Das könnte Ihnen auch gefallen

- Overview of GST Session II and III Final - RTCDokument25 SeitenOverview of GST Session II and III Final - RTCSuresh Kumar YathirajuNoch keine Bewertungen

- Input Tax Credit BasicsDokument16 SeitenInput Tax Credit BasicsPreeti SapkalNoch keine Bewertungen

- Goods and Services Tax (GST) in India: Input Tax Credit (ITC)Dokument24 SeitenGoods and Services Tax (GST) in India: Input Tax Credit (ITC)Noman AreebNoch keine Bewertungen

- UntitledDokument9 SeitenUntitledsuyash dugarNoch keine Bewertungen

- GST Overview Rachana 1Dokument31 SeitenGST Overview Rachana 1Path A Way AheadNoch keine Bewertungen

- GST in BankingDokument23 SeitenGST in BankingNareshaasatNoch keine Bewertungen

- Goods and Service Tax (GST)Dokument19 SeitenGoods and Service Tax (GST)Saurabh Kumar SharmaNoch keine Bewertungen

- CA Ashish Chaudhary 1Dokument30 SeitenCA Ashish Chaudhary 1sonapakhi nandyNoch keine Bewertungen

- GSTN GSTIN, Input Tax CreditDokument9 SeitenGSTN GSTIN, Input Tax CreditAkanksha VermaNoch keine Bewertungen

- Session 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalDokument42 SeitenSession 3 & 4 - Input Tax Credit and Cross Utilisation of Taxes FinalaskNoch keine Bewertungen

- Unit 2Dokument79 SeitenUnit 2Sathya saiNoch keine Bewertungen

- Returns and Refund Under GSTDokument7 SeitenReturns and Refund Under GSTkoushiki mishraNoch keine Bewertungen

- UNIT 2 Registration Under GSTDokument35 SeitenUNIT 2 Registration Under GSTaKsHaT sHaRmANoch keine Bewertungen

- Input Tax credit-GSTDokument17 SeitenInput Tax credit-GSTSandhya DangiNoch keine Bewertungen

- Audit Under GSTDokument11 SeitenAudit Under GSTRameshwar FundipalleNoch keine Bewertungen

- 2020 12 14 GST For FPOsDokument15 Seiten2020 12 14 GST For FPOschaithanya CRDSNoch keine Bewertungen

- Input Tax Credit Under GST by CA. Nagesh Jadhav PDFDokument22 SeitenInput Tax Credit Under GST by CA. Nagesh Jadhav PDFLumita SinghNoch keine Bewertungen

- Types of Supply GSTDokument46 SeitenTypes of Supply GSTRajatKumarNoch keine Bewertungen

- GST Unit 4Dokument48 SeitenGST Unit 4SANSKRITI YADAV 22DM236Noch keine Bewertungen

- Topic 10 - GSTDokument58 SeitenTopic 10 - GSTmichael krueseiNoch keine Bewertungen

- GST SupplyDokument15 SeitenGST SupplySaloni KejdiwalNoch keine Bewertungen

- GST Understanding Form GSTR 3BDokument10 SeitenGST Understanding Form GSTR 3BAkhil SoodNoch keine Bewertungen

- Integrated Goods and Services Tax (IGST) : Made by Anshuman VyasDokument16 SeitenIntegrated Goods and Services Tax (IGST) : Made by Anshuman VyasAnshuman VyasNoch keine Bewertungen

- Returns in Goods and Services Tax: A Brief OverviewDokument38 SeitenReturns in Goods and Services Tax: A Brief OverviewSushant SaxenaNoch keine Bewertungen

- GST FrameworkDokument21 SeitenGST FrameworkExecutive EngineerNoch keine Bewertungen

- Goods and Service TaxDokument30 SeitenGoods and Service TaxR.SUDHIR RameshNoch keine Bewertungen

- GST Accounting Impact & Accounting SoftwareDokument15 SeitenGST Accounting Impact & Accounting SoftwarenaapbooksNoch keine Bewertungen

- GSTR 1 Filing GuideDokument40 SeitenGSTR 1 Filing GuideJeetu PorwalNoch keine Bewertungen

- Unit I.4 - Levy and Collection of GSTDokument38 SeitenUnit I.4 - Levy and Collection of GSTFake MailNoch keine Bewertungen

- Goods & Services Tax - GSTDokument18 SeitenGoods & Services Tax - GSTPuneetNoch keine Bewertungen

- Unit 4 - GST Liability & Input Tax CreditDokument13 SeitenUnit 4 - GST Liability & Input Tax CreditPrathik PsNoch keine Bewertungen

- WHAT IS GSTDokument31 SeitenWHAT IS GSTBIKRAM KUMAR BEHERANoch keine Bewertungen

- GST Presentation Explains India's Upcoming Tax ReformDokument44 SeitenGST Presentation Explains India's Upcoming Tax ReformAlimehdi MukadamNoch keine Bewertungen

- Ayush PendDokument62 SeitenAyush PendPankaj MahantaNoch keine Bewertungen

- By Prof. Vijayakumar R Head, Department of CommerceDokument18 SeitenBy Prof. Vijayakumar R Head, Department of Commercevijaywin6299Noch keine Bewertungen

- GST Briefing: Key PointsDokument13 SeitenGST Briefing: Key PointsKhaja Afreen TNoch keine Bewertungen

- Input Tax Credit Mechanism in GSTDokument9 SeitenInput Tax Credit Mechanism in GSThanumanthaiahgowdaNoch keine Bewertungen

- Taxation IIIrd year-CGSTDokument7 SeitenTaxation IIIrd year-CGSTsuraj shekhawatNoch keine Bewertungen

- 3 1.2.2 Principal Adg Sushil Solanki GSTDokument23 Seiten3 1.2.2 Principal Adg Sushil Solanki GSTpradeeperd10011988Noch keine Bewertungen

- Unit 4 GSTDokument13 SeitenUnit 4 GSTViral OkNoch keine Bewertungen

- GST ITC ConditionsDokument6 SeitenGST ITC ConditionsKenny PhilipsNoch keine Bewertungen

- 1) Rate Structure Under GST: GST Rates For Supply of Goods: For Inter-State Supply, IGST Rates Are: Nil, 0.25%Dokument2 Seiten1) Rate Structure Under GST: GST Rates For Supply of Goods: For Inter-State Supply, IGST Rates Are: Nil, 0.25%Mohit BNoch keine Bewertungen

- Goods and Services Tax " Future in India": by - Joe Suhas Thambi Rahul Aurade MET Institute of Management, NasikDokument33 SeitenGoods and Services Tax " Future in India": by - Joe Suhas Thambi Rahul Aurade MET Institute of Management, NasikJOEMEETSMONUNoch keine Bewertungen

- Understanding GST: Key Concepts and ImpactsDokument27 SeitenUnderstanding GST: Key Concepts and ImpactsVaishali SharmaNoch keine Bewertungen

- GST - Hospitality IndustryDokument68 SeitenGST - Hospitality IndustrySOPHIA POLYTECHNIC LIBRARYNoch keine Bewertungen

- Presentation On : Kiet Group of InstitutionsDokument27 SeitenPresentation On : Kiet Group of InstitutionsVaishali SharmaNoch keine Bewertungen

- GST Word 7Dokument62 SeitenGST Word 7aparna aravamudhanNoch keine Bewertungen

- GST Goods & Service TaxDokument36 SeitenGST Goods & Service Taxhahire100% (2)

- GST Seminar BasicsDokument29 SeitenGST Seminar BasicsVenkatraman NatarajanNoch keine Bewertungen

- Goods and Services Tax (GST) in India: Ca R.K.BhallaDokument30 SeitenGoods and Services Tax (GST) in India: Ca R.K.BhallaIrfanNoch keine Bewertungen

- Tax Assignment 1Dokument16 SeitenTax Assignment 1Tunvir Islam Faisal100% (2)

- GSTR 1 - Presentation by GSTN - 30 August 2017Dokument42 SeitenGSTR 1 - Presentation by GSTN - 30 August 2017NitishNoch keine Bewertungen

- Uae Vat PresentationDokument64 SeitenUae Vat PresentationAhammed MuzammilNoch keine Bewertungen

- Unit 4Dokument16 SeitenUnit 4Abhishek Kumar GuptaNoch keine Bewertungen

- Benefits of GST ImplementationDokument6 SeitenBenefits of GST ImplementationMinhans SrivastavaNoch keine Bewertungen

- GST Registration Procedure and FAQsDokument21 SeitenGST Registration Procedure and FAQsSahil KumarNoch keine Bewertungen

- Everything You Need to Know About Pakistan's New VAT LawDokument4 SeitenEverything You Need to Know About Pakistan's New VAT LawMuneeb Ghufran DadawalaNoch keine Bewertungen

- Input Tax CreditDokument5 SeitenInput Tax CreditSowmya GuptaNoch keine Bewertungen

- People and Environment TestDokument7 SeitenPeople and Environment TestKavitha Kavi KaviNoch keine Bewertungen

- MCQ Commerce BookDokument20 SeitenMCQ Commerce BookKavitha Kavi KaviNoch keine Bewertungen

- Quick Research Part 2Dokument4 SeitenQuick Research Part 2Kavitha Kavi KaviNoch keine Bewertungen

- VOLUME 1 - CONFERENCE PROCEEDINGS FINAL - Compressed PDFDokument570 SeitenVOLUME 1 - CONFERENCE PROCEEDINGS FINAL - Compressed PDFKavitha Kavi KaviNoch keine Bewertungen

- Maane MaaneDokument105 SeitenMaane MaaneMadhu KarthikeyanNoch keine Bewertungen

- Department of Commerce BTDokument5 SeitenDepartment of Commerce BTKavitha Kavi KaviNoch keine Bewertungen

- Procedures, Prohibition EditedDokument16 SeitenProcedures, Prohibition EditedKavitha Kavi KaviNoch keine Bewertungen

- Financial Accounts BasicsDokument19 SeitenFinancial Accounts BasicsKavitha Kavi KaviNoch keine Bewertungen

- GST 30 EditedDokument31 SeitenGST 30 EditedKavitha Kavi KaviNoch keine Bewertungen

- Audit Under Goods and Service Tax (GST)Dokument7 SeitenAudit Under Goods and Service Tax (GST)Kavitha Kavi KaviNoch keine Bewertungen

- Basic Concepts of Financial Accounting ExplainedDokument42 SeitenBasic Concepts of Financial Accounting ExplainedKavitha Kavi KaviNoch keine Bewertungen

- Calculate Time, Distance or Speed Using FormulasDokument23 SeitenCalculate Time, Distance or Speed Using FormulasKavitha Kavi KaviNoch keine Bewertungen

- GST Audit Types and ProceduresDokument8 SeitenGST Audit Types and ProceduresKavitha Kavi KaviNoch keine Bewertungen

- Double Entry System and Trial BalanceDokument11 SeitenDouble Entry System and Trial BalanceKavitha Kavi KaviNoch keine Bewertungen

- Offences-Penalties of GST EditedDokument12 SeitenOffences-Penalties of GST EditedKavitha Kavi KaviNoch keine Bewertungen

- Basic Concepts of Financial Accounting EditedDokument42 SeitenBasic Concepts of Financial Accounting EditedKavitha Kavi KaviNoch keine Bewertungen

- Malayan Banking Berhad bank statementDokument3 SeitenMalayan Banking Berhad bank statementalcf99Noch keine Bewertungen

- Instructions: Place The Letter Corresponding To Your Answers On The Box Provided BelowDokument3 SeitenInstructions: Place The Letter Corresponding To Your Answers On The Box Provided Belowgazer beamNoch keine Bewertungen

- Data DictionaryDokument36 SeitenData DictionaryDheeya NuruddinNoch keine Bewertungen

- Acctng ProcessDokument4 SeitenAcctng ProcessElaine YapNoch keine Bewertungen

- Chapter 7Dokument27 SeitenChapter 7carlo knowsNoch keine Bewertungen

- Standard Chartered MBA certificate guideDokument67 SeitenStandard Chartered MBA certificate guideRishav Ch100% (1)

- FAQ General FinacleDokument39 SeitenFAQ General Finacleshc1288% (8)

- TEST 1 - ACC117 - Q - December 2021Dokument6 SeitenTEST 1 - ACC117 - Q - December 2021Ameerul HarithNoch keine Bewertungen

- TallyDokument25 SeitenTallyMahesh PawarNoch keine Bewertungen

- 12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01Dokument18 Seiten12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01praveentyagiNoch keine Bewertungen

- MT94042 enDokument18 SeitenMT94042 enAjeesh SudevanNoch keine Bewertungen

- 6 CHDokument27 Seiten6 CHjafariNoch keine Bewertungen

- Acc 114 p1 ReviewerDokument9 SeitenAcc 114 p1 ReviewerRona Amor MundaNoch keine Bewertungen

- Cash Disbursements JournalDokument1 SeiteCash Disbursements JournalEdwin Siruno LopezNoch keine Bewertungen

- 81B02Dokument2 Seiten81B02Thomson TanNoch keine Bewertungen

- Shivaji University B.Com Corporate Accounting SyllabusDokument5 SeitenShivaji University B.Com Corporate Accounting Syllabusshivaji jadhavNoch keine Bewertungen

- Intermediate Accounting II Problem SetDokument4 SeitenIntermediate Accounting II Problem SetM Sul100% (1)

- 2 ACCT 2A&B P. OperationDokument6 Seiten2 ACCT 2A&B P. OperationBrian Christian VillaluzNoch keine Bewertungen

- Evid SyllabusDokument111 SeitenEvid SyllabusDuds GutierrezNoch keine Bewertungen

- Annamalai University: Directorate of Distance EducationDokument314 SeitenAnnamalai University: Directorate of Distance EducationMALU_BOBBYNoch keine Bewertungen

- AP-115-Unit-4 RECORDING BUSINESS TRANSACTIONSDokument40 SeitenAP-115-Unit-4 RECORDING BUSINESS TRANSACTIONSBebie Joy Urbano100% (1)

- Section 3: Preparing A Trial Balance: - Enduring UnderstandingsDokument26 SeitenSection 3: Preparing A Trial Balance: - Enduring UnderstandingsBo Na YoonNoch keine Bewertungen

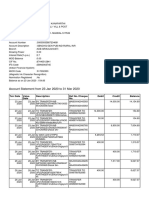

- 23 Jan To 31mar 2020 Sbi Suresh StateDokument12 Seiten23 Jan To 31mar 2020 Sbi Suresh Stateravi lingamNoch keine Bewertungen

- Hindustan Zinc Ltd. FinanceDokument75 SeitenHindustan Zinc Ltd. Financerahulsogani123Noch keine Bewertungen

- SOP: Bank Reconciliations: Stage I: Recording Bank StatementsDokument3 SeitenSOP: Bank Reconciliations: Stage I: Recording Bank Statementsudit guptaNoch keine Bewertungen

- Basic Accounting - Midterm 2009Dokument6 SeitenBasic Accounting - Midterm 2009Trixia Floie GalimbaNoch keine Bewertungen

- Financial Statements and Their Analysis - Service and Merchandising BusinessDokument21 SeitenFinancial Statements and Their Analysis - Service and Merchandising BusinessJoana Marie DonatoNoch keine Bewertungen

- Accounting 5 Step GuideDokument16 SeitenAccounting 5 Step GuideshangueleiNoch keine Bewertungen

- Eft, Ecs, Core Banking SolutionsDokument28 SeitenEft, Ecs, Core Banking SolutionsRamya KarthiNoch keine Bewertungen

- FinDokument129 SeitenFinSoniJimishNoch keine Bewertungen