine Bewertungen

- Bank Practice and Procedures (Acfn2113) : An Overview of Banks and Their FunctionDokument50 SeitenBank Practice and Procedures (Acfn2113) : An Overview of Banks and Their Functionmuke100% (1)

- Ch1 Part 2 Audit Sampling For Tests of Details of BalanceDokument46 SeitenCh1 Part 2 Audit Sampling For Tests of Details of Balanceመስቀል ኃይላችን ነውNoch keine Bewertungen

- CH 1 Audit Sampling FC1Dokument77 SeitenCH 1 Audit Sampling FC1መስቀል ኃይላችን ነውNoch keine Bewertungen

- OM Chapter 2Dokument415 SeitenOM Chapter 2መስቀል ኃይላችን ነውNoch keine Bewertungen

- OM Chapter 1Dokument135 SeitenOM Chapter 1መስቀል ኃይላችን ነውNoch keine Bewertungen

- OM Chapter 1Dokument135 SeitenOM Chapter 1መስቀል ኃይላችን ነውNoch keine Bewertungen

- OM Chapter 2Dokument415 SeitenOM Chapter 2መስቀል ኃይላችን ነውNoch keine Bewertungen

- CH 1 Audit Sampling FC1Dokument77 SeitenCH 1 Audit Sampling FC1መስቀል ኃይላችን ነውNoch keine Bewertungen

- Accounting For The Business-Type Activities of State and Local GovernmentsDokument38 SeitenAccounting For The Business-Type Activities of State and Local Governmentsመስቀል ኃይላችን ነውNoch keine Bewertungen

- CH 3 Audit of AR and Sales FCNDokument54 SeitenCH 3 Audit of AR and Sales FCNመስቀል ኃይላችን ነውNoch keine Bewertungen

- Ch1 Part 2 Audit Sampling For Tests of Details of BalanceDokument46 SeitenCh1 Part 2 Audit Sampling For Tests of Details of Balanceመስቀል ኃይላችን ነውNoch keine Bewertungen

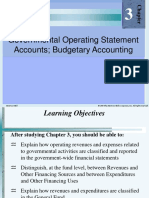

- Governmental Operating Statement Accounts Budgetary AccountingDokument75 SeitenGovernmental Operating Statement Accounts Budgetary Accountingመስቀል ኃይላችን ነው0% (2)

- Ch1 Part 2 Audit Sampling For Tests of Details of BalanceDokument46 SeitenCh1 Part 2 Audit Sampling For Tests of Details of Balanceመስቀል ኃይላችን ነውNoch keine Bewertungen

- CH 3 Audit of AR and Sales FCNDokument54 SeitenCH 3 Audit of AR and Sales FCNመስቀል ኃይላችን ነውNoch keine Bewertungen

- CH 1 Audit Sampling FC1Dokument77 SeitenCH 1 Audit Sampling FC1መስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 5 Asset-Liability Management Techniques: 5.1. General Principles of Bank ManagementDokument8 SeitenUnit 5 Asset-Liability Management Techniques: 5.1. General Principles of Bank Managementመስቀል ኃይላችን ነውNoch keine Bewertungen

- Accounting For Fiduciary Activities - Agency and Trust FundsDokument44 SeitenAccounting For Fiduciary Activities - Agency and Trust Fundsመስቀል ኃይላችን ነውNoch keine Bewertungen

- Accounting For General Long-Term Liabilities and Debt ServiceDokument50 SeitenAccounting For General Long-Term Liabilities and Debt Serviceመስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 1 An Overview of Banks and Their Function: 1.1. Historical Background of Banking 1.1.1. World Banking HistoryDokument18 SeitenUnit 1 An Overview of Banks and Their Function: 1.1. Historical Background of Banking 1.1.1. World Banking Historyመስቀል ኃይላችን ነውNoch keine Bewertungen

- Accounting For General Capital Assets and Capital ProjectsDokument49 SeitenAccounting For General Capital Assets and Capital Projectsመስቀል ኃይላችን ነውNoch keine Bewertungen

- Chapter 10Dokument37 SeitenChapter 10መስቀል ኃይላችን ነውNoch keine Bewertungen

- PPT-Unit 6Dokument10 SeitenPPT-Unit 6መስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 3: Commercial Bank Sources of Funds: 1. Transaction DepositsDokument9 SeitenUnit 3: Commercial Bank Sources of Funds: 1. Transaction Depositsመስቀል ኃይላችን ነውNoch keine Bewertungen

- Chapter 2 GADokument69 SeitenChapter 2 GAመስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 6 Financial Statements and Bank Performance EvaluationDokument9 SeitenUnit 6 Financial Statements and Bank Performance Evaluationመስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 4: Ethiopian Bank'S Loans and Advances ProceduresDokument37 SeitenUnit 4: Ethiopian Bank'S Loans and Advances Proceduresመስቀል ኃይላችን ነውNoch keine Bewertungen

- Ethiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry BanksDokument9 SeitenEthiopian Banking Sector: 2.1. Organization and Structure of Ethiopian Banking Industry Banksመስቀል ኃይላችን ነውNoch keine Bewertungen

- Unit 4: Prepared By: Tewodros EndaleDokument17 SeitenUnit 4: Prepared By: Tewodros Endaleመስቀል ኃይላችን ነውNoch keine Bewertungen

- PPT-Unit 3Dokument14 SeitenPPT-Unit 3መስቀል ኃይላችን ነውNoch keine Bewertungen

- Bank Loans & Advances Procedures Bank Loans & Advances ProceduresDokument17 SeitenBank Loans & Advances Procedures Bank Loans & Advances Proceduresመስቀል ኃይላችን ነውNoch keine Bewertungen

- Bill DiscountingDokument17 SeitenBill Discountingjohar_priyanka3723100% (1)

- Analysis of Credit Proposal for Corporate Banking Division/TITLEDokument66 SeitenAnalysis of Credit Proposal for Corporate Banking Division/TITLEGere TassewNoch keine Bewertungen

- Philippine Aluminum Wheels vs. FASGI EnterprisesDokument6 SeitenPhilippine Aluminum Wheels vs. FASGI EnterprisesMjay GuintoNoch keine Bewertungen

- Common Bank Interview QuestionsDokument23 SeitenCommon Bank Interview Questionssultan erboNoch keine Bewertungen

- Memorandum: Memorandum of Instructions On Project & Service ExportsDokument97 SeitenMemorandum: Memorandum of Instructions On Project & Service ExportsAmbar PurohitNoch keine Bewertungen

- Marphil Export Vs Allied BankDokument20 SeitenMarphil Export Vs Allied BankSamantha Ann T. TirthdasNoch keine Bewertungen

- Integrated Business Asia II Risk Analysis: Socks in MalaysiaDokument11 SeitenIntegrated Business Asia II Risk Analysis: Socks in MalaysiaSyabella TrianaNoch keine Bewertungen

- International Trade Finance: NGUYEN T Thanh Phuong, CITF® Email: Phuong - Nguyen@ftu - Edu.vnDokument110 SeitenInternational Trade Finance: NGUYEN T Thanh Phuong, CITF® Email: Phuong - Nguyen@ftu - Edu.vnVy NguyễnNoch keine Bewertungen

- 11 Quiz 1 (Trade)Dokument2 Seiten11 Quiz 1 (Trade)Melanie PermijoNoch keine Bewertungen

- Swift Cat7 mt798 Faqs 20181026Dokument23 SeitenSwift Cat7 mt798 Faqs 20181026musman0075Noch keine Bewertungen

- General Knowledge Model Question Paper Download PDFDokument5 SeitenGeneral Knowledge Model Question Paper Download PDFAkash BhoiNoch keine Bewertungen

- Analysis of Panther CompanyDokument31 SeitenAnalysis of Panther CompanyManolache RalucaNoch keine Bewertungen

- UCP IncotermsDokument4 SeitenUCP Incotermsshaunak goswamiNoch keine Bewertungen

- Export ProcedureDokument2 SeitenExport ProcedureKalpesh Singh SinghNoch keine Bewertungen

- Mercantile Law EssentialsDokument7 SeitenMercantile Law EssentialsAndrei Arkov100% (1)

- Tender 563Dokument36 SeitenTender 563KULDEEP KUMARNoch keine Bewertungen

- Standby Letter of Credit Application FormDokument1 SeiteStandby Letter of Credit Application Formalex shee chee wengNoch keine Bewertungen

- Offer: Offer & Cover Letter of OfferDokument19 SeitenOffer: Offer & Cover Letter of OfferLanChiVũNoch keine Bewertungen

- Executive SummaryDokument59 SeitenExecutive SummarywaqarNoch keine Bewertungen

- PT Bumi Perkasa Nusantara: Soft Corporate OfferingDokument4 SeitenPT Bumi Perkasa Nusantara: Soft Corporate OfferingyohansyahNoch keine Bewertungen