Das könnte Ihnen auch gefallen

- All You Need to Know About Payday LoansVon EverandAll You Need to Know About Payday LoansBewertung: 5 von 5 Sternen5/5 (1)

- PPB Module 3Dokument42 SeitenPPB Module 3RAJNoch keine Bewertungen

- UNITIIDokument66 SeitenUNITIIlokesh palNoch keine Bewertungen

- Chapter 3 Deposit MobilizationDokument28 SeitenChapter 3 Deposit MobilizationdhitalkhushiNoch keine Bewertungen

- Opening and Operating Bank AccountsDokument25 SeitenOpening and Operating Bank Accountssagarg94gmailcom100% (1)

- Banking and Cash SummaryDokument5 SeitenBanking and Cash SummaryLiam Ting WeiNoch keine Bewertungen

- 3-Banker Customer RelationshipDokument32 Seiten3-Banker Customer RelationshipMonika MalikNoch keine Bewertungen

- Retail BankingDokument71 SeitenRetail Bankingswati_rathourNoch keine Bewertungen

- Types of Accounts in A BankDokument25 SeitenTypes of Accounts in A Bankje-ann montejoNoch keine Bewertungen

- Retail Banking: Vivek Saxena Asst. Prof. LSB, LPU Reference: Introduction To Banking by Vijayaragvan IyengarDokument16 SeitenRetail Banking: Vivek Saxena Asst. Prof. LSB, LPU Reference: Introduction To Banking by Vijayaragvan IyengarninalakhotraNoch keine Bewertungen

- Saving Account Salary Account Current AccountDokument32 SeitenSaving Account Salary Account Current AccountSamdarshi KumarNoch keine Bewertungen

- 1627995259-Lecture - 3 TYPES OF ACCOUNTS & FINANCIAL INCLUSIONDokument4 Seiten1627995259-Lecture - 3 TYPES OF ACCOUNTS & FINANCIAL INCLUSIONKhushraj SinghNoch keine Bewertungen

- Types of DepOSIT 15-18-21-22Dokument94 SeitenTypes of DepOSIT 15-18-21-22Saurab JainNoch keine Bewertungen

- Current AccountDokument21 SeitenCurrent AccountSan Awale33% (3)

- Introduction To Banking: Mishu Tripathi Assistant Professor-FinanceDokument93 SeitenIntroduction To Banking: Mishu Tripathi Assistant Professor-FinanceSindru BarbiNoch keine Bewertungen

- Kisan Vikas PatraDokument16 SeitenKisan Vikas PatraAnonymous aAMqLLNoch keine Bewertungen

- Deposits 13514337657761 Phpapp01 121028091831 Phpapp01Dokument18 SeitenDeposits 13514337657761 Phpapp01 121028091831 Phpapp01Jithin Clashes ZcsNoch keine Bewertungen

- Types of Customers and Nature of AccountsDokument18 SeitenTypes of Customers and Nature of Accountssagarg94gmailcomNoch keine Bewertungen

- Opening and Operation of Accounts-SBDokument41 SeitenOpening and Operation of Accounts-SBnurul000Noch keine Bewertungen

- BIM - Unit-III: Unit-3 Management of Deposit and Advances. Opening of ADokument22 SeitenBIM - Unit-III: Unit-3 Management of Deposit and Advances. Opening of AMehak ShineNoch keine Bewertungen

- CP Associates Bullet PointsDokument13 SeitenCP Associates Bullet PointsvikashvacNoch keine Bewertungen

- Types of Accounts in A Bank: BY Abdul Qadir BhamaniDokument23 SeitenTypes of Accounts in A Bank: BY Abdul Qadir Bhamaniafzaal khanNoch keine Bewertungen

- Presentation of Commercial Bank Operations On The Chapter "Deposit MobilizationDokument46 SeitenPresentation of Commercial Bank Operations On The Chapter "Deposit MobilizationSaurav PantaNoch keine Bewertungen

- RB Chapter 3 - Savings BankDokument10 SeitenRB Chapter 3 - Savings BankHarish YadavNoch keine Bewertungen

- Deposit SchemesDokument7 SeitenDeposit SchemesTarun GargNoch keine Bewertungen

- Financial InclusionDokument425 SeitenFinancial InclusionNishad ThakurNoch keine Bewertungen

- Banking - Special Type Sof CustomersDokument29 SeitenBanking - Special Type Sof CustomersRevathi VadakkedamNoch keine Bewertungen

- MCB Bank ReportDokument30 SeitenMCB Bank ReportdadagfazalNoch keine Bewertungen

- Banking Law and ProceduresDokument114 SeitenBanking Law and ProceduresmonaeNoch keine Bewertungen

- ICICI Personal LoanDokument11 SeitenICICI Personal LoanAjit SamalNoch keine Bewertungen

- SAPMDokument45 SeitenSAPMswamyNoch keine Bewertungen

- Legal Aspects: Canara Bank Officers' AssociationDokument20 SeitenLegal Aspects: Canara Bank Officers' Associationmail2me.preet1801Noch keine Bewertungen

- BankingDokument32 SeitenBankingapi-173610472Noch keine Bewertungen

- Procedure of Account OpeningDokument11 SeitenProcedure of Account OpeningSky WalkerNoch keine Bewertungen

- 5 6226516373657356654Dokument230 Seiten5 6226516373657356654Sangeeta HatwalNoch keine Bewertungen

- Axis Bank Product: Term DepositDokument35 SeitenAxis Bank Product: Term DepositSaroj Kumar PandaNoch keine Bewertungen

- Type of DepositDokument12 SeitenType of DepositgaganngulatiiNoch keine Bewertungen

- Entrepreneurship Loan and SchemesDokument10 SeitenEntrepreneurship Loan and SchemesSriniketh SridharNoch keine Bewertungen

- FM Current Account 1Dokument9 SeitenFM Current Account 1varinder_saroaNoch keine Bewertungen

- General InfoDokument15 SeitenGeneral Infodhuni143Noch keine Bewertungen

- Features of Fixed DepositsDokument4 SeitenFeatures of Fixed DepositsBeula Heidy19 071Noch keine Bewertungen

- Customer Satisfaction On Housing Loan in SBI BankDokument23 SeitenCustomer Satisfaction On Housing Loan in SBI BankDebjyoti Rakshit100% (2)

- Functions of Banking Institution: by Resham Raj RegmiDokument49 SeitenFunctions of Banking Institution: by Resham Raj Regmibibek bNoch keine Bewertungen

- English For Banking and FinanceDokument28 SeitenEnglish For Banking and FinancefathiyarizkiNoch keine Bewertungen

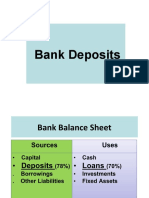

- Non-Marketable Financial Assets: Bank DepositsDokument8 SeitenNon-Marketable Financial Assets: Bank DepositsDhruv MishraNoch keine Bewertungen

- Steps 4 Opening A.CDokument20 SeitenSteps 4 Opening A.CBipinNoch keine Bewertungen

- Opening & Operation of Accounts IBPDokument136 SeitenOpening & Operation of Accounts IBPasifafaiz100% (4)

- DepositsDokument37 SeitenDepositsHarshita SahiNoch keine Bewertungen

- Banking: Presented by Mukundan SDokument31 SeitenBanking: Presented by Mukundan SRajalingam100% (1)

- Provisional Tax Saving Fixed Deposit Confirmation AdviceDokument3 SeitenProvisional Tax Saving Fixed Deposit Confirmation AdviceKunda MalleshNoch keine Bewertungen

- Calculator: Terms & Conditions - Insta Jumbo LoanDokument3 SeitenCalculator: Terms & Conditions - Insta Jumbo LoanANUDEEP CommunityNoch keine Bewertungen

- Session 17-18 Consumer and Wholesale Banking (Autosaved)Dokument61 SeitenSession 17-18 Consumer and Wholesale Banking (Autosaved)Haritika ChhatwalNoch keine Bewertungen

- Types of Accounts in A BankDokument25 SeitenTypes of Accounts in A BankchthakorNoch keine Bewertungen

- Procedures Undertaken Before Granting Bank Finance & Banking ServicesDokument24 SeitenProcedures Undertaken Before Granting Bank Finance & Banking ServicesNikhil RanjanNoch keine Bewertungen

- Idbi Bank: Casa Study Presented byDokument21 SeitenIdbi Bank: Casa Study Presented byIndal KhannaNoch keine Bewertungen

- Type of DepositDokument12 SeitenType of DepositgaganngulatiiNoch keine Bewertungen

- Presentation Of: Allied Bank LimitedDokument21 SeitenPresentation Of: Allied Bank LimitedRiaz MirzaNoch keine Bewertungen

- Types of Accounts in MCB: Internship Report On Muslim Commercial Bank Page2Dokument23 SeitenTypes of Accounts in MCB: Internship Report On Muslim Commercial Bank Page2nishazaidiNoch keine Bewertungen

- PulpectomyDokument3 SeitenPulpectomyWafa Nabilah Kamal100% (1)

- B1 Pendent SprinklerDokument2 SeitenB1 Pendent SprinklerDave BrownNoch keine Bewertungen

- A.8. Dweck (2007) - The Secret To Raising Smart KidsDokument8 SeitenA.8. Dweck (2007) - The Secret To Raising Smart KidsPina AgustinNoch keine Bewertungen

- Astm B633Dokument5 SeitenAstm B633nisha_khan100% (1)

- Hamraki Rag April 2010 IssueDokument20 SeitenHamraki Rag April 2010 IssueHamraki RagNoch keine Bewertungen

- Biology Q PDFDokument9 SeitenBiology Q PDFsumon chowdhuryNoch keine Bewertungen

- 4EVC800802-LFEN DCwallbox 5 19Dokument2 Seiten4EVC800802-LFEN DCwallbox 5 19michael esoNoch keine Bewertungen

- Complaint: Employment Sexual Harassment Discrimination Against Omnicom & DDB NYDokument38 SeitenComplaint: Employment Sexual Harassment Discrimination Against Omnicom & DDB NYscl1116953Noch keine Bewertungen

- G.R. No. 178741Dokument1 SeiteG.R. No. 178741Jefferson BagadiongNoch keine Bewertungen

- NTJN, Full Conference Program - FINALDokument60 SeitenNTJN, Full Conference Program - FINALtjprogramsNoch keine Bewertungen

- Atlas of Feline Anatomy For VeterinariansDokument275 SeitenAtlas of Feline Anatomy For VeterinariansДибензол Ксазепин100% (4)

- Marketing Study of Mango JuiceDokument18 SeitenMarketing Study of Mango JuiceVijay ArapathNoch keine Bewertungen

- People of The Philippines V. Crispin Payopay GR No. 141140 2003/07/2001 FactsDokument5 SeitenPeople of The Philippines V. Crispin Payopay GR No. 141140 2003/07/2001 FactsAb CastilNoch keine Bewertungen

- NURTURE Module-V 11 1 en PDFDokument4 SeitenNURTURE Module-V 11 1 en PDFJorge SingNoch keine Bewertungen

- Careerride Com Electrical Engineering Interview Questions AsDokument21 SeitenCareerride Com Electrical Engineering Interview Questions AsAbhayRajSinghNoch keine Bewertungen

- Unknown Facts About Physicians Email List - AverickMediaDokument13 SeitenUnknown Facts About Physicians Email List - AverickMediaJames AndersonNoch keine Bewertungen

- Rigging: GuideDokument244 SeitenRigging: Guideyusry72100% (11)

- Cis MSCMDokument15 SeitenCis MSCMOliver DimailigNoch keine Bewertungen

- 10.1.polendo (Additional Patent)Dokument11 Seiten10.1.polendo (Additional Patent)Rima AmaliaNoch keine Bewertungen

- 2015 12 17 - Parenting in America - FINALDokument105 Seiten2015 12 17 - Parenting in America - FINALKeaneNoch keine Bewertungen

- 3 Ways To Take Isabgol - WikiHowDokument6 Seiten3 Ways To Take Isabgol - WikiHownasirNoch keine Bewertungen

- Ra Concrete Chipping 7514Dokument5 SeitenRa Concrete Chipping 7514Charles DoriaNoch keine Bewertungen

- Tractor Price and Speci Cations: Tractors in IndiaDokument4 SeitenTractor Price and Speci Cations: Tractors in Indiatrupti kadamNoch keine Bewertungen

- Glycolysis Krebscycle Practice Questions SCDokument2 SeitenGlycolysis Krebscycle Practice Questions SCapi-323720899Noch keine Bewertungen

- Impression TakingDokument12 SeitenImpression TakingMaha SelawiNoch keine Bewertungen

- Standerdised Tools of EducationDokument25 SeitenStanderdised Tools of Educationeskays30100% (11)

- Form 28 Attendence RegisterDokument1 SeiteForm 28 Attendence RegisterSanjeet SinghNoch keine Bewertungen

- Pressure Classes: Ductile Iron PipeDokument4 SeitenPressure Classes: Ductile Iron PipesmithNoch keine Bewertungen

- BS 65-1981Dokument27 SeitenBS 65-1981jasonNoch keine Bewertungen

- UgpeDokument3 SeitenUgpeOlety Subrahmanya SastryNoch keine Bewertungen